Q1 FY16

MANAGEMENT PRESENTATION 14 August 2015

Exhibit 99.4 |

| Q1 FY16

MANAGEMENT PRESENTATION 14 August 2015

Exhibit 99.4 |

PAGE DISCLAIMER This Management Presentation contains forward-looking statements. James Hardie Industries plc (the “company”) may from time to time make forward-looking statements in its periodic reports filed with or furnished to the Securities and Exchange Commission, on Forms 20-F and 6-K, in its annual reports to shareholders, in offering circulars, invitation memoranda and prospectuses, in media releases and other written materials and in oral statements made by the company’s officers, directors or employees to analysts, institutional investors, existing and potential lenders, representatives of the media and others. Statements that are not historical facts are forward-looking statements and such forward-looking statements are statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995. Examples of forward-looking statements include: • statements about the company’s future performance; • projections of the company’s results of operations or financial condition; • statements regarding the company’s plans, objectives or goals, including those relating to strategies, initiatives, competition, acquisitions, dispositions and/or its products; • expectations concerning the costs associated with the suspension or closure of operations at any of the company’s plants and future plans

with respect to any such plants; •

expectations concerning the costs associated with the significant capital expenditure projects at any of the company’s plants and future plans with respect to any such projects; • expectations regarding the extension or renewal of the company’s credit facilities including changes to terms, covenants or

ratios; •

expectations concerning dividend payments and share buy-backs;

• statements concerning the company’s corporate and tax domiciles and structures and potential changes to them, including potential tax

charges; •

statements regarding tax liabilities and related audits, reviews and

proceedings; •

expectations about the timing and amount of contributions to Asbestos Injuries

Compensation Fund (AICF), a special purpose fund for the compensation of proven Australian asbestos-related personal injury and death claims; • expectations concerning indemnification obligations; • expectations concerning the adequacy of the company’s warranty provisions and estimates for future warranty-related costs;

• statements regarding the company’s ability to manage legal and regulatory matters (including but not limited to product liability,

environmental, intellectual property and competition law matters) and to

resolve any such pending legal and regulatory matters within current estimates and in anticipation of certain third-party recoveries; and • statements about economic conditions, such as changes in the US economic or housing recovery or changes in the market conditions in the Asia Pacific region, the levels of new home construction and home renovations, unemployment levels, changes in consumer income, changes or stability in housing values, the availability of mortgages and other financing, mortgage and other interest rates, housing affordability and supply, the levels of foreclosures and home resales, currency exchange

rates, and builder and consumer confidence.

2 |

PAGE DISCLAIMER (continued) Words such as “believe,” “anticipate,” “plan,” “expect,” “intend,” “target,” “estimate,” “project,” “predict,” “forecast,” “guideline,” “aim,” “will,” “should,” “likely,” “continue,” “may,” “objective,” “outlook” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Readers are cautioned not to place undue reliance on these forward-looking statements and all such forward-looking statements are qualified in their entirety by reference to the following cautionary statements. Forward-looking statements are based on the company’s current expectations, estimates and assumptions and because forward-looking statements address future results, events and conditions, they, by their very nature, involve inherent risks and uncertainties, many of which are unforeseeable and beyond the company’s control. Such known and unknown risks, uncertainties and other factors may cause actual results, performance or other achievements to differ materially from the anticipated results, performance or achievements expressed, projected or implied by these forward-looking statements. These factors, some of which are discussed under “Risk Factors” in Section 3 of the Form 20-F filed with the Securities and Exchange Commission on 21 May 2015, include, but are not limited to: all matters relating to or arising out of the prior manufacture of products that contained asbestos by current and former company subsidiaries; required contributions to AICF, any shortfall in AICF and the effect of currency exchange rate movements on the amount recorded in the company’s financial statements as an asbestos liability; governmental loan facility to AICF; compliance with and changes in tax laws and treatments; competition and product pricing in the markets in which the company operates; the consequences of product failures or defects; exposure to environmental, asbestos, putative consumer class action or other legal proceedings; general economic and market conditions; the supply and cost of raw materials; possible increases in competition and the potential that competitors could copy the company’s products; reliance on a small number of customers; a customer’s inability to pay; compliance with and changes in environmental and health and safety laws; risks of conducting business internationally; compliance with and changes in laws and regulations; the effect of the transfer of the company’s corporate domicile from the Netherlands to Ireland, including changes in corporate governance and any potential tax benefits related thereto; currency exchange risks; dependence on customer preference and the concentration of the company’s customer base on large format retail customers, distributors and dealers; dependence on residential and commercial construction markets; the effect of adverse changes in climate or weather patterns; possible inability to renew credit facilities on terms favorable to the company, or at all; acquisition or sale of businesses and business segments; changes in the company’s key management personnel; inherent limitations on internal controls; use of accounting estimates; and all other risks identified in the company’s reports filed with Australian, Irish and US securities regulatory agencies and exchanges (as appropriate). The company cautions you that the foregoing list of factors is not exhaustive and that other risks and uncertainties may cause actual results to differ materially from those referenced in the company’s forward-looking statements. Forward-looking statements speak only as of the date they are made and are statements of the company’s current expectations concerning future results, events and conditions. The company assumes no obligation to update any forward-looking statements or information except as required by law. 3 |

PAGE AGENDA • Overview and Operating Review – Louis Gries, CEO • Financial Review – Matt Marsh, CFO • Questions and Answers In this Management Presentation, James Hardie may present financial measures, sales volume terms, financial ratios, and Non-US GAAP financial measures included in the Definitions and other terms section of this document. The company presents financial measures that it believes are customarily used by its Australian investors. Specifically, these financial measures, which are equivalent to or derived from certain US GAAP measures as explained in the definitions, include “EBIT”, “EBIT margin”, “Operating profit before income taxes” and “Net operating profit”. The company may also present other terms for measuring its sales volume (“million square feet” or “mmsf” and “thousand square feet” or “msf”); financial ratios (“Gearing ratio”, “Net interest expense cover”, “Net interest paid cover”, “Net debt payback”, “Net debt (cash)”); and Non-US GAAP financial measures (“Adjusted EBIT”, “Adjusted EBIT margin”, “Adjusted net operating profit”, “Adjusted diluted earnings per share”, “Adjusted operating profit before income taxes”, “Adjusted effective tax rate on earnings”, “Adjusted EBITDA”, and “Adjusted selling, general and administrative expenses”. Unless otherwise stated, results and comparisons are of the first quarter of the current fiscal year versus the first quarter of the prior fiscal year. 4 |

OVERVIEW

AND OPERATING REVIEW Louis Gries, CEO

|

PAGE • Group net sales increased 3% for the quarter compared to pcp 1 • Group adjusted net operating profit increased 27% to US$63.5 million for the quarter, compared to pcp 1 • Higher volumes and average net sales price across our USA and Europe and Asia Pacific Fiber Cement segments • Results are largely driven by lower production costs due to the continued focus on operating performance and lower input costs of our USA and European Fiber Cement segment • Our current quarter USA and Europe Fiber Cement segment EBIT margin is 26.6% compared to 21.2% in the pcp, above our target range of 20% to 25% • Subsequent to period end, approximately 1.7 million shares were repurchased, at an aggregate cost of US$22.5 million, under the previously announced share buyback program • We started up our sheet machine as part of the previously announced Carole Park capacity expansion project in the quarter, and that project remains on track KEY THEMES 6 1 Prior corresponding period |

PAGE GROUP OVERVIEW 7 Q1'16 Q1'15 Change Adjusted EBIT (US$ millions) 89.7 71.2 26% Adjusted EBIT Margin % 20.9% 17.1% 3.8 pts Adjusted Net Operating Profit (US$ millions) 63.5 50.1 27% Net operating cash flow (US$ million) 55.1 42.5 30% Adjusted Diluted EPS (US cents) 14 11 27% Three Months Ended 30 June |

PAGE USA AND EUROPE FIBER CEMENT 1 st QUARTER SUMMARY 8 • Higher volume driven by modest market growth • Higher average net sales price reflects our annual price increase effective 1 March 2015, partially offset by the impact of foreign exchange and mix • Favorable production costs driven primarily by continued performance improvements across our network of plants, as well as lower freight costs and input costs for pulp and utilities 1 st Quarter Results Net Sales Up 5% to US$337.0 million Sales Volume Up 4% to 480.0 mmsf Average Price Up 1% to US$686 per msf EBIT Up 32% to US$89.5 million EBIT Margin Up 540 bps to 26.6% |

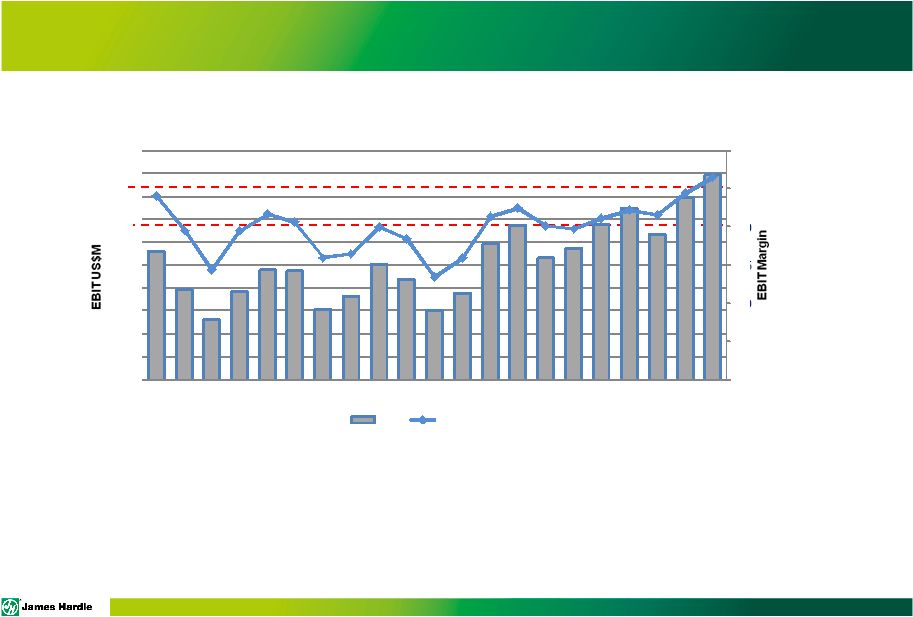

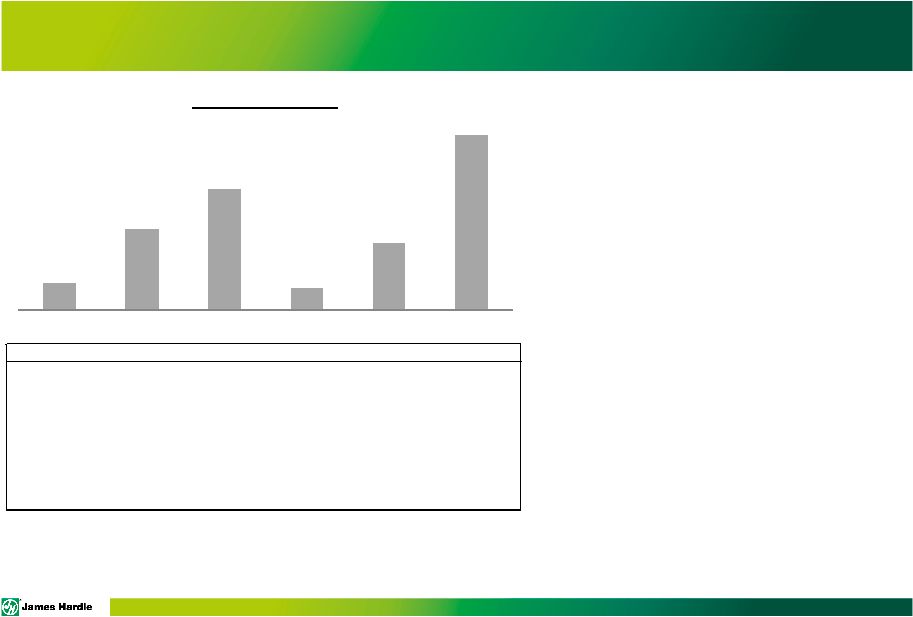

PAGE 1 Excludes asset impairment charges of US$14.3 million in 4 th quarter FY12, US$5.8 million in 3 rd quarter FY13 and US$11.1 million in 4 th quarter FY13 USA AND EUROPE FIBER CEMENT 9 • We expect EBIT margins for fiscal year 2016 to be towards the higher end of, and may exceed our stated target range of 20% to 25%, with a likely return back to our target range in fiscal year 2017 0 5 10 15 20 25 30 0 10 20 30 40 50 60 70 80 90 100 FY11 FY12 FY13 FY14 FY15 FY16 Quarterly EBIT and EBIT Margin 1 EBIT EBIT MARGIN |

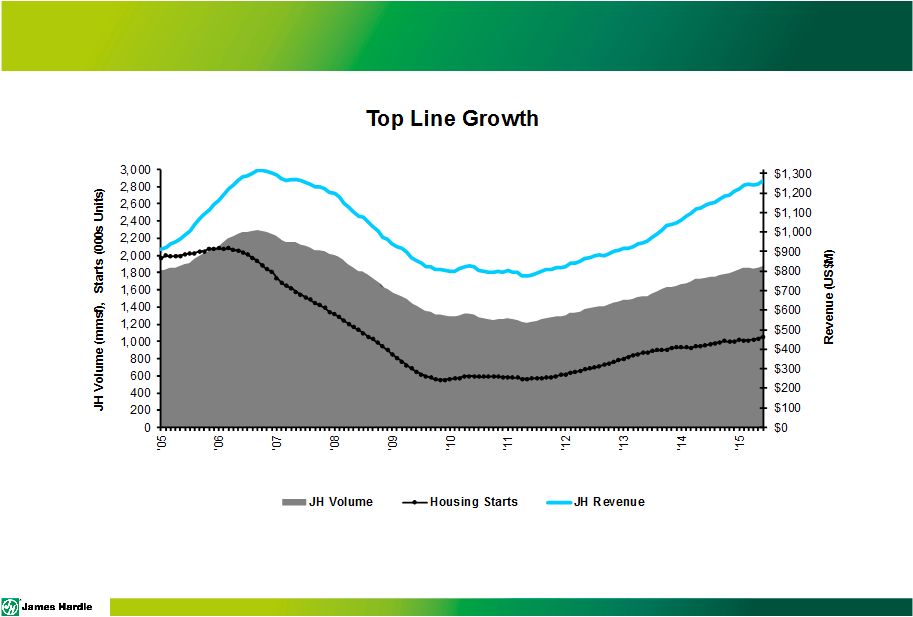

PAGE Rolling 12 month average of seasonally adjusted estimate of housing starts by US Census Bureau

USA FIBER CEMENT 10 |

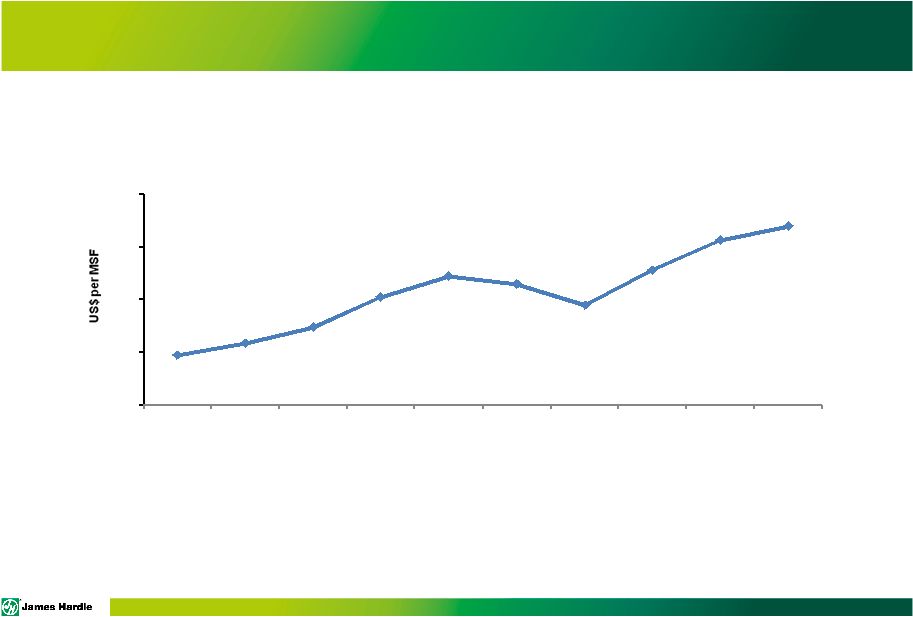

PAGE USA AND EUROPE FIBER CEMENT 11 588 597 609 632 648 642 626 652 675 686 550 590 630 670 710 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 Q1 FY16 Average Net Sales Price |

PAGE 12 • Favorable conditions in addressable markets • Higher volume and sales in AUS, NZ, and Philippines • Higher average net sales price driven by favorable product mix and price increases

• Higher production costs primarily driven by the impact of the depreciating Australian dollar on the US dollar price of

pulp and higher plant performance driven by the start up of our Carole Park sheet

machine •

EBIT results in US Dollars were impacted by a 17% unfavorable change in the weighted

average period AUD/USD exchange rate relative to the prior corresponding

quarter 1 st Quarter Results Net Sales Up 15% to A$117.4 million Sales Volume Up 10% to 119.1 mmsf Average Price Up 5% to A$975 per msf US$ EBIT 1 Down 5% to US$19.7 million A$ EBIT 1 Up 15% to A$25.4 million US$ EBIT Margin 1 Down 10 bps to 21.6% ASIA PACIFIC FIBER CEMENT 1st QUARTER SUMMARY 1 Excludes New Zealand weathertightness claims |

FINANCIAL REVIEW Matt Marsh, CFO |

PAGE GROUP RESULTS • Strong earnings growth reflects: • Higher sales volumes across all

business units •

Higher average sales prices across the USA and Europe and Asia Pacific Fiber Cement segments • Lower input costs for the USA and

Europe Fiber Cement segment driven by pulp and utilities

• Improved plant performance across our USA and Europe Fiber Cement segment • Marginally higher organizational

spend, primarily driven by higher General Corporate expense, consisting of higher stock compensation expenses and higher realized foreign exchange losses caused by

the strengthening of the US dollar during the quarter

• Net operating cash flow of US$55.1 million for the quarter compared to US$42.5 million in the pcp • Capital allocation remains on strategy • On 1 July 2015, we made a payment of A$81.1 million (US$62.8 million) to AICF, representing 35% of our

free cash flow for fiscal year 2015

• Subsequent to period end, approximately 1.7 million shares were repurchased, at an aggregate cost of

US$22.5 million, under the previously announced share buyback program

14 |

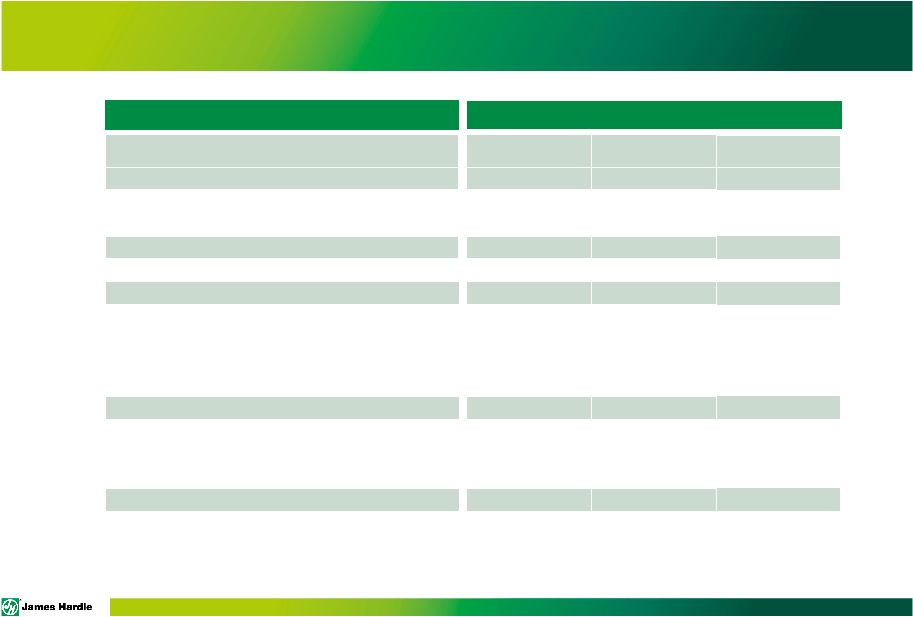

PAGE Net sales increased 3% • Higher sales volumes • Higher average net sales prices in local currencies Gross profit margin increased 320 bps • Continued performance improvement across our US plants • Lower input costs in the USA and Europe Fiber Cement segment • Higher average net sales price SG&A expenses increased • Higher stock compensation expenses due to a 14% appreciation in our stock price • Higher discretionary expenses and realized losses on foreign currency transactions caused by the strengthening of the US dollar • Partially offset by lower SG&A expenses in the business units Non-operating expenses • Interest expense increased related to our debt position • Other income (expense) includes: gain on the sale of the Australian pipes business and favorable unrealized foreign exchange gains and interest rate swaps • Income tax expense increased primarily driven by the increase in operating income RESULTS FOR THE 1 st QUARTER 15 US$ Millions Q1 '16 Q1 '15 % Change Net sales 428.3 416.8 3 Gross profit 157.6 140.2 12 SG&A expenses (61.5) (59.9) (3) Research & development expenses (7.1) (8.4) 15 Asbestos adjustments (4.5) (21.5) 79 EBIT 84.5 50.4 68 Net interest expense (5.9) (1.1) Other income (expense) 2.7 (3.7) Income tax expense (21.3) (16.7) (28) Net operating profit 60.0 28.9 Three Months Ended 30 June |

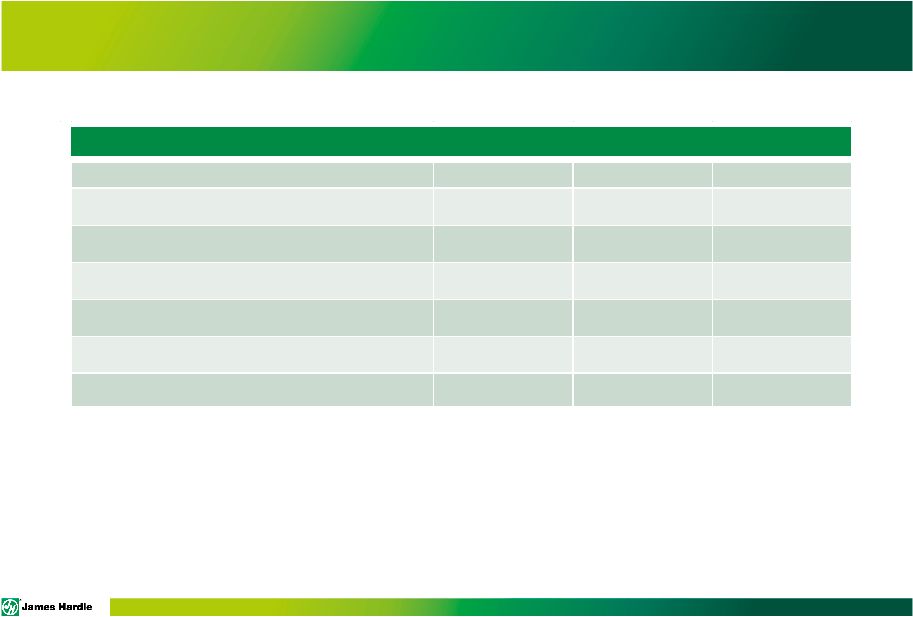

PAGE 1 Includes AICF SG&A expenses and AICF interest income, net RESULTS FOR THE 1 st QUARTER (continued) 16 Asbestos adjustments • 1% change in the AUD / USD exchange rate from beginning to ending balance sheet date for the period compared to a 2% change in spot rates in the prior corresponding period Adjusted net operating profit increased 27% • 26% increase in Adjusted EBIT • A US$6.4 million increase in Adjusted income tax expense • Favorable movement in other income (expense) of US$6.4 million • Gross interest expense of US$5.7 million US$ Millions Q1 '16 Q1 '15 % Change Net operating profit 60.0 28.9 Asbestos: Asbestos adjustments 4.5 21.5 (79) Other asbestos 1 0.4 0.8 (50) New Zealand weathertightness claims 0.2 (1.3) Asbestos and other tax adjustments (1.6) 0.2 Adjusted net operating profit 63.5 50.1 27 Three Months Ended 30 June |

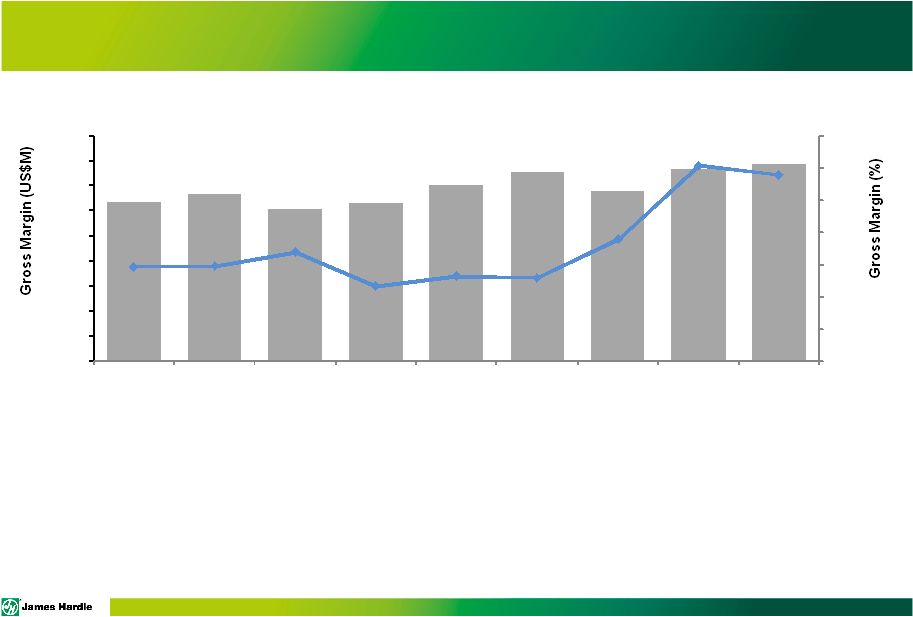

PAGE GROSS PROFIT - GROUP 17 • Gross profit margins remain strong • Price improvements continue as we execute on pricing strategies and reduce pricing inefficiencies • Input costs for pulp and utilities are lower and plant performance remains on a positive trend line as we continue to focus on cost management and operational excellence 126.3 140.2 157.6 33.9 33.6 36.8 31.0 32.0 33.0 34.0 35.0 36.0 37.0 38.0 - 20.0 40.0 60.0 80.0 100.0 120.0 140.0 160.0 180.0 Q1 FY14 Q1 FY15 Q1 FY16 |

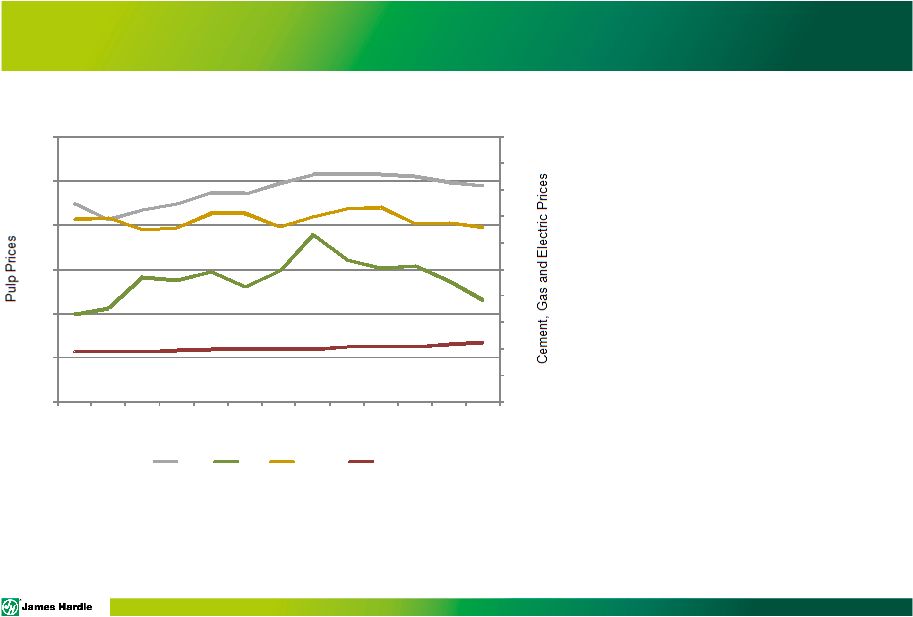

PAGE US INPUT COSTS • The price of NBSK pulp reduced by ~5% compared to pcp 1 , while cement has increased ~8% over pcp 1 • The cost of electricity for industrial users decreased from prior period • The cost of gas continued to trend down quarter over quarter 18 The information underlying the table above is sourced as follows: • Pulp – Cost per ton – from RISI • Gas – Cost per thousand cubic feet for industrial users – from US Energy Information Administration • Electric – Cost per thousand kilowatt hour for industrial users – from US Energy Information Administration • Cement – Relative index from the Bureau of Labor Statistics 1 Prior corresponding period 0 1 2 3 4 5 6 7 8 9 10 0 200 400 600 800 1,000 1,200 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Quarterly US Input Costs PULP GAS ELECTRIC CEMENT |

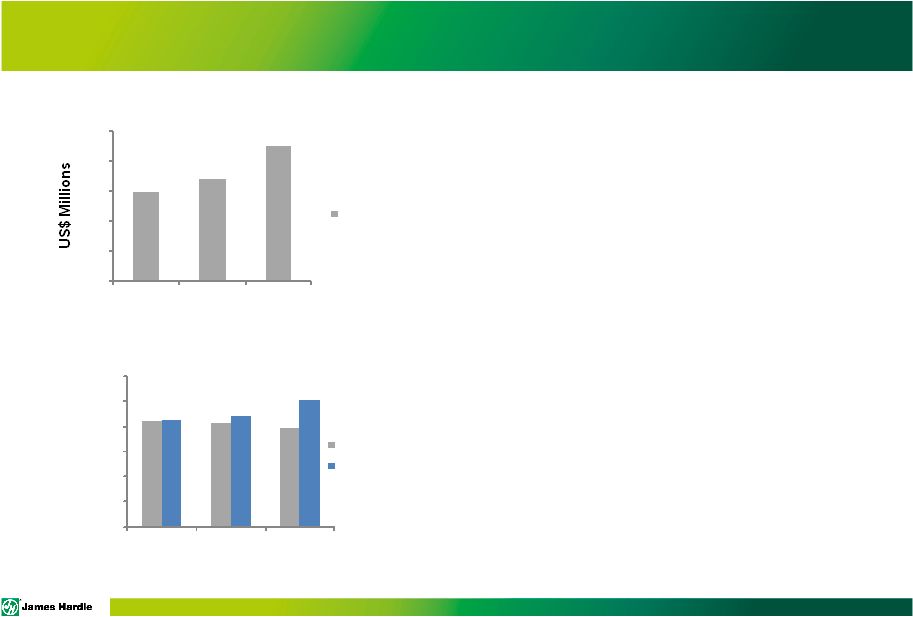

PAGE 1 Excludes New Zealand weathertightness claims USA and Europe Fiber Cement EBIT summary: • EBIT increased by 32% when compared to pcp • The increase for the quarter was driven by improved plant performance, lower input costs, increased volumes and lower segment SG&A expenses Asia Pacific Fiber Cement EBIT summary: • Quarter EBIT 1 decreased 5% compared to pcp. The Asia Pacific Fiber Cement segment results in US dollars were impacted by a 17% unfavorable change in the weighted average period AUD/USD exchange rate relative to the prior corresponding quarter. • EBIT 1 in local currency for the quarter increased 15% compared to pcp SEGMENT EBIT – 1 st QUARTER 19 59.4 68.0 89.5 0 20 40 60 80 100 FY14 FY15 FY16 USA and Europe Fiber Cement Q1 EBIT 21.1 20.7 19.7 21.4 22.1 25.4 0 5 10 15 20 25 30 FY14 FY15 FY16 Asia Pacific Fiber Cement 1 US$ Q1 EBIT A$ Q1 EBIT |

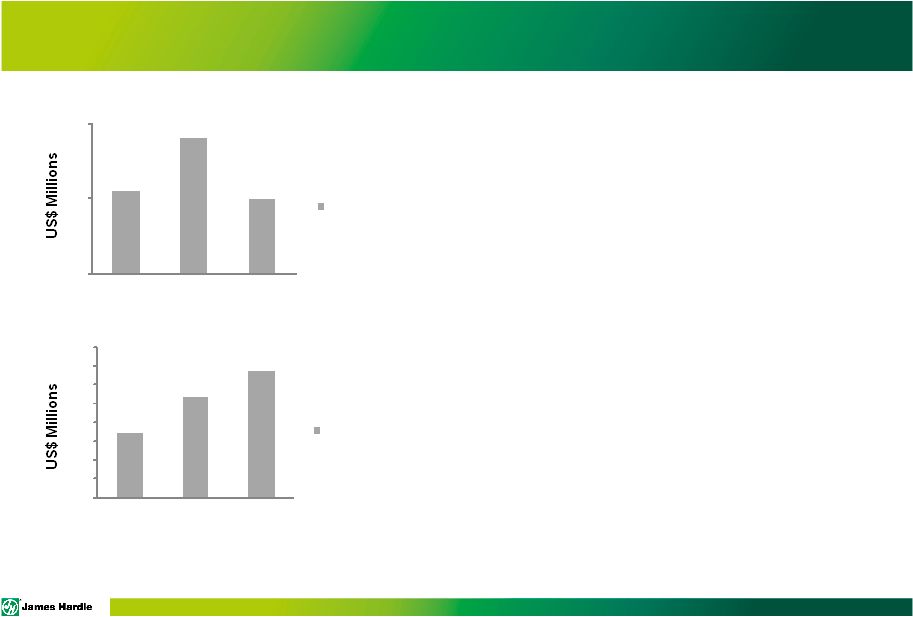

PAGE 1 Excludes Asbestos related expenses and adjustments and ASIC expenses R&D summary: • Continued broadly in line with historic trend line on a percentage of sales basis • Fluctuations reflect normal variation and timing in number of R&D projects in process in any given period General corporate costs: • Results for the quarter increased due to higher : • Stock compensation related to share price appreciation • Discretionary expenses • Foreign exchange losses SEGMENT EBIT – 1 st QUARTER 20 (6.1) (6.8) (6.0) (7) (6) (5) FY14 FY15 FY16 Research and Development Q1 EBIT (6.9) (10.7) (13.5) (16) (14) (12) (10) (8) (6) (4) (2) 0 FY14 FY15 FY16 General Corporate Costs 1 Q1 EBIT |

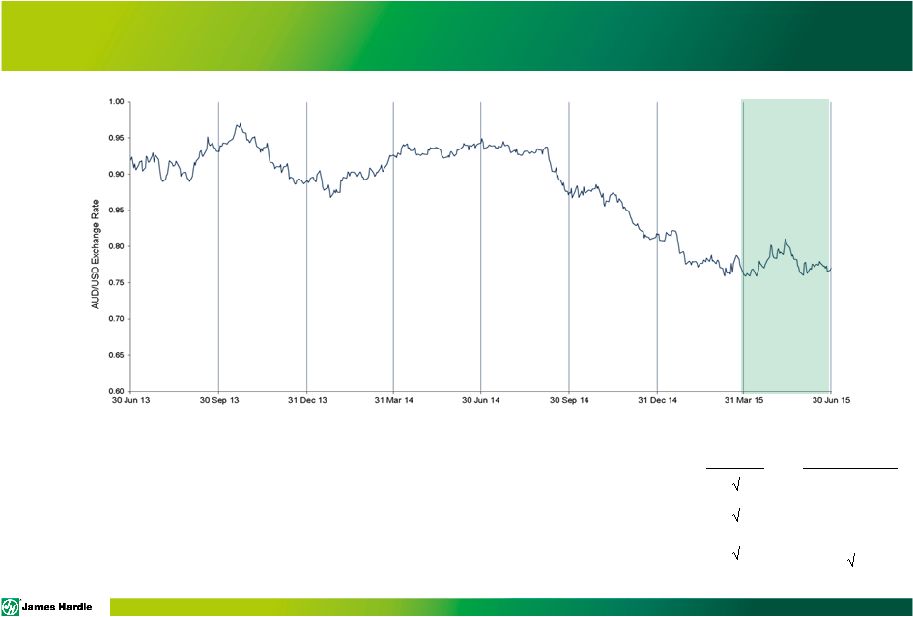

PAGE CHANGES IN AUD vs. USD • Unfavorable impact from translation of Asia Pacific results • Favorable impact on corporate costs incurred in Australian dollars • Unfavorable impact from translation of asbestos liability balance Earnings Balance Sheet N/A N/A 21 |

PAGE 1 Includes Asbestos adjustments, AICF SG&A expenses and AICF interest expense, net

2 Excludes tax effects of Asbestos and other tax adjustments 26.5% estimated adjusted effective tax rate (ETR) for the year • Adjusted income tax expense increased due to the increase in operating profit before income taxes, primarily in the US • The difference between adjusted income tax expense and income tax expense increased primarily due to lower asbestos and other tax adjustments • Income taxes are paid and payable in Ireland, the US, Canada, New Zealand and the Philippines • Income taxes are not currently paid or payable in Europe (excluding Ireland) or Australia due to tax losses. Australian tax losses primarily result from deductions relating to contributions to AICF INCOME TAX 22 Q1’16 Q1’15 Operating profit before taxes 81.3 45.6 Asbestos: Asbestos adjustments 1 4.9 22.3 NZ weathertightness claims 0.2 (1.3) Adjusted net operating profit before taxes 86.4 66.6 Adjusted income tax expense 2 (22.9) (16.5) Adjusted effective tax rate 26.5% 24.8% Income tax expense (21.3) (16.7) Income taxes paid 4.3 2.5 Income taxes payable 15.1 6.5 Three Months Ended 30 June |

PAGE 1 CASHFLOW 23 1 Includes Asbestos Adjustments and changes in asbestos-related assets and liabilities

2 Includes capitalized interest and proceeds from sale of property, plant and equipment

(US$ Millions)

Q1'16 Q1'15 Change (%) Net Income 60.0 28.9 Asbestos related 1 4.6 20.9 (78) Depreciation & amortization 18.2 16.6 10 Working capital 1.4 (0.4) Other non-cash items (29.1) (23.5) (24) Cash Flow from Operations 55.1 42.5 30 Capital expenditures 2 (16.4) (48.6) 66 Acquisition of assets (0.5) - Free Cash Flow 38.2 (6.1) Dividends paid - (124.6) Net payment of long-term debt (15.0) - Share related activities 1.2 (6.6) Free Cash Flow after Financing Activities 24.4 (137.3) • Net income increased US$31.1 million compared to prior corresponding period • Improved working capital driven by: • Improved inventory and A/P turns • Partially offset by an unfavorable change in A/R due to the timing of billing and collections • Lower capital expenditures: • Reflecting near completion of our previously announced US and Australian capacity projects • While continuing to invest in maintenance capital expenditure programs • Lower financing activities: • No dividends being paid in the current period, compared to the US$124.6 million payment of the one-time 125 year anniversary special dividend during the first quarter of fiscal year 2015 |

PAGE FINANCIAL MANAGEMENT SUPPORTING GROWTH 24 Strong margins and operating cash flows Strong governance and transparency Investment-grade financial management Investing in R&D and capacity expansion to support organic growth Maintain ordinary dividends within the defined payout ratio Flexibility for: • Accretive and strategic inorganic opportunities • Withstand market cycles • Consider further shareholder returns when appropriate Financial management consistent with an investment grade credit. Ability to withstand market cycles and other unanticipated events. 1 Strong Financial Management Disciplined Capital Allocation 2 Liquidity and Funding 3 ~$590 million of bank facilities, 68% liquidity as of Q’16 2.2 year weighted average maturity of bank facilities Completed the sale of US$325 million 8 year 5.875% senior unsecured notes Conservative leveraging of balance sheet within 1-2 times adjusted EBITDA target |

PAGE LIQUIDITY PROFILE 25 • Strong balance sheet position: • US$92.3 million of cash • US$382.6 million of gross debt • US$590 million of bank debt facilities • US$325 million 8 year unsecured notes 2,3 • 68% liquidity as of Q1’16 • At 30 June 2015, net debt of US$290.3 million compared to net debt of US$330.5 million at 31 March 2015 • At 30 June 2015, we have US$325.0 million in senior unsecured notes due 15 February 2023 with an interest of rate 5.875%. Interest is payable semi- annually in arrears on 15 August and 15 February each year. • Net Debt within target range of 1-2 times EBITDA excluding asbestos • We remain in compliance with all debt covenants 1 Debt maturities as at Q1’16 were as follows: US$50 million in Q4’16, US$150 million in Q1’17, US$100 million in

Q1’18, US$125 million Q3’18, US$40 million in Q4’19, US$125 million in

Q1’20 and US$325 million in Q4’23 2

Callable from February 2018

3 Original issue discount (OID) US$2.4 million at 30 June 2015 $50 $150 $225 $40 $125 $325 FY'16 FY'17 FY'18 FY'19 FY'20 FY'23 Debt Maturity Profile 1 Liquidity Profile of Bilateral Facilities Three months ended 30 June Cash US$92.3 million Total Combined Bank Facilities US$590.0 million Drawn Bank Facilities US$60.0 million Undrawn Bank Facilities US$530.0 million Weighted Average Interest Rate of drawn Bank Facilities 1.4% Fixed / Floating Interest Ratio 110% fixed Weighted Average Term (Bank Facilities) 2.2 years Weighted Average Term (Total Facilities) 4.1 years |

PAGE ASBESTOS CLAIMS DATA 26 1 Average claim settlement is derived as the total amount paid divided by the number of non-nil claim

settlements 2 This actuarial estimate

is a function of the assumed experience by disease type and the relative mix of settlements assumed by disease type. Any variances in the assumed mix of settlements by disease type will have an impact on the average claim settlement experience

Q1 '16 Q1 '15 % Change Claims received 139 156 11 Actuarial estimate for the period 164 153 (7) Difference in claims received to actuarial estimate 25 (3) Average claim settlement 1 233,000 223,000 (4) Actuarial estimate for the period 2 (A$) 302,000 289,000 (4) Difference in claims paid to actuarial estimate 69,000 66,000 (5) Three Months Ended 30 June Claims Data • Claims received during the quarter were 15% below actuarial estimates and 11% lower than the prior corresponding period • Mesothelioma claims reported in the current quarter are 2% above actuarial estimates and are 5% below the prior corresponding period • Average claim settlement sizes are generally lower across all disease types compared to actuarial expectations for fiscal year 2016 • The average claim settlement is 23% below actuarial estimates and 4% higher than the prior corresponding period (A$) |

PAGE • Group net sales increased 3% for the quarter when compared to the prior corresponding period • Group adjusted net operating profit increased 27% for the quarter when compared to the prior corresponding period • Results driven by higher volumes, average net sales price and the continued focus across our plants on operational management and cost management across the Company • Strong financial management continues and disciplined capital allocation resulting in: • Funding organic growth initiatives • A$81.1 million (US$62.8 million) paid to AICF on 1 July 2015, representing 35% of our free cash flow for fiscal year 2015 • Returning capital to shareholders through dividends and/or share buybacks • Net Debt within target range of 1-2 times EBITDA excluding asbestos SUMMARY 27 |

PAGE • Management notes the range of analysts’ forecasts for net operating profit excluding asbestos for the year

ending 31 March 2016 is between US$244 million and US$286 million • Management expects full year Adjusted net operating profit to be between US$240 million and US$270 million assuming, among other things, housing conditions in the United States continuing to improve in line with our

assumed forecasted new construction starts, input prices and production efficiencies

remaining consistent and an average exchange rate at or near current

levels is applicable for the remainder of the year •

Management cautions that although US housing activity has been improving, market

conditions remain somewhat uncertain and some input costs remain

volatile •

Management is unable to forecast the comparable US GAAP financial measure due to

uncertainty regarding the impact of actuarial estimates on

asbestos-related assets and liabilities in future periods FY2016

GUIDANCE 28 |

QUESTIONS |

APPENDIX |

PAGE FINANCIAL SUMMARY 1 Asia Pacific Fiber Cement EBIT excludes New Zealand weathertightness expense of US$0.2 million in Q1’FY16 and benefit of US$1.3 million in Q1’FY15 2 Excludes Asbestos related expenses and adjustments 31 US$ Millions Q1 '16 Q1 '15 % Change Net Sales USA and Europe Fiber Cement 337.0 $

321.5 $

5 Asia Pacific Fiber Cement 91.3 95.3 (4) Total Net Sales 428.3 $

416.8 $

3 EBIT - US$ Millions USA and Europe Fiber Cement 89.5 $

68.0 $

32 Asia Pacific Fiber Cement 1 19.7 20.7 (5) Research & Development (6.0) (6.8) 12 General Corporate 2 (13.5) (10.7) (26) Adjusted EBIT 89.7 $

71.2 $

26 Net interest expense excluding AICF interest income (6.0) (0.9) Other income (expense) 2.7 (3.7) Adjusted income tax expense (22.9) (16.5) (39) Adjusted net operating profit 63.5 $

50.1 $

27 Three Months Ended 30 June |

PAGE 1 Excludes asbestos adjustments, AICF SG&A expenses, AICF interest income, New Zealand weathertightness claims, tax adjustments

2 Excludes asbestos adjustments, AICF SG&A expenses, New Zealand weathertightness claims

KEY RATIOS 32 3 Months FY16 3 Months FY15 3 Months FY14 EPS (Diluted) 1 (US Cents) 14c 11c 12c EBIT/ Sales (EBIT margin) 2 20.9% 17.1% 18.1% Gearing Ratio 1 20.4% (3.3)% (16.5)% Net Interest Expense Cover 2 15.0x 79.1x 84.4x Net Interest Paid Cover 2 108.5x 89.0x 67.5x Net Debt Payback 1.4yrs - - Three Months Ended 30 June |

PAGE EBITDA – 1 st QUARTER 33 1 Asia Pacific Fiber Cement EBIT excludes New Zealand weathertightness expense of US$0.2 million in Q1’FY16 and benefit of US$1.3 million in Q1’FY15. 2 EBITDA excluding Asbestos Adjustments, New Zealand weathertightness 3 Excludes Asbestos related expenses and adjustments US$ Millions Q1'16 Q1'15 % Change Adjusted EBIT USA and Europe Fiber Cement $ 89.5

$

68.0 32

Asia Pacific Fiber Cement 1 19.7 20.7 (5) Research & Development (6.0) (6.8) 12 General Corporate 3 (13.5) (10.7) (26) Depreciation and Amortization USA and Europe Fiber Cement 16.0 14.4 11 Asia Pacific Fiber Cement 2.2 2.2 - EBITDA 2 - Asbestos adjustments (4.5) (21.5) 79 AICF SG&A expenses (0.5) (0.6) 17 New Zealand weathertightness claims (0.2) 1.3 Total EBITDA $ 102.7 $ 67.0

Three Months Ended 30 June |

PAGE NET INTEREST EXPENSE 34 US$ Millions Q1 FY16 Q1 FY15 Gross interest expense (6.6) (0.9) Capitalized interest 1.1 - Interest income 0.1 0.2 Realized loss on interest rate swaps (0.6) (0.2) Net interest expense excluding AICF interest income (6.0) (0.9) AICF net interest income (expense) 0.1 (0.2) Net interest expense (5.9) (1.1) Three Months Ended 30 June |

PAGE ASBESTOS FUND – PROFORMA (unaudited) 35 A$ millions AICF cash and investments - 31 March 2015 28.9 Insurance recoveries 3.9 Loan Drawdowns 17.7 Interest income, net 0.1 Claims paid (36.8) Operating costs (1.0) Other 0.3 AICF cash and investments - 30 June 2015 13.1 |

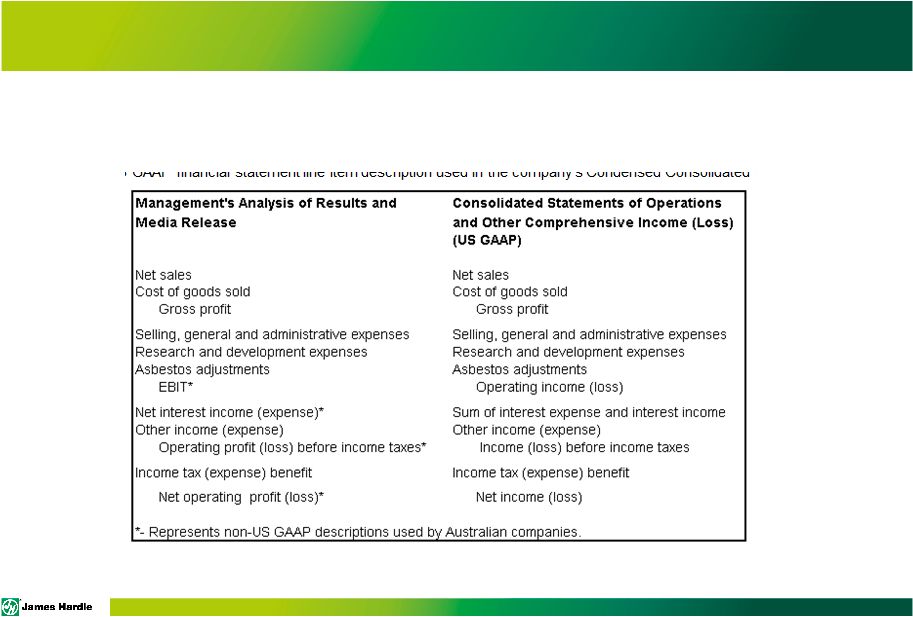

PAGE DEFINITIONS AND OTHER TERMS This Management Presentation forms part of a package of information about the company’s results. It should be read in conjunction with the other parts of this package, including the Management’s Analysis of Results, Media Release and Consolidated Financial Statements Definitions Non-financial Terms AFFA – Amended and Restated Final Funding Agreement AICF – Asbestos Injuries Compensation Fund Ltd NBSK – Northern Bleached Soft Kraft; the company's benchmark grade of pulp Legacy New Zealand weathertightness claims (“New Zealand weathertightness claims”) – Expenses arising from defending and resolving claims in New Zealand that allege poor building design, inadequate certification of plans, inadequate construction review and compliance certification and deficient work by sub-contractors 36 |

PAGE DEFINITIONS AND OTHER TERMS Financial Measures – US GAAP equivalents This document contains financial statement line item descriptions that are considered to be non-US GAAP, but are consistent with those used by Australian companies. Because the company prepares its Consolidated Financial Statements under US GAAP, the following table cross-references each non-US GAAP line item description, as used in Management’s Analysis of Results and Media Release, to the equivalent US GAAP financial statement line item description used in the company’s Condensed Consolidated Financial Statements: 37 |

PAGE DEFINITIONS AND OTHER TERMS EBIT margin – EBIT margin is defined as EBIT as a percentage of net sales Sales Volumes mmsf – million square feet, where a square foot is defined as a standard square foot of 5/16” thickness msf – thousand square feet, where a square foot is defined as a standard square foot of 5/16” thickness Financial Ratios Gearing Ratio – Net debt (cash) divided by net debt (cash) plus shareholders’ equity Net interest expense cover – EBIT divided by net interest expense (excluding loan establishment fees) Net interest paid cover – EBIT divided by cash paid during the period for interest, net of amounts capitalised Net debt payback – Net debt (cash) divided by cash flow from operations Net debt (cash) – Short-term and long-term debt less cash and cash equivalents Return on capital employed – EBIT divided by gross capital employed 38 |

PAGE Adjusted EBIT and Adjusted EBIT margin – Adjusted EBIT and Adjusted EBIT margin are not measures of financial performance under US GAAP and should not be considered to be more meaningful than EBIT and EBIT margin. Management has included these financial measures to provide investors with an alternative method for assessing its operating results in a manner that is focused on the performance of its ongoing operations and provides useful information regarding its financial condition and results of operations. Management uses these non-US GAAP measures for the same purposes.

NON-US GAAP FINANCIAL MEASURES

39 US$ Millions Three Months Ended 30 June Q1 '16 Q1 '15 EBIT 84.5 $

50.4 $ Asbestos: Asbestos adjustments 4.5 21.5 AICF SG&A expenses 0.5 0.6 New Zealand weathertightness claims 0.2 (1.3) Adjusted EBIT 89.7 71.2 Net sales 428.3 $ 416.8 $ Adjusted EBIT margin 20.9% 17.1% |

PAGE Adjusted net operating profit – Adjusted net operating profit is not a measure of financial performance under US GAAP and should not be considered to be more meaningful than net operating profit. Management has included this financial measure to provide investors with an alternative method for assessing its operating results in a manner that is focused on the performance of its ongoing operations. Management uses this non-US GAAP measure for the same purposes. NON-US GAAP FINANCIAL MEASURES 40 US$ Millions Three Months Ended 30 June Q1 '16 Q1 '15 Net operating profit 60.0 $ 28.9 $ Asbestos: Asbestos adjustments 4.5 21.5 AICF SG&A expenses 0.5 0.6 AICF interest (income) expense, net (0.1) 0.2 New Zealand weathertightness claims 0.2 (1.3) Asbestos and other tax adjustments (1.6) 0.2 Adjusted net operating profit 63.5 $ 50.1 $ |

PAGE Adjusted diluted earnings per share – Adjusted diluted earnings per share is not a measure of financial performance under US GAAP and should not be considered to be more meaningful than diluted earnings per share. Management has included this financial measure to provide investors with an alternative method for assessing its operating results in a manner that is focused on the performance of its ongoing operations. Management uses this non-US GAAP measure for the same purposes. 41 NON-US GAAP FINANCIAL MEASURES Three Months Ended 30 June Q1 '16 Q1 '15 Adjusted net operating profit (US$ millions) 63.5 $

50.1 $

Weighted average common shares outstanding -

Diluted (millions)

447.4 446.0 Adjusted diluted earnings per share (US cents) 14 11 |

PAGE Adjusted income tax expense and Adjusted effective tax rate – Adjusted income tax expenses and Adjusted effective tax rate on earnings is not a measure of financial performance under US GAAP and should not be considered to be more meaningful than income tax expense and effective tax rate, respectively. Management has included this financial measure to provide investors with an alternative method for assessing its operating results in a manner that is focused on the performance of its ongoing operations. Management uses this non-US GAAP measure for the same purposes. 42 NON-US GAAP FINANCIAL MEASURES US$ Millions Q1 '16 Q1 '15 Operating profit before income taxes 81.3 $

45.6 $

Asbestos: Asbestos adjustments 4.5 21.5 AICF SG&A expenses 0.5 0.6 AICF interest (income) expense, net (0.1) 0.2 New Zealand weathertightness claims 0.2 (1.3) Adjusted operating profit before income taxes 86.4 $

66.6 $

Income tax expense (21.3) $

(16.7) $

Asbestos and other tax adjustments

(1.6) 0.2 Adjusted income tax expense (22.9) $ (16.5) $ Effective tax rate 26.2% 36.6% Adjusted effective tax rate 26.5% 24.8% Three Months Ended 30 June |

PAGE Adjusted EBITDA – is not a measure of financial performance under US GAAP and should not be considered an alternative to, or more meaningful than, income from operations, net income or cash flows as defined by US GAAP or as a measure of profitability or liquidity. Not all companies calculate Adjusted EBITDA in the same manner as James Hardie has and, accordingly, Adjusted EBITDA may not be comparable with other companies. Management has included information concerning Adjusted EBITDA because it believes that this data is commonly used by investors to evaluate the ability of a company’s earnings from its core business operations to satisfy its debt, capital expenditure and working capital requirements NON-US GAAP FINANCIAL MEASURES 43 US$ Millions Q1 '16 Q1 '15 EBIT 84.5 $ 50.4 $ Depreciation and amortization 18.2 16.6 Adjusted EBITDA 102.7 $ 67.0 $ Three Months Ended 30 June |

PAGE Adjusted selling, general and administrative expenses – Adjusted selling, general and administrative expenses is not a measure of financial performance under US GAAP and should not be considered to be more meaningful than selling, general and administrative expenses. Management has included these financial measures to provide investors with an alternative method for assessing its operating results in a manner that is focused on the performance of its ongoing operations and provides useful information regarding its financial condition and results of operations. Management uses these non-US GAAP measures for the same purposes. NON-US GAAP FINANCIAL MEASURES 44 US$ Millions Q1 '16 Q1 '15 Selling, general and administrative expenses 61.5 $

59.9 $ Excluding: New Zealand weathertightness claims (0.2) 1.3 AICF SG&A expenses

(0.5) (0.6) Adjusted selling, general and administrative expenses

60.8 $

60.6 $ Net sales 428.3 $ 416.8 $ Selling, general and administrative expenses as a percentage of net sales 14.4% 14.4% Adjusted selling, general and administrative expenses as a percentage of net sales 14.2% 14.5% Three Months Ended 30 June |

Q1 FY16

MANAGEMENT PRESENTATION 14 August 2015

|