UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended 31 March 2018

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report

For the transition period from to

Commission file number 1-15240

JAMES HARDIE INDUSTRIES plc

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Ireland

(Jurisdiction of incorporation or organization)

Europa House, Second Floor

Harcourt Centre

Harcourt Street, Dublin 2, Ireland

(Address of principal executive offices)

Natasha Mercer

Corporate Secretary

(Contact name)

353 1411 6924 (Telephone) 353 1479 1128 (Facsimile)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

| | |

Title of each class: | | Name of each exchange on which registered: |

Common stock, represented by CHESS Units of Foreign Securities | | New York Stock Exchange* |

CHESS Units of Foreign Securities | | New York Stock Exchange* |

American Depositary Shares, each representing one unit of CHESS Units of Foreign Securities | | New York Stock Exchange |

* Listed, not for trading, but only in connection with the registered American Depositary Shares, pursuant to the requirements of the U.S. Securities and Exchange Commission |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report:

441,524,118 shares of common stock at 31 March 2018

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ☐ Yes ☒ No

Note — Checking the box will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definition of “large accelerated filer,” “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | |

Large accelerated filer | | ☒ |

Accelerated filer | | ☐ |

Non-accelerated filer | | ☐ |

Emerging growth company | | ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised† financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after 5 April 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

| | |

International Financial Reporting Standards as issued by the International Accounting Standards Board | | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

☐ Item 17 ☐ Item 18

If this is an Annual Report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

2018

ANNUAL REPORT

ON FORM 20-F

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | i |

| |

TABLE OF CONTENTS

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | ii |

| |

FORM 20-F CROSS REFERENCE

|

| |

| Page(s) |

PART 1 | |

Item 1. Identity of Directors, Senior Management and Advisers | Not applicable |

Item 2. Offer Statistics and Expected Timetable | Not applicable |

Item 3. Key Information | |

A. Selected Financial Data | 1-3 |

B. Capitalization and Indebtedness | Not applicable |

C. Reasons for the Offer and Use of Proceeds | Not applicable |

D. Risk Factors | 159-175 |

Item 4. Information on the Company | |

A. History and Development of the Company | 4-5; 16-17 |

B. Business Overview | 6-13 |

C. Organizational Structure | 5;13 |

D. Property, Plants and Equipment | 14-17; 109 |

Item 4A. Unresolved Staff Comments | None |

Item 5. Operating and Financial Review and Prospects | |

A. Operating Results | 92-106 |

B. Liquidity and Capital Resources | 106-110 |

C. Research and Development, Patents and Licenses, etc. | 11-12 |

D. Trend Information | 110-111 |

E. Off-Balance Sheet Arrangements | 111 |

F. Tabular Disclosure of Contractual Obligations | 111-112 |

G. Safe Harbor | 86-87 |

Item 6. Directors, Senior Management and Employees | |

A. Directors and Senior Management | 18-28 |

B. Compensation | 29-67 |

C. Board Practices | 23-28; 68-85 |

D. Employees | 180 |

E. Share Ownership | 59-60; 63-67 |

Item 7. Major Shareholders and Related Party Transactions | |

A. Major Shareholders | 203-205 |

B. Related Party Transactions | 77 |

C. Interests of Experts and Counsel | Not Applicable |

Item 8. Financial Information | |

A. Consolidated Statements and Other Financial Information | 113-157; 188-189 |

B. Significant Changes | None |

Item 9. The Offer and Listing | |

A. Offer and Listing Details | 180-183 |

B. Plan of Distribution | Not Applicable |

C. Markets | 181-182 |

D. Selling Shareholders | Not Applicable |

| |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | iii |

| |

|

| |

PART 1 (continued) | |

E. Dilution | Not Applicable |

F. Expenses of the Issue | Not Applicable |

Item 10. Additional Information | |

A. Share Capital | Not Applicable |

B. Memorandum and Articles of Association | 184-191 |

C. Material Contracts | 191 |

D. Exchange Controls | 191-192 |

E. Taxation | 192-198 |

F. Dividends and Paying Agents | Not Applicable |

G. Statement by Experts | Not Applicable |

H. Documents on Display | 199 |

I. Subsidiary Information | Not Applicable |

Item 11. Quantitative and Qualitative Disclosures About Market Risk | 200-202 |

Item 12. Description of Securities Other Than Equity Securities | |

A. Debt Securities | Not Applicable |

B. Warrants and Rights | Not Applicable |

C. Other Securities | Not Applicable |

D. American Depositary Shares | 182-183 |

PART II | |

Item 13. Defaults, Dividend Arrearages and Delinquencies | None |

Item 14. Material Modifications to the Rights of Security Holders and Use of Proceeds | None |

Item 15. Controls and Procedures | 178-179 |

Item 16A. Audit Committee Financial Expert | 80 |

Item 16B. Code of Ethics | 78-79 |

Item 16C. Principal Accountant Fees and Services | 158 |

Item 16D. Exemptions from the Listing Standards for Audit Committees | None |

Item 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers | None |

Item 16F. Change in Registrant’s Certifying Accountant | None |

Item 16G. Corporate Governance | 68-85 |

Item 16H. Mine Safety Disclosures | 15-16 |

PART III | |

Item 17. Financial Statements | Not Applicable |

Item 18. Financial Statements | 113-157 |

Item 19. Exhibits | 210-214 |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 1 |

| |

SECTION 1

INTRODUCTION

James Hardie Industries plc is a world leader in the manufacture of fiber cement siding and backerboard. Our products are used in a number of markets, including new residential construction (single and multi-family housing), manufactured housing, repair and remodeling and a variety of commercial and industrial applications. We manufacture numerous types of fiber cement products with a variety of patterned profiles and surface finishes for a range of applications, including external siding and trim and soffit lining, internal linings, facades and floor and tile underlay. Our current primary geographic markets include the United States of America (“US,” “USA” or the “United States”), Canada, Australia, New Zealand, the Philippines and Europe.

James Hardie Industries plc is a “public limited company,” incorporated and existing under the laws of Ireland. Except as the context otherwise may require, references in this Annual Report on Form 20-F (this “Annual Report”) to “James Hardie,” the “James Hardie Group,” the “Company,” “JHI plc,” “we,” “our” or “us” refer to James Hardie Industries plc, together with its direct and indirect wholly owned subsidiaries as of the time relevant to the applicable reference.

For certain information about the basis of preparing the financial information in this Annual Report, see “Section 2 – Reading this Report.” In addition, this Annual Report contains statements that constitute “forward-looking statements.” For an explanation of forward-looking statements and the risks, uncertainties and assumptions to which they are subject, see “Section 2 – Reading this Report.” Further, a “Glossary of Abbreviations and Definitions” has also been included under Section 4 of this Annual Report.

The term “fiscal year” refers to our fiscal year ended 31 March of such year; the term “dollars,” “US$” or “$” refers to US dollars; and the term “A$” refers to Australian dollars.

Information contained in or accessible through the websites mentioned in this Annual Report does not form a part of this Annual Report unless we specifically state that it is incorporated by reference herein. All references in this Annual Report to websites are inactive textual references and are for information only.

SELECTED FINANCIAL DATA

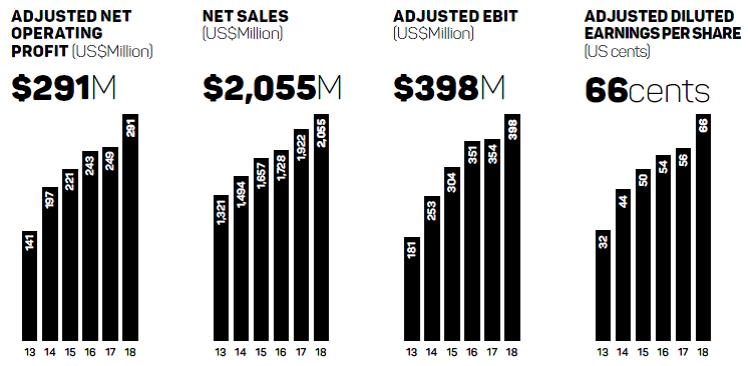

We have included in this Annual Report the audited consolidated financial statements of the Company, consisting of our consolidated balance sheets as of 31 March 2018 and 2017, and our consolidated statements of operations and comprehensive income, cash flows and changes in shareholders’ deficit for each of the years ended 31 March 2018, 2017 and 2016, together with the related notes thereto. The consolidated financial statements included in this Annual Report have been prepared in accordance with accounting principles generally accepted in the US (“US GAAP”).

The selected consolidated financial information, summarized below for the five most recent fiscal years has been derived in part from the Company’s consolidated financial statements. You should read the selected consolidated financial information in conjunction with the Company’s consolidated financial statements and related notes contained in “Section 2 – Consolidated Financial Statements” and with the information provided in “Section 2 – Management’s Discussion and Analysis.” Historic financial data is not necessarily indicative of our future results and you should not unduly rely on it.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 2 |

| |

|

| | | | | | | | | | | | | | | | | | | | |

| | (Millions of US dollars) |

Consolidated Statement of Operations Data | | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Net sales | | $ | 2,054.5 |

| | $ | 1,921.6 |

| | $ | 1,728.2 |

| | $ | 1,656.9 |

| | $ | 1,493.8 |

|

Income from operations1 | | 146.1 |

| | 276.5 |

| | 244.4 |

| | 291.3 |

| | 99.5 |

|

Net income1 | | $ | 146.1 |

| | $ | 276.5 |

| | $ | 244.4 |

| | $ | 291.3 |

| | $ | 99.5 |

|

| | | | | | | | | | |

| | (Millions of US dollars) |

Consolidated Balance Sheet Data | | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Total assets | | $ | 2,351.0 |

| | $ | 2,012.7 |

| | $ | 2,029.4 |

| | $ | 2,036.4 |

| | $ | 2,104.0 |

|

Net assets | | (221.5 | ) | | (212.2 | ) | | (225.2 | ) | | (202.6 | ) | | (199.0 | ) |

Common stock | | $ | 229.5 |

| | $ | 229.1 |

| | $ | 231.4 |

| | $ | 231.2 |

| | $ | 230.6 |

|

| | | | | | | | | | |

| | (Millions) |

Shares | | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Basic weighted average number of common shares | | 441.2 |

| | 442.7 |

| | 445.3 |

| | 445.0 |

| | 442.6 |

|

Diluted weighted average number of common shares | | 442.3 |

| | 443.9 |

| | 447.2 |

| | 446.4 |

| | 444.6 |

|

| | | | | | | | | | |

| | (US dollar) |

Earnings Per Share | | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Income from operations per common share – basic | | $ | 0.33 |

| | $ | 0.62 |

| | $ | 0.55 |

| | $ | 0.65 |

| | $ | 0.22 |

|

Net income per common share – basic | | 0.33 |

| | 0.62 |

| | 0.55 |

| | 0.65 |

| | 0.22 |

|

Income from operations per common share – diluted | | 0.33 |

| | 0.62 |

| | 0.55 |

| | 0.65 |

| | 0.22 |

|

Net income per common share – diluted | | 0.33 |

| | 0.62 |

| | 0.55 |

| | 0.65 |

| | 0.22 |

|

Dividends declared per share | | 0.38 |

| | 0.39 |

| | 0.58 |

| | 0.60 |

| | 0.73 |

|

Dividends paid per share | | $ | 0.38 |

| | $ | 0.39 |

| | $ | 0.58 |

| | $ | 0.88 |

| | $ | 0.45 |

|

|

| | | | | | | | | | | | | | | | | | | | |

Other Financial Data | | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Cash Flow (Millions of US dollars) | | | | | | | | | | |

Net cash provided by operating activities | | $ | 295.0 |

| | $ | 292.1 |

| | $ | 260.4 |

| | $ | 179.5 |

| | $ | 322.8 |

|

Net cash used in investing activities | | (200.6 | ) | | (109.0 | ) | | (66.6 | ) | | (277.9 | ) | | (118.8 | ) |

Net cash provided by (used in) financing activities | | $ | 112.5 |

| | $ | (212.7 | ) | | $ | (154.4 | ) | | $ | (4.6 | ) | | $ | (186.3 | ) |

Volume (million square feet) | | | | | | | | | | |

North America Fiber Cement | | 2,238.8 |

| | 2,215.4 |

| | 1,969.2 |

| | 1,821.5 |

| | 1,672.7 |

|

International Fiber Cement 2 | | 528.7 |

| | 487.2 |

| | 480.9 |

| | 484.4 |

| | 441.4 |

|

International Fiber Cement excluding the Australian Pipes business | | 528.7 |

| | 487.2 |

| | 471.1 |

| | 442.8 |

| | 404.1 |

|

Net Sales (Millions of US dollars) | | | | | | | | | | |

North America Fiber Cement | | $ | 1,578.1 |

| | $ | 1,493.4 |

| | $ | 1,335.0 |

| | $ | 1,224.7 |

| | $ | 1,083.6 |

|

International Fiber Cement 2 | | 461.7 |

| | 411.8 |

| | 379.4 |

| | 418.4 |

| | 399.2 |

|

International Fiber Cement excluding the Australian Pipes business | | 461.7 |

| | 411.8 |

| | 374.3 |

| | 392.3 |

| | 373.1 |

|

Other Businesses | | $ | 14.7 |

| | $ | 16.4 |

| | $ | 13.8 |

| | $ | 13.8 |

| | $ | 11.0 |

|

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 3 |

| |

|

| | | | | | | | | | | | | | | | | | | | |

| | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Average sales price per unit (per thousand square feet) | | | | | | | | | | |

North America Fiber Cement | | $ | 698 |

| | $ | 665 |

| | $ | 669 |

| | $ | 666 |

| | $ | 641 |

|

International Fiber Cement 2 | | 774 |

| | 775 |

| | 729 |

| | 811 |

| | 846 |

|

International Fiber Cement excluding the Australian Pipes business | | $ | 774 |

| | $ | 775 |

| | $ | 734 |

| | $ | 829 |

| | $ | 859 |

|

____________

| |

1 | Income from operations and net income include the following: asbestos adjustments, Asbestos Injuries Compensation Fund (“AICF”) selling, general and administrative (“SG&A”) expenses, AICF interest income (expense), loss on early debt extinguishment, Fermacell acquisition costs, non-recurring stamp duty, New Zealand weathertightness claims and related tax adjustments. |

|

| | | | | | | | | | | | | | | | | | | | |

| | (Millions of US dollars) |

Other Financial Data | | 2018 | | 2017 | | 2016 | | 2015 | | 2014 |

Asbestos adjustments (expense) benefit | | $ | (156.4 | ) | | $ | 40.4 |

| | $ | 5.5 |

| | $ | 33.4 |

| | $ | (195.8 | ) |

AICF SG&A expenses | | (1.9 | ) | | (1.5 | ) | | (1.7 | ) | | (2.5 | ) | | (2.1 | ) |

AICF interest income (expense) | | 1.9 |

| | (1.1 | ) | | (0.3 | ) | | 1.4 |

| | 2.9 |

|

Loss on early debt extinguishment | | (26.1 | ) | | — |

| | — |

| | — |

| | — |

|

Fermacell acquisition costs | | (10.0 | ) | | — |

| | — |

| | — |

| | — |

|

Non-recurring stamp duty | | — |

| | — |

| | — |

| | (4.2 | ) | | — |

|

New Zealand weathertightness claims | | — |

| | — |

| | (0.5 | ) | | 4.3 |

| | (1.8 | ) |

Tax adjustments | | $ | 47.3 |

| | $ | (9.9 | ) | | $ | (1.5 | ) | | $ | 37.5 |

| | $ | 99.1 |

|

For additional information on asbestos adjustments, AICF SG&A expenses, AICF interest income (expense), loss on early debt extinguishment, Fermacell acquisition costs (related to professional, legal and other fees incurred in conjunction with the acquisition of Fermacell and its subsidiaries) and New Zealand weathertightness, see “Section 2 – Management’s Discussion and Analysis” and Notes 9, 11, 13 and 19 to our consolidated financial statements in Section 2.

| |

2 | International Fiber Cement segment includes all fiber cement products manufactured in Australia, New Zealand and the Philippines and sold in Australia, New Zealand, Asia, the Middle East and various Pacific Islands. This segment also includes product manufactured in the United States that is sold in Europe. |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 4 |

| |

INFORMATION ON THE COMPANY

History and Development of the Company

About James Hardie

James Hardie Industries plc is incorporated and existing under the laws of Ireland. As an Irish plc, we are governed by the Irish Companies Act 2014 and we operate under the regulatory requirements of numerous jurisdictions and organizations, including the Australian Securities Exchange ("ASX"), ASIC, the New York Stock Exchange (“NYSE”), the United States Securities and Exchange Commission (“SEC”), the Irish Takeover Panel and various other rulemaking bodies.

The address of our registered office in Ireland is Europa House, Second Floor, Harcourt Centre, Harcourt Street, Dublin 2, Ireland. The telephone number there is +353 1411 6924. Our agent in the United States is CT Corporation. Its office is located at 111 Eight Avenue – 13th Floor, New York, New York 10011. The address of our registered office in Australia is Level 3, 22 Pitt Street, Sydney NSW 2000 and the telephone number there is +61 2 8845 3360. Our share registry is maintained by Computershare Investor Services Pty Ltd. All inquiries and correspondence regarding holdings should be directed to: Computershare Investor Services Pty Ltd, Level 5, 115 Grenfell Street, Adelaide, SA 5000; telephone: +61 3 9415 4000 or toll free within Australia: 1300 855 080. Our American Depositary Receipt ("ADR") register is maintained by Deutsche Bank. All inquiries and correspondence regarding American Depositary Shares ("ADSs") should be directed to Deutsche Bank, 60 Wall Street, New York, New York 10005, United States; telephone 1-212-250-9100.

Our History

James Hardie was established in 1888 as an import business, listing on the ASX in 1951 to become a publicly owned company in Australia. After becoming a listed company, we built a diverse portfolio of building and industrial products. In the late-1970s, we pioneered the development of asbestos-free fiber cement technology and in the early-1980’s began designing and manufacturing a wide range of fiber cement building products that made use of the benefits that came from the products’ durability, versatility and strength. Using the technical and manufacturing expertise developed in Australia, we expanded into the United States, opening our first fiber cement plant in Fontana, California in February 1990. Today, James Hardie is a leading global manufacturer of a wide range of fiber cement building products in each of the United States, Australia, Europe, New Zealand and the Philippines.

Fermacell Acquisition

On 3 April 2018, we announced the completion of our acquisition of 100% of the outstanding stock of German-based XI (DL) Holdings GmbH and its subsidiaries (including, but not limited to, Fermacell GmbH) (collectively, "Fermacell") from Xella International S.A. in an all-cash transaction based on an enterprise value of €473.0 million.

Headquartered in Duisburg, Germany, Fermacell operates six manufacturing plants across Germany, the Netherlands and Spain, with a sales force in 12 countries and revenues generated primarily from countries in Western Europe. Fermacell is a provider of innovative building solutions, producing and distributing high-quality gypsum fiber boards and cement-bonded boards, which are two complementary products in the high performance board space. Fermacell focuses on selling full system solutions into four main segments: (1) timber frame construction; (2) dry lining applications; (3) DIY; and (4) structural fire protection. Fermacell’s products are sold into the residential repair and remodel, commercial and residential new construction markets.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 5 |

| |

See Note 19 to our consolidated financial statements in Section 2 for additional information about our Fermacell acquisition.

Our Agreement with Asbestos Injuries Compensation Fund

Prior to 1987, ABN 60 Pty Limited (formerly James Hardie Industries Limited, then the ultimate parent company of the James Hardie Group) (“ABN 60”) and two of its former subsidiaries, Amaca Pty Limited (“Amaca”) and Amaba Pty Limited (“Amaba”) (collectively the “Former James Hardie Companies”), manufactured products in Australia that contained asbestos. The manufacture and sale of these products has resulted in liabilities for the Former James Hardie Companies in Australia.

In February 2007, our shareholders approved the Amended and Restated Final Funding Agreement (“AFFA”) entered into on 21 November 2006 to provide long-term funding to AICF for the compensation of proven Australian-related personal injuries for which the Former James Hardie Companies are found liable. AICF, an independent trust, subsequently assumed ownership of the Former James Hardie Companies. We do not own AICF, however, we are entitled to appoint three directors, including the Chairman and the New South Wales (“NSW”) Government is entitled to appoint two directors.

Under the terms of the AFFA, subject to the operation of an annual cash flow cap, James Hardie 117 Pty Ltd (the “Performing Subsidiary”) will make annual payments to AICF. The amount of these annual payments is dependent on several factors, including our free cash flow (as defined in the AFFA), actuarial estimations, actual claims paid, operating expenses of AICF, changes in the AUD/USD exchange rate and the annual cash flow cap. JHI plc owns 100% of the Performing Subsidiary and guarantees the Performing Subsidiary’s obligation. As a result, for US GAAP purposes, we consider JHI plc to be the primary beneficiary of AICF.

Although we have no legal ownership in AICF, for financial reporting purposes, our interest in AICF is considered variable and we consolidate AICF due to our pecuniary and contractual interests in AICF as a result of the funding arrangements outlined in the AFFA. For additional information on our consolidation of AICF and asbestos-related assets and liabilities, see Note 2 to our consolidated financial statements.

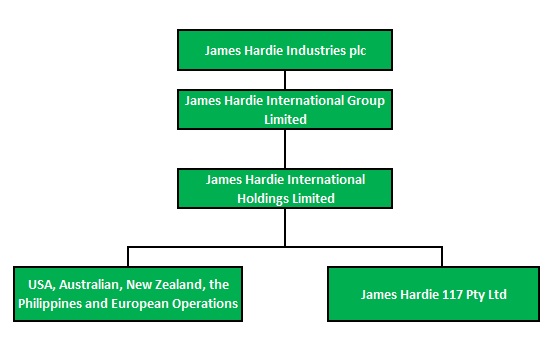

Corporate Structure

The following diagram summarizes our corporate structure at 31 March 2018:

At 31 March 2018, James Hardie International Group Limited ("JHIGL") also holds subsidiaries which were created for the subsequent acquisition of Fermacell and its subsidiaries. For further information see “Fermacell Acquisition” discussed above.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 6 |

| |

Business Overview

General Overview of Our Business

We are a world leader in the manufacture of fiber cement siding and backerboard. Based on net sales, we believe we are the largest manufacturer of fiber cement products and systems for internal and external building construction applications in the United States, Australia, New Zealand, and the Philippines. We market our fiber cement products and systems under various Hardie brand names, such as HardiePlank®, HardiePanel®, HardieTrim® and HardieBacker® boards, and other brand names such as Aspyre Collection from James Hardie™, Artisan®, Reveal®, Cemplank®, Scyon®, Ritek® and HardieLinea®.

The breakdown of our net sales by operating segment for each of our last three fiscal years is as follows:

|

| | | | | | | | | | | | |

| | (Millions of US dollars) |

| | 2018 | | 2017 | | 2016 |

North America Fiber Cement | | $ | 1,578.1 |

| | $ | 1,493.4 |

| | $ | 1,335.0 |

|

International Fiber Cement | | 461.7 |

| | 411.8 |

| | 379.4 |

|

Other Businesses | | 14.7 |

| | 16.4 |

| | 13.8 |

|

Total Net Sales | | $ | 2,054.5 |

| | $ | 1,921.6 |

| | $ | 1,728.2 |

|

Beginning with the first quarter fiscal year 2019 results, the Company intends to include a European Building Products segment in its report of quarterly results. This new segment will include the on-going James Hardie European Fiber Cement business and the newly acquired Fermacell business. The current International Fiber Cement segment will be renamed Asia Pacific Fiber Cement segment and will include our Australia, New Zealand and Philippines businesses.

Products

We manufacture a wide-range of fiber cement building materials for both internal and external use across a broad range of applications, including: external siding, internal walls, floors, ceilings, soffits, trim, fencing, decking and facades. While there are some market specific products, our core products, planks, which are used for external siding, flat panels, which are used for internal and external wall linings, and floor underlayments, are sold across all of the markets in which we operate.

Products Used in External Applications

We developed a proprietary technology platform that enables us to produce thicker yet lighter-weight fiber cement products that are generally easier to handle than most traditional building products. Further, we believe that our products provide certain durability and performance advantages leading to improved maintenance, while offering comparable aesthetics to competing products, such as wood, and superior aesthetics when compared to vinyl siding.

Performance and design advantages:

| |

• | Our fiber cement products exhibit resistance to the damaging effects of moisture, fire, impact and termites compared to natural and engineered wood and wood-based products; |

| |

• | Competing products do not duplicate fiber cement aesthetics and the characteristics necessary for effectively accepting paint applications; |

| |

• | Our fiber cement products provide the ability to imprint designs that closely resemble the patterns and profiles of traditional building materials such as wood and stucco; |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 7 |

| |

| |

• | The surface properties of our products provide an effective paint-holding finish, especially when compared to natural and engineered wood products, allowing for greater periods of time between necessary maintenance and repainting; and |

| |

• | Compared to masonry construction, fiber cement is lightweight, physically flexible and can be cut using readily available tools, making our products more appealing across a broad range of architectural styles, be it of timber or steel-framed construction. |

We believe the benefits associated with our fiber cement products have enabled us to gain a competitive advantage over competing products.

Products Used in Internal Applications

Compared to natural and oriented strand board ("OSB") and wood-based products, we believe our product range for internal applications provide the same general advantages provided by our products for external applications. In addition, our fiber cement products for internal applications exhibit less movement in response to exposure to moisture and impact damage than many competing products, providing a more consistent and durable substrate on which to install tiles. Further, we believe our ceramic tile underlayment products exhibit better handling and installation characteristics compared to fiberglass mesh cement boards.

Non-Fiber Cement Products

In addition to our portfolio of fiber cement product offerings and the recently acquired Fermacell business, we continue to invest in business development opportunities aligned with our long term strategy, including our fiberglass windows business in North America.

Significant New Products

In the United States, new products released over the last three years include the James Hardie® Insulated Lap Siding and Trim, HardieTrim® 2x board, HardieTrim® NT3® Roughsawn board, HardieTrim® Mouldings, custom colors using our ColorPlus® Technology, and an improved touch-up accessory to support ColorPlus® products. In addition, we also launched the Aspyre Collection from James Hardie™, which brings together the modernity of our Reveal® Panel System (now available with color matching Reveal Surround Trim and Exposed Fasteners in 24 colors) with the traditional profiles of our Artisan® siding products (in addition to V-Groove and lap siding, the range has been expanded to include Bevel Channel, Square channel, Shiplap and Beaded lap).

In Australia and New Zealand, extensions to the existing Stria® cladding products have been launched to provide Stria® Standard 325mm, Stria® Wide 405mm, Splayed 255mm cladding profiles. Similarly, Axon® cladding has now been extended to provide Axon® Smooth 133mm, Axon® Smooth 400mm, and Axon® Grained 133mm cladding. In addition, the new HardieBrace® online calculator tool, which is available in Australia and New Zealand, offers a way to simplify selection of bracing products. The ease of installation of core product Villaboard® lining has been enhanced with the launch of the VillaboardTM knife.

In Australia, HardieEdge® trim for covering slab edges provides an easy to install solution to unfinished, rough concrete slab edges that would otherwise detract from the appearance of a wall clad with James Hardie products. The HardieDeckTM system continues to provide a major new product offering since its launch in 2015. Modcem® modular flooring has provided an entry into commercial flooring applications. Similarly, Systemboard® cladding provides a niche multi-story construction product application. Acquisition of Building Solutions Pty Ltd, has resulted in the formation of the James Hardie Systems business unit and provided the Australian business with a new product category, the Ritek® permanent formwork walling system, a quality durable wall solution, which expands our product and systems offering into the growing medium to high density construction segment. Additions to the range of building science offerings include HardieWrap®

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 8 |

| |

weather barrier, HardieFire® Insulation, HardieBreak® Thermal Strip, as well as the HardieSmart® Boundary, Aged Care, Intertenancy and ZeroLot® Wall Systems. The launch of new wall systems are also supported by the Compliant System® trade mark. The performance of the ZeroLot® wall system is supported by the new Coreshield® protective sealer technology. An improved ZeroLot® wall system, incorporating a thinner 60mm HardieFire® insulation layer and also providing a cavity for running services, while maintaining necessary fire rating performance, has also been launched.

In New Zealand, over the same timeframe, Secura® Interior Flooring, Secura® Exterior Flooring, AxentTM Fascia, HomeRAB® 4.5mm Pre Cladding, Stria® Cladding, Axon® 400 and 133 Grained Cladding, and Linea® Oblique® Cladding have been launched.

In the Philippines, new products released over the past three years include the extension of the established Hardieflex® board range with the inclusion of Hardieflex® Wet Area Walls lining. An improved version of their wall jointing compound has been launched under the HardieFlex® Putty trade mark. A Vented Eaves extension to the Hardieflex® Eaves product is also now available.

The European business continues to provide HardieFloor® Structural Flooring, HardieFloor dB® Structural Acoustic Flooring, and HardieQStrip® Acoustic Battens into the market as part of our Smart Flooring Solutions™ offer.

Principal Markets for Our Products

United States and Canada

In the US and Canada, the largest application for fiber cement building products is in external siding for the residential building industry. The external siding market includes various cladding types, including fiber cement, vinyl, natural wood, OSB, hardboard, brick, stucco and stone. Based on industry estimates, vinyl has the largest share of the US and Canadian siding markets. External siding typically occupies a significant square footage component of the outside of every building. Selection of siding material is based on installed cost, durability, aesthetic appeal, strength, weather resistance, maintenance requirements and cost, insulating properties and other features. Different regions of the US and Canada show a preference amongst siding materials according to economic conditions, weather, materials availability and local preference.

Demand for siding in the US and Canada fluctuates based on the level of new residential housing starts and the repair and remodeling activity of existing homes. The level of activity is generally a function of interest rates and the availability of financing to homeowners to purchase a new home or make improvements to their existing homes, inflation, household income and wage growth, unemployment levels, demographic trends, gross domestic product growth and consumer confidence. The sale of fiber cement products in North America accounts for the largest portion of our net sales, accounting for 77%, 78% and 77% of our total net sales in fiscal years 2018, 2017 and 2016, respectively.

In the US and Canada, competition in the external siding market comes primarily from substitute products, such as natural or OSB, vinyl, stucco and brick. We believe we can continue to increase our market share from these competing products through targeted marketing programs designed to educate customers on our brand and the performance, design and cost advantages of our products.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 9 |

| |

International

In the Asia Pacific region, we principally sell into the Australian, New Zealand and Philippines markets, with the residential building industry representing the principal market for fiber cement products. The largest applications of fiber cement across our three primary markets are in external siding, internal walls, ceilings, floors, soffits, fences and facades. We believe the level of activity in this industry is generally a function of interest rates, inflation, household income and wage growth, unemployment levels, demographic trends, gross domestic product growth and consumer confidence. Demand for fiber cement building products is also affected by the level of new housing starts and renovation activity.

In Australia, competition from imports and two locally based fiber cement manufacturers, has intensified over the past decade. Additionally, we continue to see competition from natural and engineered wood, wallboard, masonry and brick products.

In New Zealand, we continue to see competition intensifying as fiber cement imports have become more cost competitive and overseas manufacturers look to supplement their primary operating environments with additional markets.

In the Philippines, we have seen fiber cement gain broader acceptance across a range of product applications in the last decade, leading to additional fiber cement products entering the market. We see fiber cement having long-term growth potential not only in the Philippines, but across Asia and the Middle East, as the benefits of its light-weight and durability become more widely recognized.

In Europe, fiber cement building products are used in both residential and commercial building applications in external siding, internal walls, floors, soffits and roofing. We compete in most segments, except roofing, and promote the use of fiber cement products against traditional masonry and wood-based products.

In April 2018, we completed our previously announced acquisition of Fermacell, a market leader in fiber gypsum and cement bonded boards in Europe. Like James Hardie’s fiber cement products, we believe Fermacell’s fiber gypsum boards deliver superior performance relative to competitive products, such as gypsum plaster and OSB boards. Fermacell, which is headquartered in Duisburg, Germany, operates 6 plants located in Germany, the Netherlands and Spain and has a sales force of more than 300 employees throughout Europe and the Middle East. Fermacell markets its products and systems under various brand names, such as Fermacell® gypsum fiber boards, Fermacell Powerpanel® and Fermacell AESTUVER® fire protection products.

Since we commenced selling our products in Europe in fiscal year 2004, we have continued to work to grow demand for our products by building awareness among distributors, builders and contractors. Management believes that with the acquisition of Fermacell, the growth outlook in Europe for both fiber cement and fiber gypsum is favorable.

Seasonality

Our businesses are seasonal and typically follow activity levels in the building and construction industry. In the United States, the calendar quarters ending in December and March generally reflect reduced levels of building activity depending on weather conditions. In Australia and New Zealand, the calendar quarter ending in March is usually the quarter most affected by a slowdown due to summer holidays. In the Philippines, construction activity diminishes during the wet season from June through September and during the last half of December due to the slowdown in business activity over the holiday period. Also, general industry patterns can be affected by weather, economic conditions, industrial disputes and other factors. See “Section 3 – Risk Factors.”

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 10 |

| |

Raw Materials

The principal raw materials used in the manufacture of our fiber cement products are cellulose fiber (wood-based pulp), silica (sand), Portland cement and water. We have established supplier relationships for all of our raw materials across the various markets in which we operate, and we do not anticipate having difficulty in obtaining our required raw materials from these suppliers. The purchase price of these raw materials and other materials can fluctuate depending on the supply-demand situation at any given point in time.

We work hard to reduce the effect of both price fluctuations and supply interruptions by entering into contracts with qualified suppliers and through continuous internal improvements in both our products and manufacturing processes.

Cellulose Fiber

Reliable access to specialized, consistent quality, low cost pulp is critical to the production of fiber cement building materials. As a result of our many years of experience and expertise in the industry, we share our internal expertise with pulp producers in New Zealand, the United States, Canada and Chile to ensure they are able to provide us with a highly specialized and proprietary formula crucial to the reinforcing cement matrix of our fiber cement products. We have confidentiality agreements with our pulp producers, and we have obtained patents in the United States and in certain other countries covering certain unique aspects of our pulping formulas and processes that we believe cannot adequately be protected through confidentiality agreements. However, we cannot be assured that our intellectual property and other proprietary information will be protected in all cases. See “Section 3 – Risk Factors.”

Silica

High purity silica is sourced locally by the various production plants. In the majority of locations, we use silica sand as a silica source. In certain other locations, however, we process quartz rock and beneficiate silica sand to ensure the quality and consistency of this key raw material.

Cement

Cement is acquired in bulk from local suppliers. We continue to evaluate options on agreements with suppliers for the purchase of cement that can lock in our cement prices over longer periods of time.

Water

We use local water supplies and process all wastewater to comply with environmental requirements.

Sales, Marketing and Distribution

The principal markets for our fiber cement products are the United States, Australia, New Zealand, the Philippines, Canada, and parts of Europe, including the United Kingdom and France. In addition, in the past fiscal year, we have sold fiber cement products in many other markets, including Denmark, Germany, Hong Kong, the Middle East, various Pacific Islands and South Korea. Our brand name, customer education in comparative product advantages, differentiated product range and customer service, including technical advice and assistance, provide the basis for our marketing strategy.

We offer our customers support through a specialized fiber cement sales force and customer service infrastructure in the United States, Australia, New Zealand, the Philippines and Europe.

Our customer service infrastructure includes inbound customer service support coordinated nationally in each country, and is complemented by outbound telemarketing capability. Within each regional market, we

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 11 |

| |

provide sales and marketing support to building products dealers and lumber yards and also provide support directly to the customers of these distribution channels, principally homebuilders and building contractors.

We maintain dedicated regional sales management teams in our major sales territories, with our national sales managers and national account managers, together with regional sales managers and sales representatives, maintaining relationships with national and other major accounts. Our various sales forces, which in some instances manage specific product categories, include skilled trades people who provide on-site technical advice and assistance.

In the United States, we sell fiber cement products for new residential construction predominantly to distributors, which then sell these products to dealers or lumber yards. This two-step distribution process is supplemented with direct sales to dealers and lumber yards as a means of accelerating product penetration and sales. Repair and remodel products in the United States are typically sold through the large home center retailers and specialist distributors. Our products are distributed across the United States and Canada primarily by road and, to a lesser extent, by rail.

In Australia and New Zealand, both new construction and repair and remodel products are generally sold directly to distributor/hardware stores and lumber yards rather than through the two-step distribution process. In the Philippines, a network of thousands of small to medium size retail outlets sell our fiber cement products to consumers, builders and real estate developers, although in recent years, do-it-yourself type stores have started to enter the Philippines market. The physical distribution of our product in each country is primarily by road, rail or sea transport. Products manufactured in Australia, New Zealand and the Philippines are also exported to a number of markets in Asia, various Pacific Islands, and the Middle East by sea transport.

Despite the fact that distributors and dealers are generally our direct customers, we also aim to increase primary demand for our products by marketing our products directly to homeowners, architects and builders. We encourage them to specify and install our products because of the quality and craftsmanship of our products. This “pull through” strategy, in turn, assists us in expanding sales for our distribution network as distributors benefit from the increasing demand for our products.

Geographic expansion of our fiber cement business has occurred in markets where framed construction is prevalent for residential applications or where there are opportunities to change building practices from masonry to framed construction. Expansion is also possible where there are direct substitution opportunities irrespective of the methods of construction. Our entry into the Philippines is an example of the ability to substitute fiber cement for an alternative product (in this case plywood). With the exception of our current major markets, as well as Japan and certain rural areas in Asia, Scandinavia, and Eastern Europe, most markets in the world principally utilize masonry construction for external walls in residential construction. Accordingly, further geographic expansion depends substantially on our ability to provide alternative construction solutions and for those solutions to be accepted in those markets.

Dependence on Trade Secrets and Research and Development (“R&D”)

We pioneered the successful development of cellulose reinforced fiber cement and, since the early-1980s, have progressively introduced products developed as a result of our proprietary product formulation and process technology. The introduction of differentiated products is one of the core components of our global business strategy. This product differentiation strategy is supported by our significant investment in R&D activities.

We view spending on R&D as the key to sustaining our existing product leadership position, by providing a continuous pipeline of innovative new products and technologies with sustainable performance and design advantages over our competitors. Further, through our investments in new process technology or by modifying existing process technology, we aim to keep reducing our capital and operating costs and to find

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 12 |

| |

new ways to make existing and new products. As such, we expect to continue allocating significant funding to these endeavors. For fiscal years 2018, 2017 and 2016, our expenses for R&D were US$33.3 million, US$30.3 million and US$29.5 million, respectively.

Our current patent portfolio is based mainly on fiber cement compositions, associated manufacturing processes and the resulting products. Our non-patented technical intellectual property consists primarily of our operating and manufacturing know-how and raw material and operating equipment specifications, all of which are maintained as trade secret information. We have enhanced our abilities to effectively create, manage and utilize our intellectual property and have implemented a strategy that increasingly uses patenting and trade secret protection to protect and increase our competitive advantage.

In addition, we have a variety of industrial, commercial and financial contracts relating to our proprietary manufacturing processes. While we are dependent on the competitive advantage that these items provide as a whole, we are not dependent on any one of them individually and do not consider any one of them individually to be material. We do not materially rely on intellectual property licensed from any outside third parties. However, we cannot assure that our intellectual property and other proprietary information will be protected in all cases. In addition, if our R&D efforts fail to generate new, innovative products or processes, our overall profit margins may decrease and demand for our products may fall. See “Section 3 – Risk Factors.”

Governmental Regulation

As an Irish plc, we are governed by the Irish Companies Act 2014 and are also subject to all applicable European Union level legislation. We also operate under the regulatory requirements of numerous jurisdictions and organizations, including the ASX, ASIC, the NYSE, the SEC, the Irish Takeover Panel and various other federal, state, local and foreign rulemaking bodies. See “Section 3 – Constitution” for additional information regarding the Irish Companies Act 2014 and regulations to which we are subject.

Environmental, Health and Safety Regulation

Our operations and properties are subject to extensive federal, state, local and foreign environmental protection, health and safety laws, regulations and ordinances governing activities and operations that may have adverse environmental effects. As it relates to our operations, our manufacturing plants produce regulated materials, including waste water and air emissions. The waste water produced from our manufacturing plants is internally recycled and reused before eventually being discharged to publicly owned treatment works, a process which is monitored by us, as well as by regulators. In addition, we actively monitor air emissions and other regulated materials produced by our plants so as to ensure compliance with the various environmental regulations under which we operate.

Some environmental laws provide that a current or previous owner or operator of real property may be liable for the costs of investigation, removal or remediation of certain regulated materials on, under, or in that property or other impacted properties. In addition, persons who arrange, or are deemed to have arranged, for the disposal or treatment of certain regulated materials may also be liable for the costs of investigation, removal or remediation of the regulated materials at the disposal or treatment site, regardless of whether the affected site is owned or operated by such person. Environmental laws often impose liability whether or not the owner, operator, transporter or arranger knew of, or was responsible for, the presence of such regulated materials. Also, third parties may make claims against owners or operators of properties for personal injuries, property damage and/or for clean-up associated with releases of certain regulated materials pursuant to applicable environmental laws and common law tort theories, including strict liability.

In the past, from time to time, we have received notices of alleged discharges in excess of our water and air permit limits. In each case, and in compliance with our Environmental Policy, we have addressed the concerns raised in those notices, in part, through enhanced administrative controls and/or capital

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 13 |

| |

expenditures intended to prevent future discharges in excess of permitted levels and, on occasion, the payment of associated minor fines.

Environmental compliance costs in the future will depend, in part, on continued oversight of operations, expansion of operations and manufacturing activities, regulatory developments and future requirements that cannot presently be predicted.

Organizational Structure

JHI plc is incorporated and domiciled in Ireland and the table below sets forth our significant subsidiaries, all of which are wholly-owned by JHI plc, either directly or indirectly, as of 31 March 2018.

|

| | | | |

Name of Company | | Jurisdiction of Establishment | | Jurisdiction of Tax Residence |

James Hardie 117 Pty Ltd | | Australia | | Australia |

James Hardie Australia Pty Ltd | | Australia | | Australia |

James Hardie Building Products Inc. | | United States | | United States |

James Hardie Europe B.V. | | Netherlands | | Netherlands |

James Hardie Finance Holdings 1 Ltd | | Bermuda | | Ireland |

James Hardie Germany GmbH | | Germany | | Germany |

James Hardie Holdings Ltd | | Ireland | | Ireland |

James Hardie International Finance Designated Activity Company | | Ireland | | Ireland |

James Hardie International Group Ltd | | Ireland | | Ireland |

James Hardie International Holdings Ltd | | Ireland | | Ireland |

James Hardie New Zealand | | New Zealand | | New Zealand |

James Hardie NL1 B.V. | | Netherlands | | Netherlands |

James Hardie NL2 B.V. | | Netherlands | | Netherlands |

James Hardie NZ Holdings | | New Zealand | | New Zealand |

James Hardie NZ Holdings Ltd | | Bermuda | | New Zealand |

James Hardie North America Inc. | | United States | | United States |

James Hardie NV | | Netherlands | | Netherlands |

James Hardie Philippines Inc. | | Philippines | | Philippines |

James Hardie Research (Holdings) Pty Ltd | | Australia | | Australia |

James Hardie Research Pty Ltd | | Australia | | Australia |

James Hardie Research USA LLC | | United States | | United States |

James Hardie Technology Holdings 1 | | Ireland | | Ireland |

James Hardie Technology Holdings 2 | | Ireland | | Ireland |

James Hardie Technology Ltd | | Bermuda | | Ireland |

James Hardie U.S. Investments Sierra Inc. | | United States | | United States |

RCI Holdings Pty Ltd | | Australia | | Australia |

On 3 April 2018, we announced the completion of our acquisition of Fermacell and its subsidiaries. See “History and Development of the Company” in this Section of the Annual Report and Note 19 to our consolidated financial statements in Section 2.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 14 |

| |

Property, Plants and Equipment

We believe we have some of the largest and lowest cost fiber cement manufacturing plants across the United States, Australia, New Zealand and the Philippines, with our plants servicing both domestic and export markets. Our plants are ideally located to take advantage of established transportation networks, allowing us to distribute our products into key markets, while also providing easy access to key raw materials.

Manufacturing Capacity

At 31 March 2018, we had manufacturing facilities at the following locations:

|

| | | | | |

Plant Location | | Owned / Leased | | Nameplate Capacity (mmsf)1 |

United States2 | | | | |

Cleburne, Texas | | Owned | | 666 |

|

Peru, Illinois | | Owned | | 560 |

|

Plant City, Florida | | Owned | | 600 |

|

Pulaski, Virginia | | Owned | | 600 |

|

Reno, Nevada | | Owned | | 300 |

|

Tacoma, Washington | | Owned | 3 | 200 |

|

Waxahachie, Texas | | Owned | | 360 |

|

Fontana, California | | Owned | | 250 |

|

Summerville, South Carolina | | Owned | 4 | 190 |

|

Australia | | | | |

Rosehill, New South Wales | | Owned | | 180 |

|

Carole Park, Queensland | | Owned | 5 | 160 |

|

New Zealand | | | | |

Auckland | | Leased | 6 | 75 |

|

Philippines | | | | |

Cabuyao City | | Owned | 7 | 145 |

|

____________

| |

1 | The calculated annual nameplate capacity is based on management’s historical experience with our production process and is calculated assuming continuous operation, 24 hours per day, seven days per week, producing 5/16” medium density product at a targeted operating speed. No accepted industry standard exists for the calculation of our fiber cement manufacturing facility nameplate, design and utilization capacities. |

| |

2 | In the fourth quarter of fiscal year 2018, we announced a Greenfield capacity project in Prattville, Alabama with an expected commissioning date in the first half of fiscal year 2020. This project will add an additional 600 mmsf to our manufacturing capacity. This incremental capacity is not included in the table above. |

| |

3 | In the third quarter of fiscal year 2017, we announced a Greenfield capacity project at our Tacoma, Washington facility with an expected commissioning date in the first half of fiscal year 2019. This incremental capacity is not included in the table above. |

| |

4 | We suspended production at our Summerville, South Carolina location in November 2008. The plant was re-commissioned in the first quarter of fiscal year 2018. |

| |

5 | In the fourth quarter of fiscal year 2018, we announced an A$28.5 million (US$22.8 million) Brownfield expansion project at our Carole Park, Queensland facility with an expected commissioning date in the first quarter of fiscal year 2021. This incremental capacity is not included in the table above. |

| |

6 | We exercised our option to renew the Auckland leases for a further term of 10 years prior to the leases’ expiry on 22 March 2016. The Auckland leases now expire on 22 March 2026, at which time we have an option to renew them for a further term of 10 years expiring in March 2036. There is no option to purchase at the expiration of the leases. |

| |

7 | The land on which our Philippines fiber cement plant is located is owned by Ajempa Holding Inc. (“Ajempa”), a related party. Ajempa is 40% owned by our operating entity, James Hardie Philippines Inc., and 60% owned by the James Hardie Philippines Retirement Fund. James Hardie Philippines Inc. owns 100% of the fixed assets on the land owned by Ajempa. |

We are adding additional capacity in the Philippines with an estimated total cost of US$18.0 million and an expected completion date in the first quarter of fiscal year 2019. This incremental capacity is not included in the table above.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 15 |

| |

We continually evaluate the capacity required to service the US housing market, and as a result, to ensure we meet demand and achieve our market penetration objectives, we have completed and continue to start-up and commission several lines across our manufacturing network. For a discussion of significant active and recently completed capacity expansion projects, see “Capital Expenditures.”

Beginning in the fourth quarter of fiscal year 2016, management determined that for measuring the annual flat sheet design capacity of the fiber cement network, the calculation should incorporate our historical experience with certain factors such as demand, product mix of varying thickness and density, batch size, plant availability and differing production speeds multiplied by 24 hours per day, seven days per week. Additionally, commencing in the second quarter of fiscal year 2017, management adjusted the definition of plant availability pertaining to idled, non-commissioned, and start-up lines when determining annual flat sheet design capacity and capacity utilization. In the second quarter of fiscal year 2018, management adjusted the definition of production speeds and uptime expectations when determining annual flat sheet design capacity for the United States.

Based on the methodology noted above, for the year ended 31 March 2018, we had an annual flat sheet design capacity of 3,744 mmsf and 600 mmsf in the United States and Asia Pacific, respectively. It is important to note that annual design capacity does not necessarily reflect the actual capacity utilization rates of our manufacturing facilities, with actual utilization affected by factors such as demand, product mix, batch size, plant availability and production speeds. For fiscal year 2018, actual capacity utilization across our plants was an average of 90% and 92% in the United States and Asia Pacific, respectively.

Based on the methodology noted above, for the year ended 31 March 2017, we had an annual flat sheet design capacity of 3,284 mmsf and 619 mmsf in the United States and Asia Pacific, respectively. It is important to note that annual design capacity does not necessarily reflect the actual capacity utilization rates of our manufacturing facilities, with actual utilization affected by factors such as demand, product mix, batch size, plant availability and production speeds. For fiscal year 2017, actual capacity utilization across our plants was an average of 94% and 92% in the United States and Asia Pacific, respectively.

Finally, as a result of our completion of the Fermacell acquisition in April 2018, we expanded our manufacturing and production footprint with the addition of six Fermacell plants located in Calbe, Germany, Munchehof, Germany, Schraplau, Germany, Siglingen, Germany, Niftrik, The Netherlands and Orejo, Spain.

Mines

We lease silica quartz mine sites in Tacoma, Washington and Reno, Nevada. The lease for our quartz mine in Tacoma, Washington was renewed per the lease for another four year renewal term through February 2022 (with additional options to renew at that time). The lease for our silica quartz mine site in Reno, Nevada expires in January 2019. We also own property in Victorville, California which could be mined for silica. As of 30 April 2018, however, we have not begun to mine this site and have no immediate plans to do so. We continue to lease a parcel of land in Victorville, California adjacent to and for access to our owned property, as well as providing an equipment area for mining operations.

The recently acquired Fermacell business has an operating license for a mining facility in Schraplau, Germany, however no active mining is being undertaken, or allowed with respect to the former owner FELS-WERKE GmbH, and the mine is only being used for storage of material.

As a mine operator, we are required by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), and rules promulgated by the SEC implementing that section of the Dodd-Frank Act, to provide certain information concerning mine safety violations and other regulatory matters concerning the operation of our mines. During fiscal year 2018, we did not receive any notices, citations, orders, legal action or other communication from the US Department of Labor’s Mine Safety and Health

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 16 |

| |

Administration that would necessitate additional disclosure under Section 1503(a) of the Dodd-Frank Act. Similarly, we have not experienced any mining-related fatalities in our mining operations. There are currently no pending legal actions before the Federal Mine Safety and Health Review Commission related to our mining operations.

Capital Expenditures

We utilize a mix of operating cash flow and debt facilities to fund our capital expenditure projects and investments. We continuously invest in safety, equipment maintenance and upgrades, and capacity to ensure continued environmental compliance and operating effectiveness of our plants. The following table sets forth our capital expenditures for the three most recent fiscal years:

|

| | | | | | | | | | | | |

| | (Millions of US dollars) |

| | 2018 | | 2017 | | 2016 |

North America Fiber Cement | | $ | 182.5 |

| | $ | 76.1 |

| | $ | 40.3 |

|

International Fiber Cement | | 18.4 |

| | 24.4 |

| | 28.7 |

|

Other Businesses | | 2.0 |

| | 0.7 |

| | 2.3 |

|

R&D and Corporate | | 0.8 |

| | 0.7 |

| | 1.9 |

|

Total Capital Expenditures | | $ | 203.7 |

| | $ | 101.9 |

| | $ | 73.2 |

|

Significant active capital expenditures

At 31 March 2018, the following significant capital expenditures related to capacity projects remain in progress:

|

| | | | | | | | | | | | | | |

Project Description | | Approximate Investment (US millions) | | Investment to date (US millions) | | Project Start Date | | Expected Commission Date | | Expected Nameplate Capacity Increase1 |

Tacoma Greenfield expansion | | $ | 150.0 |

| | $ | 100.8 |

| | Q4 FY17 | | FY19 | | 8% |

Carole Park Brownfield expansion | | 22.8 |

| | 0.1 |

| | Q4FY18 | | FY21 | | 16% |

Philippines capacity expansion | | $ | 18.0 |

| | $ | 15.2 |

| | Q4 FY16 | | FY19 | | 9% |

____________

| |

1 | The expected capacity increase is based on management’s historical experience with our production process and is calculated assuming continuous operation, 24 hours per day, seven days per week, producing 5/16” medium density product at a targeted operating speed. It does not take into account factors such as product mix with varying thickness and density, batch size, plant availability and production speeds. Expected increase in capacity related to Tacoma Greenfield expansion represents expected increase in North America nameplate capacity as of 31 March 2018. Expected increases in Carole Park Brownfield expansion and Philippines capacity expansion represent expected increase in Asia Pacific's nameplate capacity as of 31 March 2018. |

During fiscal year 2018, we also continued the planning of our Prattville, Alabama facility, which is expected to be commissioned in the first half of fiscal year 2020. Additionally, on 22 May 2018, we announced that this greenfield expansion project will add an additional 600 mmsf to our manufacturing capacity at an estimated total cost of US$240.0 million.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 17 |

| |

Significant completed capital expenditure projects

The following is a list of significant capital expenditure projects we have invested in over the three most recent fiscal years:

|

| | | | | | |

Project Description | | Total Investment (US Millions) | | Fiscal Year of Expenditure |

Carole Park land and building purchase and capacity expansion | | $ | 85.3 |

| | FY14 - FY16 |

Plant City SM4 - 3rd operating sheet machine | | 71.2 |

| | FY14 - FY17 |

Cleburne - 3rd sheet machine | | 40.8 |

| | FY14 - FY17 |

Waxahachie lease buyout | | 16.5 |

| | FY17 |

Summerville recommissioning | | $ | 15.7 |

| | FY17 - FY18 |

Capital Divestitures

During the three most recent fiscal years, we did not make any material capital divestitures. On 30 June 2015, we finalized the sale of our Australian Pipes business. Additionally, on 1 June 2015 we finalized the sale of our Blandon, Pennsylvania location. We do not consider the disposition of the pipes business or the sale of Blandon, Pennsylvania location to constitute material divestitures or strategic shifts in the nature of our operations.

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 18 |

| |

DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES

James Hardie Executive Team

Our management is overseen by our executive team, whose members cover the key areas of fiber cement R&D, production, manufacturing, human resources, marketing, investor relations, finance and legal.

Members of our executive team at 30 April 2018 (in alphabetical order) are: |

| |

Joe Blasko BSFS, JD General Counsel and Chief Compliance Officer Age 51 |

| Joe Blasko joined James Hardie as General Counsel and Chief Compliance Officer in June 2011. Before joining James Hardie, Mr Blasko was Assistant General Counsel, and later, the General Counsel at Liebert Corporation, an Emerson Network Power Systems company and wholly-owned subsidiary of Emerson Electric Co. In his four years with Liebert/Emerson, Mr Blasko was responsible for establishing the legal department in Columbus, Ohio, managing and overseeing all legal matters and working closely with the executive management team. In this role, Mr Blasko also had global responsibilities which required expertise across multiple jurisdictions.

|

From 2004 to 2006, Mr Blasko was Associate General Counsel at The Scotts Miracle-Gro Company, serving as the effective “general counsel” to numerous corporate divisions within the organization. From 1997 to 2004, Mr Blasko gained considerable regulatory and litigation expertise working at Vorys, Sater, Seymour and Pease LLP in Ohio. Mr Blasko has a Juris Doctor from Case Western Reserve University in Cleveland, Ohio, USA and a Bachelor of Science in Foreign Service from Georgetown University, USA, with a specialty in International Relations, Law and Organizations. |

|

| |

Sean Gadd BEng, MBA Executive Vice President, Markets and Segments Age 45 |

| Sean Gadd joined James Hardie in 2004 as a Regional Engineering Manager for the Asia Pacific business, and progressed to Plant Manager for both the Carole Park and Rosehill facilities in Australia. Mr Gadd then moved to the US in 2006 to take the role of Manufacturing Manager for Trim and various manufacturing facilities across the US. In 2009, Mr Gadd ran the US trim business for James Hardie with responsibility for both Manufacturing and Sales, followed by a brief assignment leading Supply Chain. In 2012, Mr Gadd was promoted to the role of Vice President of Sales for Western USA and Canada. Over the next year, his role was expanded to include the Midwest and Northeast of the USA.

|

Mr Gadd was appointed Executive General Manager in September 2013 with full responsibility for the Northern Division. In October 2015, he was appointed Executive Vice President, Markets and Segments, North America with responsibility for Strategic Marketing and Development. Mr Gadd has a Bachelor of Engineering in Manufacturing Management and an executive MBA from the Australian Graduate School of Management, Australia. |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 19 |

| |

|

| |

Louis Gries BSc, MBA Chief Executive Officer Age 64 |

| Louis Gries joined James Hardie as Manager of the Fontana fiber cement plant in California in February 1991 and was appointed President of James Hardie Building Products, Inc. in December 1993. Mr Gries became Executive Vice President – Operations in January 2003, responsible for operations, sales and marketing in our businesses in the Americas, Asia Pacific and Europe. He was appointed Interim Chief Executive Officer (“CEO”) in October 2004 and became CEO in February 2005. In addition to being the Company’s CEO, Mr Gries is responsible for managing the Company’s fiber cement operations in North America. |

Before he joined James Hardie, Mr Gries worked for 13 years for USG Corp, including a variety of roles in research, plant quality and production, and product and plant management. Mr Gries has a Bachelor of Science in Mathematics from the University of Illinois, USA and an MBA from California State University, Long Beach, USA. |

|

| |

Ryan Kilcullen BSc, MS Executive Vice President – Operations Age 37 |

| Ryan Kilcullen joined James Hardie in 2007 as a PcI/PdI Engineer. Since then, he has worked for the Company in various manufacturing and supply chain roles including Process Engineer, Production Manager, and Supply Chain Engineer. In 2012, he became Supply Chain Manager, ColorPlus Business Unit, responsible for the end-to-end design and performance of our ColorPlus product line supply chain. In 2013, he became responsible for North American Supply Chain operations, with responsibilities that included Procurement, Network Planning, Production Planning, Transportation, Distribution Management, Customer Service, and Inside Sales. In June 2015, he was appointed Vice President – Central Operations, responsible for the Company’s Supply Chain Operations and Centralized Manufacturing functions. |

In August 2016, he was appointed Executive Vice President – Operations, responsible for the Company’s Supply Chain, Manufacturing, Engineering and Environmental, Health & Safety Operations. Mr Kilcullen has a Bachelor of Science in Industrial Engineering from Rensselaer Polytechnic Institute and a Master of Engineering in Logistics from Massachusetts Institute of Technology. |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 20 |

| |

|

| |

Matthew Marsh BA, MBA Chief Financial Officer and Executive Vice President – Corporate Age 43 |

| Matthew Marsh joined James Hardie as Chief Financial Officer (“CFO”) in June 2013. As CFO he oversees the Company’s overall financial activities, including accounting, tax, treasury, performance and competitor analysis, internal audit and financial operations. Effective 16 October 2015, Mr Marsh’s role was expanded to include the role of Executive Vice President – Corporate. In this role, Mr Marsh continues his oversight of the Company’s overall financial management in addition to the oversight of James Hardie’s information systems, legal and compliance, and investor and media relations functions. |

After a 16-year career at General Electric Company (“GE”), Mr Marsh brings a strong background in financial management. Before joining James Hardie, Mr Marsh most recently served as CFO of GE Healthcare’s IT business. Prior to being named CFO of GE Healthcare IT, Mr Marsh oversaw the finance operations for GE Healthcare’s US Healthcare Systems and US Diagnostic Imaging businesses. Prior to those appointments, Mr Marsh traveled globally with the GE Internal Audit Staff gaining extensive experience in several industries including appliances, information services, distribution and supply, aviation, plastics, financial services, capital markets and healthcare, across more than twenty countries. Mr Marsh has graduated from GE’s Financial Management Program (FMP). Mr Marsh has a Bachelor of Arts in Economics and Public Affairs from Syracuse University, USA and an MBA from University of Chicago’s Booth School of Business, USA. |

|

| | | | |

Dave Merkley BSc (Construction) Executive Vice President, Manufacturing and Engineering Age 55 |

| Dave Merkley first joined James Hardie in 1994 as Plant Manager of the Fontana, California facility in the United States. Mr Merkley has held a number of roles with the Company including US R&D Manager and US Manufacturing Manager, before being promoted to the position of Executive Vice President, Operations and Manufacturing with global responsibility in 2002. In 2006, Mr Merkley left James Hardie and worked as a consultant in the building products industry, gaining experience in composite building material and wood polymer composites decking and fencing. Mr Merkley rejoined James Hardie in October 2016 and was promoted to the role of Executive Vice President, Manufacturing and Engineering in November 2017.

|

Prior to joining James Hardie in 1994, Mr Merkley held various engineering positions in the civil construction industry, including heavy highway and infrastructure construction. Collectively Mr Merkley has over 30 years relevant industry experience and holds a Bachelor of Science in Construction from Arizona State University. |

|

| |

| |

James Hardie 2018 Annual Report on Form 20-F | 21 |

| |

|

| |

Jason Miele, BA Vice President, Investor and Media Relations Age 41 |

| Jason Miele was appointed to the position of Vice President – Investor and Media Relations in February 2017. Mr Miele has responsibility for overseeing the Company’s investor relations strategy and successful interface with external audiences, communicating the Company’s business strategy and its financial performance to various stakeholders including shareholders, investment analysts, and the financial media. Mr Miele has 20 years of relevant professional experience, including 11 years of experience with James Hardie, where he has served in various finance and operational support roles, most recently as James Hardie’s Group Controller, a position he has held since 2013. |

Mr Miele has a Bachelor’s Degree from the University of California at Santa Barbara, where he graduated with a degree in Business Economics with an emphasis in Accounting. |

|

| |