Exhibit 99.8

|

||||

| KPMG Actuarial Pty Ltd Australian Financial Services Licence No. 392050 10 Shelley Street Sydney NSW 2000

PO Box H67 Australia Square NSW 1215 Australia |

ABN: 91 144 686 046 Telephone: +61 2 9335 7000 Facsimile: +61 2 9335 7001 DX: 1056 Sydney www.kpmg.com.au |

23 May 2013

Narreda Grimley

General Manager

Asbestos Injuries Compensation Fund Limited

Suite 1, Level 7, 233 Castlereagh Street

Sydney NSW 2000

| Cc | Russell Chenu, Chief Financial Officer, James Hardie Industries plc |

Paul Miller, General Counsel, Department of Premier and Cabinet, The State of

New South Wales

The Board of Directors, Asbestos Injuries Compensation Fund Limited

Dear Narreda

VALUATION OF ASBESTOS-RELATED DISEASE LIABILITIES OF FORMER JAMES HARDIE ENTITIES (“THE LIABLE ENTITIES”) TO BE MET BY THE AICF TRUST

We are pleased to provide you with our actuarial valuation report relating to the asbestos-related disease liabilities of the Liable Entities which are to be met by the AICF Trust.

The report is effective as at 31 March 2013 and has taken into account claims data and information provided to us by AICFL as at 31 March 2013.

If you have any questions with respect to the contents of this report, please do not hesitate to contact us.

Yours sincerely

|

| |

| Neil Donlevy MA FIA FIAA | Jefferson Gibbs BSc FIA FIAA | |

| Executive, KPMG Actuarial Pty Ltd | Executive, KPMG Actuarial Pty Ltd | |

| Fellow of the Institute of Actuaries (London) | Fellow of the Institute of Actuaries (London) | |

| Fellow of the Institute of Actuaries of Australia | Fellow of the Institute of Actuaries of Australia | |

© 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights

reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of

KPMG International. Liability limited by a scheme approved under Professional Standards Legislation.

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Table of Contents

| Executive Summary |

i | |||||||

| 1 | Scope and Purpose |

1 | ||||||

| 1.1 | Introduction |

1 | ||||||

| 1.2 | Scope of report |

2 | ||||||

| 1.3 | Areas of potential exposure |

6 | ||||||

| 1.4 | Data reliances and limitations |

9 | ||||||

| 1.5 | Uncertainty |

9 | ||||||

| 1.6 | Distribution and use |

9 | ||||||

| 1.7 | Date labelling convention used in this Report |

10 | ||||||

| 1.8 | Author of the report |

10 | ||||||

| 1.9 | Professional standards and compliance |

10 | ||||||

| 1.10 | Control processes and review |

11 | ||||||

| 1.11 | Funding position of the AICF Trust |

11 | ||||||

| 1.12 | Basis of preparation of Report |

11 | ||||||

| 2 | Data |

12 | ||||||

| 2.1 | Data provided to KPMG Actuarial |

12 | ||||||

| 2.2 | Data limitations |

12 | ||||||

| 2.3 | Data reconciliation and testing |

12 | ||||||

| 2.4 | Data conclusion |

15 | ||||||

| 3 | Valuation Methodology and Approach |

17 | ||||||

| 3.1 | Previous valuation work and methodology changes |

17 | ||||||

| 3.2 | Overview of current methodology |

17 | ||||||

| 3.3 | Disease type and class subdivision |

19 | ||||||

| 3.4 | Numbers of future claims notifications |

21 | ||||||

| 3.5 | Incidence of claim settlements from future claim notifications |

25 | ||||||

| 3.6 | Average claim costs of IBNR claims |

26 | ||||||

| 3.7 | Proportion of claims settled for nil amounts |

27 | ||||||

| 3.8 | Pending claims |

27 | ||||||

| 3.9 | Insurance Recoveries |

30 | ||||||

| 3.10 | Cross-claim recoveries |

34 | ||||||

| 3.11 | Discounting cashflows |

35 | ||||||

| 4 | Claims Experience – Claim Numbers |

36 | ||||||

| 4.1 | Overview |

36 | ||||||

| 4.2 | Mesothelioma claims |

37 | ||||||

| 4.3 | Asbestosis claims |

41 | ||||||

| 4.4 | Lung cancer claims |

42 | ||||||

| 4.5 | ARPD & Other claims |

42 | ||||||

| 4.6 | Workers Compensation and wharf claims |

42 | ||||||

| 4.7 | Summary of base claims numbers assumptions |

43 | ||||||

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

i |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| 4.8 | Exposure information |

44 | ||||||

| 4.9 | Latency period of reported claims |

46 | ||||||

| 4.10 | Modelled peak year of claims and estimated future claim notifications |

51 | ||||||

| 4.11 | Baryulgil |

55 | ||||||

| 5 | Claims Experience – Average Claims Costs |

56 | ||||||

| 5.1 | Overview |

56 | ||||||

| 5.2 | Mesothelioma claims |

57 | ||||||

| 5.3 | Asbestosis claims |

58 | ||||||

| 5.4 | Lung cancer claims |

59 | ||||||

| 5.5 | ARPD & Other claims |

60 | ||||||

| 5.6 | Workers Compensation claims |

61 | ||||||

| 5.7 | Wharf claims |

62 | ||||||

| 5.8 | Large claim size and incidence rates |

63 | ||||||

| 5.9 | Summary assumptions |

65 | ||||||

| 6 | Claims Experience – Nil Settlement Rates |

66 | ||||||

| 6.1 | Overview |

66 | ||||||

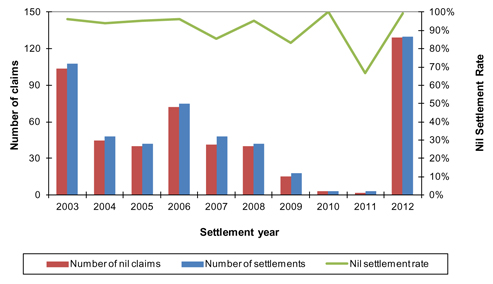

| 6.2 | Mesothelioma claims |

67 | ||||||

| 6.3 | Asbestosis claims |

68 | ||||||

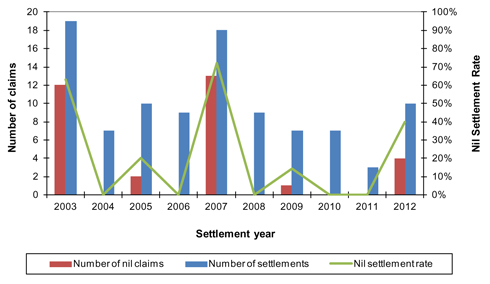

| 6.4 | Lung cancer claims |

69 | ||||||

| 6.5 | ARPD & Other claims |

70 | ||||||

| 6.6 | Workers Compensation claims |

71 | ||||||

| 6.7 | Wharf claims |

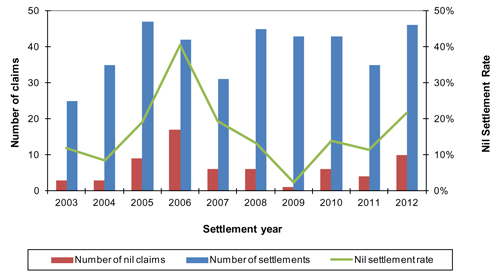

72 | ||||||

| 6.8 | Summary assumptions |

73 | ||||||

| 7 | Economic and Other Assumptions |

74 | ||||||

| 7.1 | Overview |

74 | ||||||

| 7.2 | Claims inflation |

74 | ||||||

| 7.3 | Superimposed inflation |

80 | ||||||

| 7.4 | Summary of claims inflation assumptions |

83 | ||||||

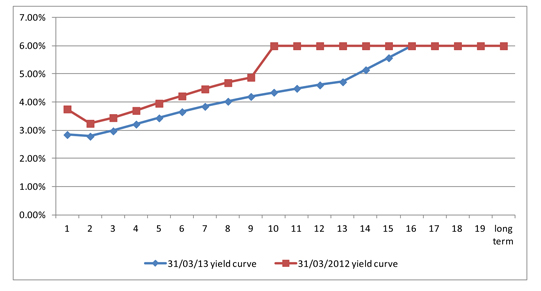

| 7.5 | Discount rates: Commonwealth bond zero coupon yields |

83 | ||||||

| 7.6 | Cross-claim recovery rates |

85 | ||||||

| 7.7 | Settlement Patterns |

86 | ||||||

| 8 | Valuation Results |

88 | ||||||

| 8.1 | Central estimate liability |

88 | ||||||

| 8.2 | Comparison with previous valuation |

89 | ||||||

| 8.3 | Cashflow projections |

91 | ||||||

| 8.4 | Amended Final Funding Agreement calculations |

93 | ||||||

| 8.5 | Insurance Recoveries |

94 | ||||||

| 8.6 | Accounting liability calculations: James Hardie |

95 | ||||||

| 9 | Uncertainty |

96 | ||||||

| 9.1 | Overview |

96 | ||||||

| 9.2 | Sensitivity testing |

97 | ||||||

| 9.3 | Results of sensitivity testing |

98 |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

ii |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| Tables | ||||

| Table 2.1: Grouping of financial data from claims and accounting databases |

14 | |||

| Table 2.2: Comparison of amounts from claims and accounting databases ($m) |

15 | |||

| Table 3.1: Change in cost of claims during 2012/13 financial year ($m) – claim award component only |

29 | |||

| Table 4.1: Number of claims reported annually |

36 | |||

| Table 4.2: Claim numbers experience and assumptions for 2013/14 |

43 | |||

| Table 4.3: Assumed underlying latency distribution parameters from average date of exposure to date of notification |

50 | |||

| Table 4.4: Modelled peak year of claim notifications |

51 | |||

| Table 5.1: Average attritional non-nil claim award (inflated to mid 2012/13 money terms) |

56 | |||

| Table 5.2: Average mesothelioma claims assumptions |

57 | |||

| Table 5.3: Average asbestosis claims assumptions |

58 | |||

| Table 5.4: Average lung cancer claims assumptions |

59 | |||

| Table 5.5: Average ARPD & Other claims assumptions |

60 | |||

| Table 5.6: Average Workers Compensation claims assumptions |

61 | |||

| Table 5.7: Average wharf claims assumptions |

62 | |||

| Table 5.8: Summary average claim cost assumptions |

65 | |||

| Table 6.1: Nil settlement rates |

66 | |||

| Table 6.2: Summary nil settlement rate assumptions |

73 | |||

| Table 7.1: Claims inflation assumptions |

83 | |||

| Table 7.2: Zero coupon yield curve by duration |

84 | |||

| Table 7.3: Settlement pattern of claims awards by delay from claim reporting |

87 | |||

| Table 8.1: Comparison of central estimate of liabilities |

88 | |||

| Table 8.2: Amended Final Funding Agreement calculations |

93 | |||

| Table 8.3: Insurance recoveries at 31 March 2013 |

94 | |||

| Table 9.1: Summary results of sensitivity analysis |

100 | |||

| Figures | ||||

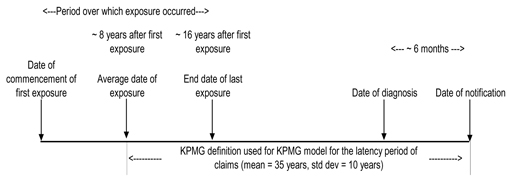

| Figure 3.1: Illustration of timeline of exposure, latency and claim reporting (example shown is for mesothelioma) |

22 | |||

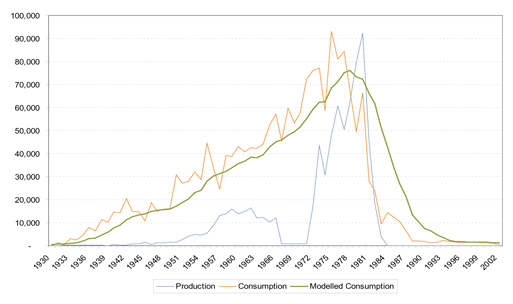

| Figure 3.2: Consumption and production indices – Australia 1930-2002 |

23 | |||

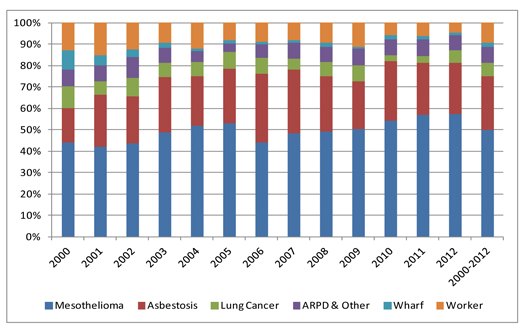

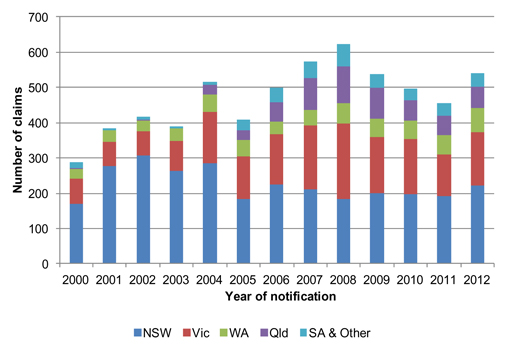

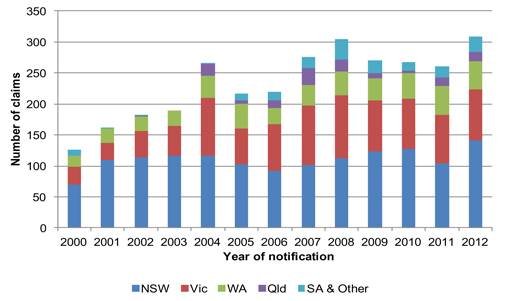

| Figure 4.1: Proportion of claims by disease type |

36 | |||

| Figure 4.2: Mix of claims by state (all disease types) |

37 | |||

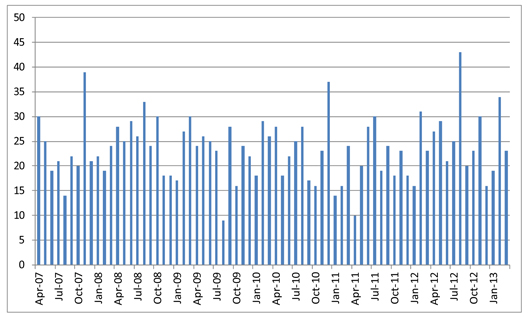

| Figure 4.3: Monthly notifications of mesothelioma claims |

38 | |||

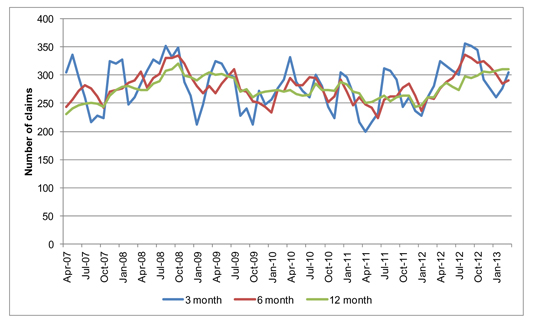

| Figure 4.4: Rolling annualised averages of mesothelioma claim notifications |

39 | |||

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

iii |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| Figure 4.5: Number of mesothelioma claims by state |

40 | |||

| Figure 4.6: Mix of claims by duration of exposure (years) |

44 | |||

| Figure 4.7: Exposure (person-years) of all Liable Entities’ claimants to date |

45 | |||

| Figure 4.8: Exposure (person years) of all claimants to date by report year and exposure period |

46 | |||

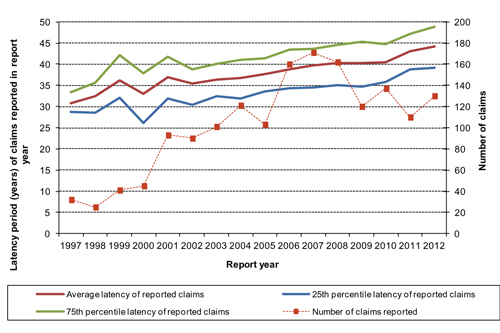

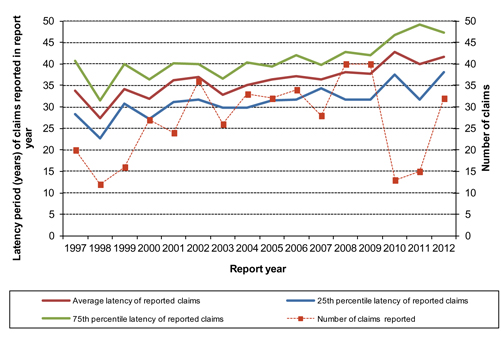

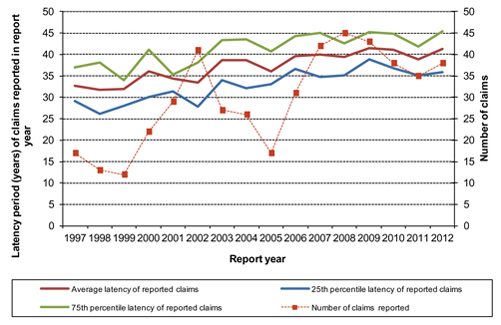

| Figure 4.9: Latency of mesothelioma claims |

47 | |||

| Figure 4.10: Latency of asbestosis claims |

48 | |||

| Figure 4.11: Latency of lung cancer claims |

49 | |||

| Figure 4.12: Latency of ARPD & Other claims |

49 | |||

| Figure 4.13: Projected mesothelioma claim numbers |

53 | |||

| Figure 4.14: Expected future claim notifications by disease type |

54 | |||

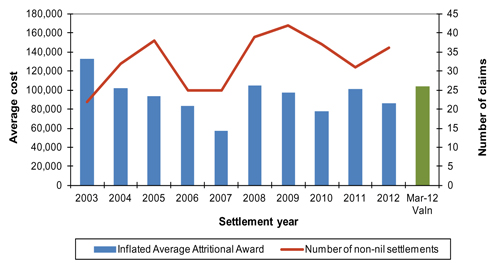

| Figure 5.1: Average attritional awards (inflated to mid 2012/13 money terms) and number of non-nil claims settlements for mesothelioma claims (excluding large claims) |

57 | |||

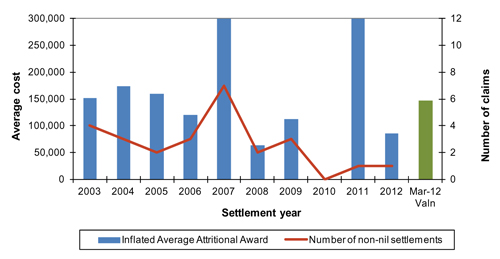

| Figure 5.2: Average awards (inflated to mid 2012/13 money terms) and number of non-nil claims settlements for asbestosis claims |

58 | |||

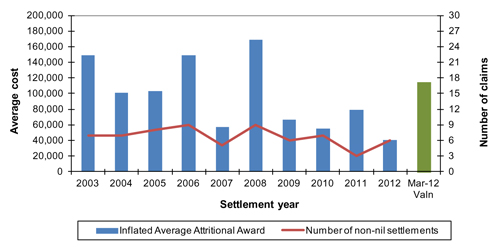

| Figure 5.3: Average awards (inflated to mid 2012/13 money terms) and number of non-nil claims settlements for lung cancer claims |

59 | |||

| Figure 5.4: Average awards (inflated to mid 2012/13 money terms) and number of non-nil claims settlements for ARPD & Other claims |

60 | |||

| Figure 5.5: Average awards (inflated to mid 2012/13 money terms) and number of non-nil claims settlements for Workers Compensation claims |

61 | |||

| Figure 5.6: Average awards (inflated to mid 2012/13 money terms) and number of non-nil claims settlements for wharf claims |

62 | |||

| Figure 5.7: Distribution of individual large claims by settlement year |

63 | |||

| Figure 5.8: Number of large claims by year of notification |

64 | |||

| Figure 6.1: Mesothelioma nil claims experience |

67 | |||

| Figure 6.2: Asbestosis nil claims experience |

68 | |||

| Figure 6.3: Lung cancer nil claims experience |

69 | |||

| Figure 6.4: ARPD & Other nil claims experience |

70 | |||

| Figure 6.5: Workers Compensation nil claims experience |

71 | |||

| Figure 6.6: Wharf nil claims experience |

72 | |||

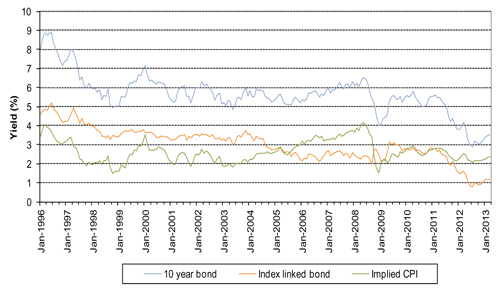

| Figure 7.1: Trends in Bond Yields |

75 | |||

| Figure 7.2: Trends in CPI and AWOTE |

76 | |||

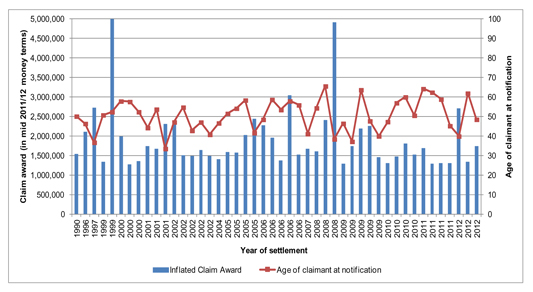

| Figure 7.3: Age profile of mesothelioma claimants by report year |

78 | |||

| Figure 7.4: Average mesothelioma claim settlement amounts by decade of age |

79 | |||

| Figure 7.5: Average mesothelioma awards of the Liable Entities (uninflated) |

82 | |||

| Figure 7.6: Zero coupon yield curve by duration |

85 | |||

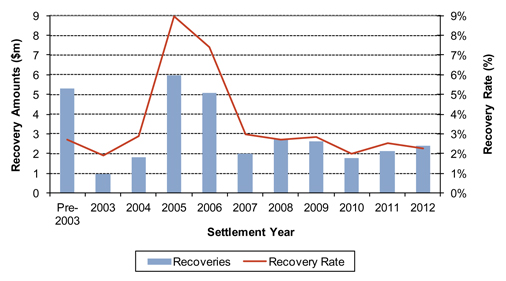

| Figure 7.7: Cross-claim recovery experience |

86 | |||

| Figure 7.8: Settlement pattern derivation for mesothelioma claims: paid as % of ultimate cost |

87 |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

iv |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| Figure 7.9: Settlement pattern derivation for non-mesothelioma claims: paid as % of ultimate cost |

87 | |||||

| Figure 8.1: Analysis of change in central estimate liability |

90 | |||||

| Figure 8.2: Historical claim-related expenditure of the Liable Entities |

91 | |||||

| Figure 8.3: Annual cashflow projections – inflated and undiscounted ($m) |

92 | |||||

| Figure 9.1: Sensitivity testing results – Impact around the Discounted Central Estimate (in $m) |

99 | |||||

| Appendices | ||||||

| A |

Credit rating default rates by duration |

102 | ||||

| B |

Projected inflated and undiscounted cashflows ($m) |

103 | ||||

| C |

Projected inflated and discounted cashflows ($m) |

104 | ||||

| D |

Derivation of US GAAP net accounting liability of James Hardie |

105 | ||||

| E |

Allocation of central estimate liabilities to AICFL entities |

107 | ||||

| F |

Australian asbestos consumption and production data: 1930-2002 |

108 | ||||

| G |

Data provided by AICFL |

109 | ||||

| H |

Glossary of terms used in the AFFA |

111 | ||||

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

v |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Executive Summary

Important Note: Basis of Report

This valuation report (“the Report”) has been prepared by KPMG Actuarial Pty Ltd (ABN 91 144 686 046) (“KPMG Actuarial”) in accordance with an “Amended and Restated Final Funding Agreement in respect of the provision of long-term funding for compensation arrangements for certain victims of Asbestos-related diseases in Australia” (hereafter referred to as the “the Amended Final Funding Agreement”) between James Hardie Industries NV (now known as James Hardie Industries plc) (hereafter referred to as “James Hardie”), James Hardie 117 Pty Limited, the State of New South Wales and Asbestos Injuries Compensation Fund Limited (“AICFL”) which was signed on 21 November 2006.

This Report is intended to meet the requirements of the Amended Final Funding Agreement and values the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust.

This Report is not intended to be used for any other purpose and may not be suitable, and should not be used, for any other purpose. Opinions and estimates contained in the Report constitute our judgment as of the date of the Report.

The information contained in this Report is of a general nature and is not intended to address the objectives, financial situation or needs of any particular individual or entity. It is provided for information purposes only and does not constitute, nor should it be regarded in any manner whatsoever as, advice and is not intended to influence a person in making a decision in relation to any financial product or an interest in a financial product. No one should act on the information contained in this Report without obtaining appropriate professional advice after a thorough examination of the accuracy and appropriateness of the information contained in this Report having regard to their objectives, financial situation and needs.

In preparing the Report, KPMG Actuarial has relied on information supplied to it from various sources and has assumed that the information is accurate and complete in all material respects. KPMG Actuarial has not independently verified the accuracy or completeness of the data and information used for this Report.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

i |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Except insofar as liability under statute cannot be excluded, KPMG Actuarial, its executives, directors, employees and agents will not be held liable for any loss or damage of any kind arising as a consequence of any use of the Report or purported reliance on the Report including any errors in, or omissions from, the valuation models.

The Report must be read in its entirety. Individual sections of the Report, including the Executive Summary, could be misleading if considered in isolation. In particular, the opinions expressed in the Report are based on a number of assumptions and qualifications which are set out in the full Report.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

ii |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Introduction

The Amended Final Funding Agreement requires the completion of an Annual Actuarial Report evaluating the potential asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust. KPMG Actuarial has been retained by AICFL to provide this actuarial valuation report as required under the Amended Final Funding Agreement and this is detailed in our Engagement Letter dated 15 November 2012.

The Liable Entities are defined as being the following entities:

| • | Amaca Pty Ltd (formerly James Hardie & Coy); |

| • | Amaba Pty Ltd (formerly Jsekarb, James Hardie Brakes and Better Brakes); and |

| • | ABN60 Pty Ltd (formerly James Hardie Industries Ltd). |

In addition, the liability for Baryulgil claims is deemed to be a liability of Amaca by virtue of the James Hardie (Civil Liability) Act 2005 (NSW). Under Part 4 of that Act, Amaca is liable for the “Marlew Asbestos Claims” or “Marlew Contribution Claims” as defined in that Act.

Our valuation is on a central estimate basis and is intended to be effective as at 31 March 2013. It has been based on claims data and information as at 31 March 2013 provided to us by AICFL.

Overview of Recent Claims Experience and comparison with previous valuation projections

In this section we compare the actual experience in 2012/13 (referred to in the following tables as “FY13 Actual”) with the projections for 2012/13 that were contained within our previous valuation report at 31 March 2012. We will refer to these projections for 2012/13 as “FY13 Expected” in the tables that follow.

Claim numbers

The number of mesothelioma claims reported has shown an increase in the year. There have been 310 claims reported in 2012/13. This compares to 260 claims reported in 2011/12, 268 claims reported in 2010/11 and 270 claims reported in 2009/10.

For non-mesothelioma claims, there have been 232 claims reported in 2012/13 compared to 196 claims reported in 2011/12, 228 claims reported in 2010/11 and 267 claims reported in 2009/10. This increase is predominantly due to a significant increase in reporting activity for asbestosis claims and lung cancer claims.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

iii |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

The following table shows the comparison of actual experience with that which had been forecast at the previous valuation.

Table E.1. Comparison of claim numbers

| FY13 Actual |

FY13 Expected |

Ratio of Actual to Expected (%) |

FY12 Actual |

|||||||||||||

| Mesothelioma |

310 | 276 | 112 | % | 260 | |||||||||||

| Asbestosis |

130 | 126 | 103 | % | 110 | |||||||||||

| Lung Cancer |

32 | 18 | 178 | % | 15 | |||||||||||

| ARPD & Other |

38 | 42 | 90 | % | 36 | |||||||||||

| Wharf |

6 | 6 | 100 | % | 6 | |||||||||||

| Workers |

26 | 36 | 72 | % | 29 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

542 | 504 | 108 | % | 456 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Average Claim Awards

Average claims awards in 2012/13 have typically been in line with, or lower than, expectations.

There have been three large mesothelioma claim settlements (being claims in excess of $1m in 2006/07 money terms) in 2012/13. This is below our allowance of 5.5 large claims. Total claims expenditure on large claims has been 47% below expectations, reflecting the lower number of large claims.

The following table shows the comparison of actual experience with that which had been forecast at the previous valuation.

Table E.2. Comparison of average claim size of non-nil claims

| FY13 Actual ($) |

FY13 Expected ($) |

Ratio of Actual to Expected (%) |

FY12 Actual ($) | |||||

| Mesothelioma |

286,641 | 311,800 | 92% | 283,234 | ||||

| Asbestosis |

121,187 | 114,600 | 106% | 108,862 | ||||

| Lung Cancer |

115,523 | 143,900 | 80% | 125,042 | ||||

| ARPD & Other |

86,358 | 103,900 | 83% | 97,571 | ||||

| Wharf |

40,601 | 114,600 | 35% | 76,090 | ||||

| Workers |

85,000 | 146,600 | 58% | 900,000 | ||||

| Mesothelioma Large Claims Costs |

3 claims @ $1,929,500 = $5,788,500 |

5.5 claims @ $1,972,000 = $10,847,000 |

53% | 4 claims @ $1,337,800 = $5,351,200 |

Note: FY12 Actual values are expressed in 2011/12 money terms. FY13 Actual values and FY13 Expected values are expressed in 2012/13 money terms.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

iv |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

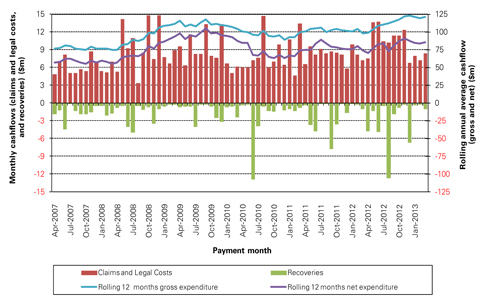

Cashflow expenditure: gross and net

Gross cashflow expenditure, at $121.3m, was 1% below expectations.

Net cashflow expenditure, at $85.6m, was 20% below expectations.

Table E.3. Comparison of cashflow

| FY13 YTD Actual ($M) |

FY13 YTD Expected ($M) |

Ratio of Actual to Expected (%) |

FY12 YTD Actual ($M) |

|||||||||||||

| Gross Cashflow |

121.3 | 122.2 | 99 | % | 99.1 | |||||||||||

| Insurance and Other Recoveries |

(11.8 | ) | (14.9 | ) | 79 | % | (12.4 | ) | ||||||||

| Insurance recoveries from HIH (under 562A(4)) and from commutations |

(23.9 | ) | 0.0 | n/a | (11.5 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net Cashflow |

85.6 | 107.3 | 80 | % | 75.2 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Insurance and Other Recoveries have been considerably higher than expected. This is due to proceeds from insurance collections from HIH and associated entities as a result of successful application of Section 562A(4) and other commutation proceeds.

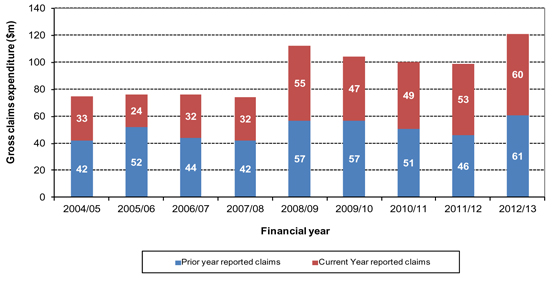

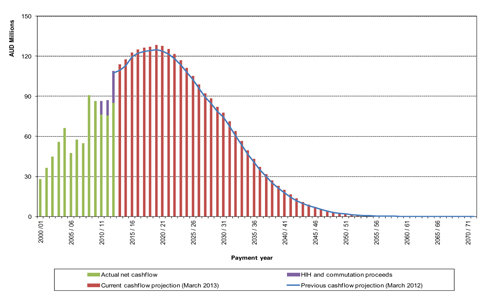

The following chart shows the composition of the gross cashflow between current and prior years’ reported claims over the past nine financial years.

Figure E.1. Composition of gross cashflow between current and prior years’ reported claims

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

v |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Payments in relation to claims reported in the financial year have shown an increase compared with the previous year. This is predominantly due to the higher number of mesothelioma claims reported in the year and which have been settled in the year.

Payments in relation to prior years’ reported claims have shown a more material increase and are a consequence of the higher numbers of claims settled.

The previous observations we have made in relation to the average claim sizes being better than expected and being broadly in line with, or lower than, the previous year further demonstrates that the higher claim payments being made are substantially a consequence of the increased numbers of claims settled.

As a consequence of the settlement activity that occurred in 2012/13, the number of claims that have been received and not yet settled (“pending claims”) are at their lowest levels since the formation of AICF.

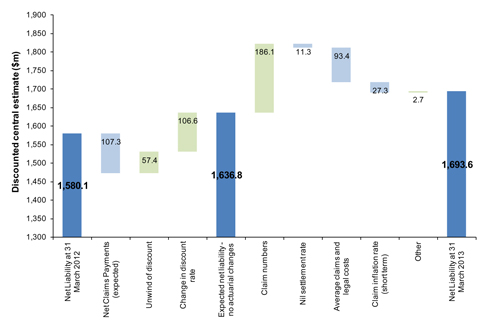

Liability Assessment

At 31 March 2013, our projected central estimate of the liabilities of the Liable Entities (the Discounted Central Estimate) to be met by the AICF Trust is $1,693.6m (March 2012: $1,580.1m).

We have not allowed for the future Operating Expenses of the AICF Trust or the Liable Entities in the liability assessment.

Table E.4. Comparison of central estimate of liabilities

| 31 March 2013 $m |

31 March 2012 $m |

|||||||||||||||

| Gross of insurance recoveries |

Insurance recoveries |

Net

of insurance recoveries |

Net of insurance recoveries |

|||||||||||||

| Total projected cashflows (uninflated) |

1,561.1 | 216.1 | 1,345.0 | 1,313.1 | ||||||||||||

| Future inflation allowance |

1,294.3 | 126.8 | 1,167.5 | 1,211.9 | ||||||||||||

| Total projected cash-flows with inflation |

2,855.5 | 342.9 | 2,512.6 | 2,525.0 | ||||||||||||

| Discounting allowance |

(923.7 | ) | (104.7 | ) | (818.9 | ) | (944.9 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net present value liabilities |

1,931.8 | 238.2 | 1,693.6 | 1,580.1 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

vi |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

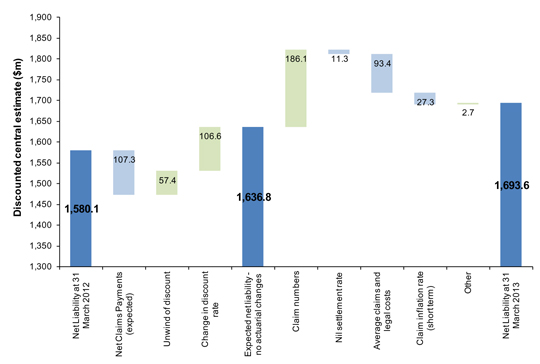

Comparison with previous valuation

In the absence of any change to the claim projection assumptions from our 31 March 2012 valuation, other than allowing for the changes in the discount rate, we would have projected a Discounted Central Estimate liability of $1,636.8m as at 31 March 2013, i.e. an increase of $56.7m from our 31 March 2012 valuation result.

This increase of $56.7m is due to:

| • | A reduction of $49.9m, being the net impact of expected claims payments (which reduce the liability) and the “unwind of discount” (which increases the liability and reflects the fact that cashflows are now one year nearer and therefore are discounted by one year less). |

| • | An increase of $106.6m resulting from the lower discount rates prevailing at 31 March 2013 compared with those adopted at 31 March 2012. |

Our liability assessment at 31 March 2013 of $1,693.6m represents an increase of $56.8m (or 3.5% of the liability), which arises from changes to the claim projection assumptions.

The increase of $56.8m is principally a consequence of:

| • | An increase in the projected future number of claims for most disease types; and |

| • | A decrease in projected future insurance recoveries largely as a result of the commutations entered into during 2012/13. This leads to lower future recoveries being available (i.e. increasing the liability) although this has been done in exchange for an immediate cash amount having been paid to AICF; |

offset by

| • | Lower assumed average claim awards, in particular for mesothelioma; |

| • | Higher assumed future nil settlement rate for most disease types; and |

| • | A reduction in the assumed rate of claim inflation over the near-term in response to the current prevailing economic conditions. The long-term rate of claim inflation has not been changed. |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

vii |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

The following chart shows an analysis of the change in our liability assessments from March 2012 to March 2013.

Figure E.2. Analysis of change in central estimate liability

Note: Green bars signal that this factor has given rise to an increase in the liability whilst light blue bars signal that this factor has given rise to a reduction in the liability.

The undiscounted liability as of 31 March 2013 has increased from $2,418m (based on the 31 March 2012 valuation) to $2,513m. This represents an increase of $95m (approximately 4% of the undiscounted liability).

Amended Final Funding Agreement calculations

The Amended Final Funding Agreement sets out the basis on which payments will be made to the AICF Trust.

Additionally, there are a number of other figures specified within the Amended Final Funding Agreement that we are required to calculate. These are:

| • | Discounted Central Estimate; |

| • | Term Central Estimate; and |

| • | Period Actuarial Estimate. |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

viii |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Table E.5. Amended Final Funding Agreement calculations

| $m | ||||

| Discounted Central Estimate (net of cross-claim recoveries, Insurance and Other Recoveries) |

1,693.6 | |||

| Period Actuarial Estimate (net of cross-claim recoveries, gross of Insurance and Other Recoveries) comprising: |

384.7 | |||

| Discounted value of cashflow in 2013/14 |

127.3 | |||

| Discounted value of cashflow in 2014/15 |

129.0 | |||

| Discounted value of cashflow in 2015/16 |

128.4 | |||

| Term Central Estimate (net of cross-claim recoveries, Insurance and Other Recoveries) |

1,688.3 | |||

The actual funding amount due at a particular date will depend upon a number of factors, including:

| • | the net asset position of the AICF Trust at that time; |

| • | the free cash flow amount of the James Hardie Group in the preceding financial year; and |

| • | the Period Actuarial Estimate in the latest Annual Actuarial Report. |

Uncertainty

Estimates of asbestos-related disease liabilities are subject to considerable uncertainty, significantly more than personal injury liabilities in relation to other causes, such as CTP or Workers Compensation claims.

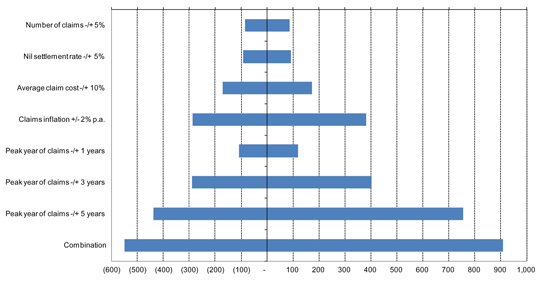

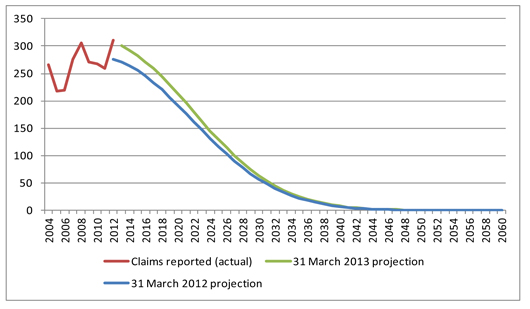

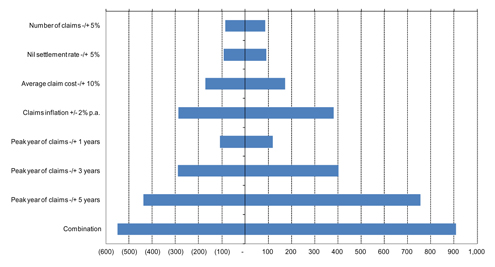

It should therefore be expected that the actual emergence of the liabilities will vary from any estimate. As indicated in Figure E.3, depending on the actual out-turn of experience relative to that currently forecast, the variation could potentially be substantial.

Thus, no assurance can be given that the actual liabilities of the Liable Entities to be met by the AICF Trust will not ultimately exceed the estimates contained in this Report. Any such variation may be significant.

We have performed sensitivity testing to identify the impact of different assumptions upon the size of the liabilities.

We note that these sensitivity test ranges are not intended to correspond to a specified probability of sufficiency, nor are they intended to indicate an upper bound or a lower bound of all possible outcomes.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

ix |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Figure E.3. Sensitivity testing results – Impact around the Discounted Central Estimate (in $m)

The single most sensitive assumption shown in the chart is the peak year of claims reporting against the Liable Entities. Shifting the peak year of claims reporting by 5 years (e.g. for mesothelioma, it would be equivalent to shifting the peak year from 2010/11 to 2015/2016) could imply an increase in the discounted central estimate of approximately 45%.

Table E.6. Summary results of sensitivity analysis

| Undiscounted | Discounted | |||

| Central estimate |

$2,513m | $1,694m | ||

| Range around the central estimate |

-$940m to +$1,700m |

-$550m to +$910m | ||

| Range of liability estimates |

$1.57bn to $4.21bn |

$1.14bn to $2.60bn |

Whilst the table above indicates a range around the discounted central estimate of liabilities of -$550m to +$910m, the actual cost of liabilities could fall outside that range depending on the actual experience.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

x |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

Data, Reliances and Limitations

We have been provided with the following data by AICFL:

| • | Claims dataset at 31 March 2013 with individual claims listings; |

| • | Accounting transactions dataset at 31 March 2013 (which includes individual claims payment details); and |

| • | Detailed insurance bordereaux information (being a listing of claims filed with the insurers of the Liable Entities) produced by Randall & Quilter Investment Holdings as at 31 March 2013. |

While we have tested the consistency of the various data sets provided, we have not otherwise verified the data nor have we undertaken any auditing of the data at source. We have relied on the data provided as being complete and accurate in all material respects. Consequently, should there be material errors or incompleteness in the data, our assessment could be affected materially.

Executive Summary Not Report

Please note that this executive summary is intended as a brief overview of our Report. To properly understand our analysis and the basis of our liability assessment requires examination of our Report in full.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

xi |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| 1 | Scope and Purpose |

| 1.1 | Introduction |

The Amended Final Funding Agreement requires the completion of an Annual Actuarial Report evaluating the potential asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust.

| 1.1.1 | Liable Entities |

The Liable Entities are defined as being the following entities:

| • | Amaca Pty Ltd (formerly James Hardie & Coy); |

| • | Amaba Pty Ltd (formerly Jsekarb, James Hardie Brakes and Better Brakes); and |

| • | ABN60 Pty Ltd (formerly James Hardie Industries Ltd). |

In addition, the liability for Baryulgil claims is deemed to be a liability of Amaca by virtue of the James Hardie (Civil Liability) Act 2005 (NSW). Under Part 4 of that Act, Amaca is liable for “Marlew Asbestos Claims” or “Marlew Contribution Claims” as defined in that Act.

| 1.1.2 | Personal asbestos claims |

Under the Amended Final Funding Agreement, the liabilities to be met by the AICF Trust relate to personal asbestos-related disease liabilities of the Liable Entities.

Such claims must relate to exposure which took place in Australia and which have been brought in a Court in Australia.

The precise scope of the liabilities is documented in Section 1.2 and in Appendix H of this Report.

| 1.1.3 | Purpose of report |

KPMG Actuarial has been retained by AICFL to provide an Annual Actuarial Report as required under the Amended Final Funding Agreement and this is detailed in our Engagement Letter dated 15 November 2012.

The prior written consent of KPMG Actuarial is required for any other use of this Report or the information contained in it.

Our valuation is effective as at 31 March 2013 and has been based on claims data and information as at 31 March 2013 provided to us by AICFL.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

1 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| 1.2 | Scope of report |

We have been requested to provide an actuarial assessment as at 31 March 2013 of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust, consistent with the terms of the Amended Final Funding Agreement.

The assessment is on a central estimate basis and is based on the claims experience as at 31 March 2013.

A “central estimate” liability assessment is an estimate of the expected value of the range of potential future liability outcomes. In other words, if all the possible values of the liabilities are expressed as a statistical distribution, the central estimate is an estimate of the mean of that distribution.

It is of note that our liability assessment:

| • | Relates to the Liable Entities and Marlew (in relation to Marlew Claims arising from asbestos mining activities at Baryulgil). |

| • | Is intended to cover: |

| • | The amount of settlements, judgments or awards for all Personal Asbestos Claims. |

| • | Claims Legal Costs incurred by the AICF Trust in connection with the settlement of Personal Asbestos Claims. |

| • | Is not intended to cover: |

| • | Personal injury or death claims arising from exposure to asbestos which took place outside Australia. |

| • | Personal injury or death claims, arising from exposure to Asbestos, which are brought in Courts outside Australia. |

| • | Claims for economic loss, other than any economic loss forming part of an award for damages for personal injury and/or death. |

| • | Claims for loss of property, including those relating to land remediation. |

| • | The costs of asbestos or asbestos product removal relating to asbestos or asbestos products manufactured or used by or on behalf of the Liable Entities. |

| • | Includes an allowance for: |

| • | Compensation to the NSW Dust Diseases Board or a Workers Compensation Scheme by way of a claim by such parties for contribution or reimbursement from the Liable Entities, but only to the extent that the cost of such claims is within the limits of funding for such claims as outlined within the Amended Final Funding Agreement. |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

2 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| • | Workers Compensation claims, being claims from former employees of the Liable Entities, but only to the extent that such liabilities are not met by a Workers Compensation Scheme or Policy (see section 1.2.1). |

| • | Assumes that the product and public liability insurance policies of the Liable Entities will continue to respond to claims as and when they fall due. We have not made any allowance for the impact of any disputation concerning Insurance Recoveries, nor for any legal costs that may be incurred in resolving such disputes. |

| • | Makes no allowance for: |

| • | potential Insurance Recoveries that could be made on product and public liability insurance policies placed from 1986 onwards which were placed on a “claims made” basis. |

| • | the future Operating Expenses of the Liable Entities or the AICF Trust. Separate allowance for future Operating Expenses should be considered by the management of AICFL. |

| • | the inherent uncertainty of the liability assessment. That is, no additional provision (or risk margin) has been included in excess of a central estimate. |

Readers of this Report may refer to our previous reports which are available at www.ir.jameshardie.com.au and www.aicf.org.au.

| 1.2.1 | Workers Compensation |

Workers Compensation claims are claims made by former employees of the Liable Entities. Such past, current and future reported claims were insured with, amongst others, Allianz Australia Limited, QBE and the various State-based Workers Compensation Schemes.

Under the Amended Final Funding Agreement, the part of a future Workers Compensation claim that is met by a Workers Compensation Scheme or Policy of the Liable Entities is outside of the AICF Trust. The AICF Trust is, however, to provide for any part of a claim not covered by a Workers Compensation Scheme or Policy (e.g. as a result of the existence of limits of indemnity and policy deductibles on those policies of insurance).

On this basis our liability assessment in relation to Workers Compensation claims and which relates to the AICF Trust, includes only the amount borne by the Liable Entities in excess of the anticipated recoveries due from a Workers Compensation Scheme or Policy.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

3 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

In making our assessment we have assumed that the Workers Compensation insurance programme will continue to respond to claims by former employees of the Liable Entities as and when they fall due. To the extent that they were not to respond owing to (say) insurer insolvency, Insurer Guarantee Funds may be available to meet such obligations.

| 1.2.2 | Dust Disease Board and Other Reimbursements |

There exists a right under Section 8E (Reimbursement Provisions) of the Dust Diseases Act 1942 for the NSW Dust Diseases Board (“DDB”) to recover certain costs from common law defendants, excluding the employer of the claimant.

This component of cost is implicitly included within our liability assessment as the claims awards made in recent periods and in recent settlements contain allowance for DDB reimbursement where applicable. Furthermore, currently reported open claims have an allowance within their case estimates for the costs of DDB reimbursement where relevant and applicable.

The Amended Final Funding Agreement indicates that the AICF Trust is intended to meet Personal Asbestos Claims and that claims by the DDB or a Workers Compensation Scheme for reimbursement will only be met up to a certain specified limit (aggregated across the DDB and Workers Compensation Schemes), being:

| • | In the first financial year (2006/07) a limit of $750,000 applied; |

| • | In respect of each financial year thereafter, that limit is indexed annually in line with the Consumer Price Index; |

| • | There is an overall unindexed aggregate cap of $30m. |

The cashflow and liability figures contained within this Report have already removed that component of any reimbursements that will not be met by the AICF Trust owing to the application of these limits and caps.

| 1.2.3 | Baryulgil (“Marlew Claims”) |

“Marlew Asbestos Claims” and “Marlew Contribution Claims” are deemed to be liabilities of Amaca. These claims specifically include:

| • | Claims made against Amaca Pty Ltd or ABN60 resulting from their past ownership of the mine; and, in the case of Amaca, includes claims made in relation to the joint venture (Asbestos Mines Pty Ltd) established with Wunderlich in 1944 to begin mining at Baryulgil. |

| • | Claims made against the subsequent owner of the mine (following its sale by James Hardie Industries to Woodsreef in 1976), being Marlew Mining Pty Ltd (“Marlew”) which is in liquidation, are to be met by the AICF Trust except where such claims are Excluded Marlew Claims, which are recoverable by the Claimant from other sources. |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

4 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

These claims are discussed further in Section 4.11.

| 1.2.4 | Risk Margins |

Australian-licensed insurance companies are required to hold, and many non-insurance companies elect to hold, insurance and self-insurance claims provisions at a level above the central estimate basis to reflect the uncertainty attaching to the liability assessment and to include an allowance in respect of that uncertainty.

A risk margin is an additional amount held, above the central estimate, so as to increase the likelihood of adequacy of the provisions to meet the ultimate cost of settlement of those liabilities.

We note that the Amended Final Funding Agreement envisages the ongoing financing of the AICF Trust is to be based on a “central estimate” approach and that the Annual Actuarial Report should provide a Discounted Central Estimate valuation.

Accordingly, we have made no allowance for any risk margins within this Report.

| 1.2.5 | Discounting |

We have determined a Discounted Central Estimate in this Report by discounting the projected future cashflows to 31 March 2013 using yields on Commonwealth Government Bonds.

Conceptually, the Discounted Central Estimate would normally represent an amount of money which, if fully provided in advance (i.e. as of 31 March 2013) and invested in risk-free assets (such as Commonwealth Government Bonds) of term and currency appropriate to the liabilities, would generate the necessary investment income such that (together with the capital value of those assets) it would be expected to be sufficient to pay for the liabilities as they fall due.

To the extent that the actual investments are:

| • | of different terms; and/or |

| • | in different currencies; and/or |

| • | provide different expected rates of return |

investment profits or losses would emerge.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

5 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

One of the uncertainties in our valuation is the fact that fixed interest Commonwealth Government Bonds do not exist at most of the durations of our cashflow projection.

At 31 March 2013, there were 18 fixed interest Commonwealth Government Bonds on issue, with 3 of them having maturity dates 10 years or more from now, and with the longest-dated maturity being April 2029.

This means we need to take a long-term view on bond yields that is not measured by market-observable rates of return.

At this valuation, we have made some modifications to the approach taken in relation to the estimation of the bond yields between years 10 and 15. This revised approach is described in detail in Section 3.11 of this Report.

We continue to note that the actual funding mechanism under the Amended Final Funding Agreement only provides for up to three years’ worth of projected Claims and Claims Legal Costs expenditure and one year’s worth of Operating Expenses at any one time.

| 1.3 | Areas of potential exposure |

As identified in Section 1.2, there are other potential sources of claims exposure beyond those directly considered within this Report. However, in a number of cases they are unquantifiable even if they have the potential to generate claims. This is especially the case for those sources of future claim where there has been no evidence of claims to date.

| 1.3.1 | General areas of potential exposure |

Areas of potential changes in claims exposure we have not explicitly allowed for in our valuation include, but are not limited to:

| • | Future significant individual landmark and precedent-setting judicial decisions; |

| • | Significant medical advancements; |

| • | Unimpaired claims, i.e. claims for fear, stress, pure nervous shock or psychological illness. In this regard, we note the 2010/11 decisions by the Supreme Court (in relation to two cases: Tamaresis v Amaca and Galea v Amaca) which indicated that the AICF Trust was not required to meet the cost of nervous shock claims brought by individuals who have not been exposed to asbestos; |

| • | A change in the basis of compensation for asymptomatic pleural plaques for which no associated physical impairment is exhibited; |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

6 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| • | A proliferation (compared to past and current levels of activity) of “third-wave” claims, i.e. claims arising as a result of indirect exposure such as home renovation, washing clothes of family members that worked with asbestos, or from workers involved in the removal of asbestos or the demolition of buildings containing asbestos; |

| • | Changes in legislation, especially those relating to tort reform for asbestos sufferers; |

| • | Introduction of new, or elimination of existing, heads of damage; |

| • | Exemplary and aggravated or punitive damages (being damages awarded for personal injuries caused as a result of negligence or reckless conduct); |

| • | Changes in the basis of apportionment of awards for asbestos-related diseases for claimants who have smoked (we note the decisions in Amaca v Ellis [2010] HCA 5 and Evans v Queanbeyan City Council [2010] NSWDDT 7 which we understand are consistent with the previous decision in Judd v Amaca [2002] NSWDDT 25); |

| • | Any changes to GST or other taxes; and |

| • | Future bankruptcies of other asbestos claim defendants (i.e. other liable manufacturers or distributors). |

Nonetheless, implicit allowance is made in respect of some of these items in the allowance for superimposed inflation included in our liability assessment. Furthermore, to the extent that some of these have emerged in past claims experience, they are reflected in our projections.

| 1.3.2 | New Zealand and other overseas exposures |

We have made no allowance for the risk of further development in relation to New Zealand exposures and the rights of claims from New Zealand claimants in Australian courts (as per Frost vs. Amaca Pty Ltd (2005), NSWDDT 36 although this decision was successfully appealed by Amaca in August 2006) nor for the risk of additional exposures from overseas. This is because, as noted in Section 1.2, the AICF Trust is not required to meet the cost of these claims as they are Excluded Claims.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

7 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| 1.3.3 | Third-wave claims |

We have made some implicit allowance for so-called “third-wave” claims. These are defined as claims for personal injury and / or death arising from asbestos exposure during home renovations by individuals or to builders involved in such renovations. Such claims are allowed for within the projections to the extent to which they have arisen to date and to the extent our exposure model factors in these tertiary exposures in its projection.

We have not allowed for a surge in third-wave claims in the future arising from renovations, but conversely we have not allowed for a tempering of those third-wave claims already included within our projection as a result of improved education of individuals as to the risks of such home renovations, or of any local Councils or State Governments passing laws in this regard.

It should be noted that claims for the cost of asbestos or asbestos product removal from homes and properties or any claims for economic loss arising from asbestos or asbestos products being within such homes and properties is not required to be met by the AICF Trust.

| 1.3.4 | Recent court cases of potential significance |

In our previous valuation report at 31 March 2012, we noted the cases of Amaca vs. Booth, King vs. Amaca, Hamilton vs. BHP, and Lowes vs. Amaca in relation to the levels of general damages awards.

In our previous valuation report at 31 March 2012, we noted that the matter of Lowes vs. Amaca was the subject of appeal by Amaca on aspects including foreseeability and causation. That appeal was not pursued by Amaca.

During 2012/13, there have been further matters of note in this regard.

In the matter of Perez vs. State of New South Wales, judgment was delivered in the Dust Diseases Tribunal on 26 February 2013. Curtis J rejected the formal submission by Special Counsel for the plaintiff that he ought to have regard to the award in King vs. Amaca given they were based on similar facts. Curtis J assessed general damages in the sum of $290,000. This is in line with previous awards for general damages in NSW.

We understand that in the matter of Hamilton vs. BHP, the plaintiff has appealed in relation to the amount awarded for general damages. The outcome of this appeal has not yet been determined as of the date of this report.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

8 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| 1.4 | Data reliances and limitations |

KPMG Actuarial has relied upon the accuracy and completeness of the data with which it has been provided. KPMG Actuarial has not verified the accuracy or completeness of the data, although we have undertaken steps to test its consistency with data previously received. However, KPMG Actuarial has placed reliance on the data previously received, and currently provided, as being accurate and complete in all material respects.

| 1.5 | Uncertainty |

It must be understood that estimates of asbestos-related disease liabilities are subject to considerable uncertainty.

This is due to the fact that the ultimate disposition of future claims will be subject to the outcome of events that have not yet occurred. Examples of these events, as noted in Section 1.3, include jury decisions, court interpretations, legislative changes, epidemiological developments, medical advancements, public attitudes, potential additional third-wave exposures and social and economic conditions such as inflation.

Therefore, it should be expected that the actual emergence of the liabilities will vary, perhaps materially, from any estimate. Thus, no assurance can be given that the actual liabilities of the Liable Entities to be met by the AICF Trust will not ultimately exceed the estimates contained herein. Any such variation may be significant.

| 1.6 | Distribution and use |

The purpose of this Report is as stated in Section 1.1.

This Report should not be used for any purpose other than those specified.

This Report will be provided to the Board and management of AICFL. This Report will also be provided to the Board and management of James Hardie, the NSW Government and to Ernst & Young in their capacity as auditors to both James Hardie and AICFL.

We understand that this Report will be filed with the ASX and placed on James Hardie’s website in its entirety.

We understand that this Report will also be placed on AICFL’s website in its entirety.

KPMG Actuarial consents to this Report being made available to the above-mentioned parties and for the Report to be distributed in the manner described above.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

9 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

To the extent permitted by law, neither KPMG Actuarial nor its Executives, directors or employees will be responsible to any third parties for the consequences of any actions they take based upon the opinions expressed with this Report, including any use of or purported reliance upon this Report not contemplated in Section 1.2. Any reliance placed is that party’s sole responsibility.

Where distribution of this Report is permitted by KPMG Actuarial, the Report may only be distributed in its entirety and judgements about the conclusions and comments drawn from this Report should only be made after considering the Report in its entirety and with necessary consultation with KPMG Actuarial.

Readers are also advised to refer to the “Important Note: Basis of Report” section at the front of the Executive Summary of this Report.

| 1.7 | Date labelling convention used in this Report |

In our analyses throughout this Report (unless otherwise stated), the “year” we refer to aligns with the financial year of AICFL and James Hardie and runs from 1 April to 31 March.

A “2008” notified claim would be a claim notified in the period 1 April 2008 to 31 March 2009. This might also be referred to as “2008/09”.

Similarly, a “2012” claim settlement would be a claim settled in the period 1 April 2012 to 31 March 2013. This might also be referred to as “2012/13”.

| 1.8 | Author of the report |

This Report is authored by Neil Donlevy, an Executive of KPMG Actuarial Pty Ltd, a Fellow of the Institute of Actuaries (London) and a Fellow of the Institute of Actuaries of Australia.

This Report is co-authored by Jefferson Gibbs, an Executive of KPMG Actuarial Pty Ltd, a Fellow of the Institute of Actuaries (London) and a Fellow of the Institute of Actuaries of Australia.

In relation to this Report, the primary regulator for both Neil Donlevy and Jefferson Gibbs is the Institute of Actuaries of Australia.

| 1.9 | Professional standards and compliance |

This Report details a valuation of the outstanding claims liabilities of entities which hold liabilities with features similar to general insurance liabilities as self-insured entities, and which have purchased related insurance protection.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

10 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

In preparing this Report, we have complied with the revised version of Professional Standard 300 of the Institute of Actuaries of Australia (“PS300”), “Valuation of General Insurance Claims”. The revised standard is applicable for balance sheet dates occurring on or after 31 March 2013.

However, as we note in Section 1.2, this Report does not include an allowance for the future Operating Expenses of the AICF Trust (which are estimated by AICFL) and nor does it include any allowance for a risk margin to reflect the inherent uncertainty in the liability assessment.

| 1.10 | Control processes and review |

This valuation report and the underlying analyses have been subject to technical review and internal peer review.

The technical review focuses on ensuring that the valuation models and supporting claims experience analyses that are carried out are done correctly and that the calculations are being correctly applied. The technical review also focuses on ensuring that the data that is being used has been reconciled insofar as possible.

Internal peer review involves a review of the approach, the methods, the assumptions selected and the professional judgments applied.

Both the technical review and internal peer review processes are applied to the Report as well as the valuation models.

| 1.11 | Funding position of the AICF Trust |

This Report does not analyse nor provide any opinion on the current, or prospective, funding position of the AICF Trust, nor of its likely funding needs and its potential use of the loan facility provided by the NSW Government.

This is because to do so requires consideration and estimation of the future financial performance of James Hardie.

This Report only provides analysis and opinion on the estimates of the future expenditure to be met by the AICF Trust.

| 1.12 | Basis of preparation of Report |

We have been advised by the management of AICFL to prepare the Report on a “going concern” basis (i.e. we should assume that AICFL will be able to meet the cost of the liabilities of the Liable Entities as they fall due).

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

11 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| 2 | Data |

| 2.1 | Data provided to KPMG Actuarial |

We have been provided with the following data by AICFL:

| • | Claims dataset at 31 March 2013 with individual claims listings; |

| • | Accounting transactions dataset at 31 March 2013 (which includes individual claims payment details); and |

| • | Detailed insurance bordereaux information (being a listing of claims filed with the insurers of the Liable Entities) produced by Randall & Quilter Investment Holdings as at 31 March 2013. |

We have allowed for the benefits of the product and public liability insurance policies of the Liable Entities based on information provided to us by AICFL relating to the insurance programme’s structure, coverage and layers.

We have also considered the claims data listings which formed the basis of our previous valuation assessments.

The data structures for the claims and accounting databases provided to us by AICFL as of 31 March 2013 are detailed in Appendix G.

| 2.2 | Data limitations |

We have tested the consistency of the various data sets provided to us at different valuation dates. Section 2.3 outlines the nature of the testing undertaken.

However, we have not otherwise verified the data and have instead relied on the data provided as being complete and accurate in all material respects.

We have relied upon the robustness of AICFL’s internal administration and systems as to the completeness of the data provided.

Consequently, should there be material errors or incompleteness in the data, our assessment could also be affected materially.

| 2.3 | Data reconciliation and testing |

We have performed a reconciliation of the data provided at 31 March 2013 with the data provided at 31 March 2012.

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

12 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

We have undertaken a number of tests and reconciliations to test the accuracy of the data to the extent possible, noting the limitations outlined above.

| 2.3.1 | Reconciliation with previous valuation’s data |

We have performed a reconciliation of the claims database as at 31 March 2013 with that provided at 31 March 2012. Our findings are:

| • | Claims notifications: There were no late notifications (claims with a report date prior to 31 March 2012 that were not present in the database at 31 March 2012). In addition, no claims changed notification date between the two databases. |

| • | Portfolio Category: Six claims changed category. Of these, 2 claims have been re-labelled as asbestosis, 2 claims have been re-labelled as wharf claims and 2 claims have been re-labelled as Workers Compensation claims. |

| • | Settlement date: Two claims changed their settlement date – in both cases by an immaterial amount. Additionally, there were 24 product and public liability claims that previously did not have a settlement date recorded (as at 31 March 2012) but have since had a settlement date (prior to 31 March 2012) recorded against them. These claims were identified by AICFL, during a claim review conducted by them in 2012/13, to have been settled in previous years and accordingly AICFL has now reflected the status of these claims in their database as settled and they have assigned the original settlement date to their records.1 |

Changing and developing data is not unexpected or to be considered as adverse. Indeed, changing data is common to all claims administration systems. We do not consider the number or extent of the changes noted above to be unreasonable.

| 2.3.2 | Reconciliation of claims settlement amounts between claims and accounting databases |

The accounting database extract contains the following fields:

| • | Damages – which are gross of cross-claim recoveries; |

| • | Costs; |

| 1 | This matter has also been the subject of reporting and disclosure by James Hardie Industries plc in their quarterly financial statements disclosures for each of the three previous quarters of FY13. |

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

13 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013

| • | DDB reimbursements; |

| • | Other costs; |

| • | Payments to Medicare; and |

| • | Defence legal costs. |

The claims database extract contains the following fields:

| • | Damages – which in some cases are net of cross-claim recoveries, and which in others are gross of cross-claim recoveries. We are able to identify which records are gross of cross-claims recoveries and which records are net of cross-claim recoveries. We have then restated all damages data to be gross of cross-claim recoveries; |

| • | Costs; |

| • | DDB reimbursements; |

| • | Other costs (which include payments to Medicare); and |

| • | Defence legal costs. |

We then mapped the financial data between the two databases into standardised groupings as follows:

Table 2.1: Grouping of financial data from claims and accounting databases

| CLAIMS DATABASE |

ACCOUNTING DATABASE | |||

| Award |

Damages (gross of cross-claims) plus DDB reimbursement plus Medicare (from Accounting Database) | Damages plus DDB reimbursements plus Medicare | ||

| Costs / Other |

Costs plus Other less Medicare (from accounting database) | Costs plus Consulting | ||

| Defence legal costs |

Defence legal costs | Defence legal costs | ||

Note: Recovery amounts are available from the accounting database

| © 2013 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International. Liability limited by a scheme approved under Professional Standards Legislation. |

14 |

|

|

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust |

Effective as at 31 March 2013