Exhibit 99.1

| Exhibit 99.1

|

Exhibit 99.1

INVESTOR PRESENTATION

JANUARY 2016

|

|

DISCLAIMER

This Management Presentation contains forward-looking statements. James Hardie Industries plc (the “company”) may from time to time make forward-looking statements in its periodic reports filed with or furnished to the Securities and Exchange Commission, on Forms 20-F and 6-K, in its annual reports to shareholders, in offering circulars, invitation memoranda and prospectuses, in media releases and other written materials and in oral statements made by the company’s officers, directors or employees to analysts, institutional investors, existing and potential lenders, representatives of the media and others. Statements that are not historical facts are forward-looking statements and such forward-looking statements are statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995.

Examples of forward-looking statements include:

statements about the company’s future performance;

projections of the company’s results of operations or financial condition;

statements regarding the company’s plans, objectives or goals, including those relating to strategies, initiatives, competition, acquisitions, dispositions and/or its products;

expectations concerning the costs associated with the suspension or closure of operations at any of the company’s plants and future plans with respect to any such plants;

expectations concerning the costs associated with the significant capital expenditure projects at any of the company’s plants and future plans with respect to any such projects;

expectations regarding the extension or renewal of the company’s credit facilities including changes to terms, covenants or ratios;

expectations concerning dividend payments and share buy-backs;

statements concerning the company’s corporate and tax domiciles and structures and potential changes to them, including potential tax charges;

statements regarding tax liabilities and related audits, reviews and proceedings;

expectations about the timing and amount of contributions to Asbestos Injuries Compensation Fund (AICF), a special purpose fund for the compensation of proven Australian

asbestos-related personal injury and death claims;

expectations concerning indemnification obligations;

expectations concerning the adequacy of the company’s warranty provisions and estimates for future warranty-related costs;

statements regarding the company’s ability to manage legal and regulatory matters (including but not limited to product liability, environmental, intellectual property and

competition law matters) and to resolve any such pending legal and regulatory matters within current estimates and in anticipation of certain third-party recoveries; and

statements about economic conditions, such as changes in the US economic or housing recovery or changes in the market conditions in the Asia Pacific region, the levels of

new home construction and home renovations, unemployment levels, changes in consumer income, changes or stability in housing values, the availability of mortgages and

other financing, mortgage and other interest rates, housing affordability and supply, the levels of foreclosures and home resales, currency exchange rates, and builder and

consumer confidence.

PAGE 2

|

|

DISCLAIMER (continued)

Words such as “believe,” “anticipate,” “plan,” “expect,” “intend,” “target,” “estimate,” “project,” “predict,” “forecast,” “guideline,” “aim,” “will,” “should,” “likely,” “continue,” “may,” “objective,” “outlook” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Readers are cautioned not to place undue reliance on these forward-looking statements and all such forward-looking statements are qualified in their entirety by reference to the following cautionary statements.

Forward-looking statements are based on the company’s current expectations, estimates and assumptions and because forward-looking statements address future results, events and conditions, they, by their very nature, involve inherent risks and uncertainties, many of which are unforeseeable and beyond the company’s control. Such known and unknown risks, uncertainties and other factors may cause actual results, performance or other achievements to differ materially from the anticipated results, performance or achievements expressed, projected or implied by these forward-looking statements. These factors, some of which are discussed under “Risk Factors” in Section 3 of the Form 20-F filed with the Securities and Exchange Commission on 21 May 2015, include, but are not limited to: all matters relating to or arising out of the prior manufacture of products that contained asbestos by current and former company subsidiaries; required contributions to AICF, any shortfall in AICF and the effect of currency exchange rate movements on the amount recorded in the company’s financial statements as an asbestos liability; governmental loan facility to AICF; compliance with and changes in tax laws and treatments; competition and product pricing in the markets in which the company operates; the consequences of product failures or defects; exposure to environmental, asbestos, putative consumer class action or other legal proceedings; general economic and market conditions; the supply and cost of raw materials; possible increases in competition and the potential that competitors could copy the company’s products; reliance on a small number of customers; a customer’s inability to pay; compliance with and changes in environmental and health and safety laws; risks of conducting business internationally; compliance with and changes in laws and regulations; the effect of the transfer of the company’s corporate domicile from the Netherlands to Ireland, including changes in corporate governance and any potential tax benefits related thereto; currency exchange risks; dependence on customer preference and the concentration of the company’s customer base on large format retail customers, distributors and dealers; dependence on residential and commercial construction markets; the effect of adverse changes in climate or weather patterns; possible inability to renew credit facilities on terms favorable to the company, or at all; acquisition or sale of businesses and business segments; changes in the company’s key management personnel; inherent limitations on internal controls; use of accounting estimates; and all other risks identified in the company’s reports filed with Australian, Irish and US securities regulatory agencies and exchanges (as appropriate). The company cautions you that the foregoing list of factors is not exhaustive and that other risks and uncertainties may cause actual results to differ materially from those referenced in the company’s forward-looking statements. Forward-looking statements speak only as of the date they are made and are statements of the company’s current expectations concerning future results, events and conditions. The company assumes no obligation to update any forward-looking statements or information except as required by law.

PAGE 3

|

|

AGENDA

Global Strategy and Business Overview

USA & Europe Fiber Cement

Asia Pacific Fiber Cement

Capital Management Framework

Guidance

Appendix

In this Investor Presentation, the company may present financial measures, sales volume terms, financial ratios, and Non-US GAAP financial measures included in the Definitions and other terms section of this document. The company presents financial measures that it believes are customarily used by its Australian investors. Specifically, these financial measures, which are equivalent to or derived from certain US GAAP measures as explained in the definitions, include “EBIT”, “EBIT margin”, “Operating profit before income taxes” and “Net operating profit”. The company may also present other terms for measuring its sales volume (“million square feet” or “mmsf” and “thousand square feet” or “msf”); financial ratios (“Gearing ratio”, “Net interest expense cover”, “Net interest paid cover”, “Net debt payback”, “Net debt (cash)”); and Non-US GAAP financial measures (“Adjusted EBIT”, “Adjusted EBIT margin”, “Adjusted net operating profit”, “Adjusted diluted earnings per share”, “Adjusted operating profit before income taxes”, “Adjusted effective tax rate on earnings”, “Adjusted EBITDA”, and “Adjusted selling, general and administrative expenses”. Unless otherwise stated, results and comparisons are of the second quarter of the current fiscal year versus the second quarter of the prior fiscal year

PAGE 4

|

|

GLOBAL STRATEGY

Industry Leadership and Profitable Growth

Introduce differentiated products to deliver a sustainable competitive advantage

Aggressively grow demand for our products in targeted market segments

PAGE 5

|

|

A GROWTH FOCUSED COMPANY

Annual net sales US$1.8b

Total assets US$1.9b

Strong cash generation

Operations in North America, Asia Pacific and Europe

3,178 employees

Market cap US$5.08b (approx)

S&P/ASX 100 company

NYSE ADR listing

Market capitalization as at 11 December 2015. Total assets as at 30 September 2015 and employees as at 31 March 2015. Annual net sales for six months to

30 September 2015 annualised. Total assets exclude asbestos compensation.

PAGE 6

|

|

GROUP OVERVIEW – 2nd QUARTER & HALF YEAR FY16 RESULTS

Adjusted Net Operating Profit

2nd Qtr Half Year

US$65.3M Flat US$128.8M 12%

Adjusted EBIT

2nd Qtr Half Year

US$95.3M 12% US$185.0M 18%

Adjusted EBIT Margin %

2nd Qtr Half Year

21.2% 1.9 pts 21.1% 2.9 pts

Adjusted Diluted EPS

2nd Qtr Half Year

US15cents Flat US29cents 12%

Net Operating Cash Flow

Half Year

US$85.5M 151%

Dividends declared per share. Excludes Australian Pipes business which was sold in Q1 FY16

PAGE 7

|

|

KEY THEMES – 2ND QUARTER & HALF YEAR FY16 RESULTS

Higher volumes in all businesses, but PDG in our US business tracked below our target level

Higher average net sales prices in local currencies

Improved plant performance trend sustained

Half year USA and Europe Fiber Cement segment EBIT margin of 25.6% above our target range of 20% to

25%

PAGE 8

|

|

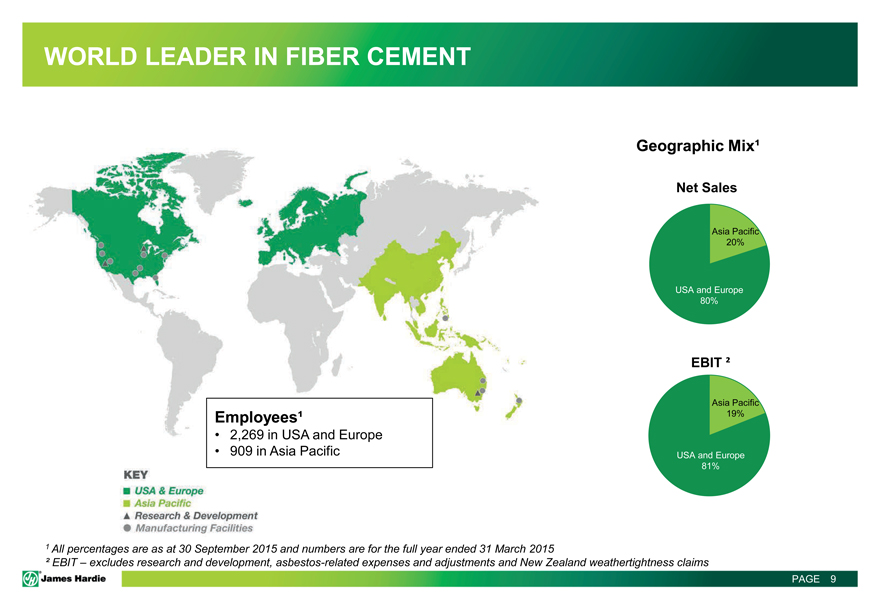

WORLD LEADER IN FIBER CEMENT

Employees¹

2,269 in USA and Europe

909 in Asia Pacific

USA & Europe

Asia Pacific

Research & Development

Manufacturing FacilitiesGeographic Mix¹

Net Sales

Asia Pacific 20%

USA and Europe 80%

EBIT ²

Asia Pacific 19%

USA and Europe 81%

1 All percentages are as at 30 September 2015 and numbers are for the full year ended 31 March 2015

² EBIT – excludes research and development, asbestos-related expenses and adjustments and New Zealand weathertightness claims

KEY

PAGE 9

|

|

CREATING A SUSTAINABLE AND DIFFERENTIATED ADVANTAGE

Research & Development: Significant and consistent investment

US$31.7m spent on Research & Development in FY15 US$394.8m spent on Research & Development since 2000

James Hardie

Siding Products

History of Fiber Cement Substrate Development

7th ENGNEERED FOR CLIMATETM – HardieZoneTM

6th MODIFIED THICKNESS TECHNOLOGY

5TH COLORPLUS TECHNOLOGY

4TH SURFACE ADHESION TECHNOLOGY

3RD SUBSTRATE COMPOSITION

2ND PRIMER ADDED

1ST FIBER-CEMENT SUBSTRATE THE JAMES HARDIE INNOVATION PATH Product Generations generic Fiber-CementPAGE 10

|

|

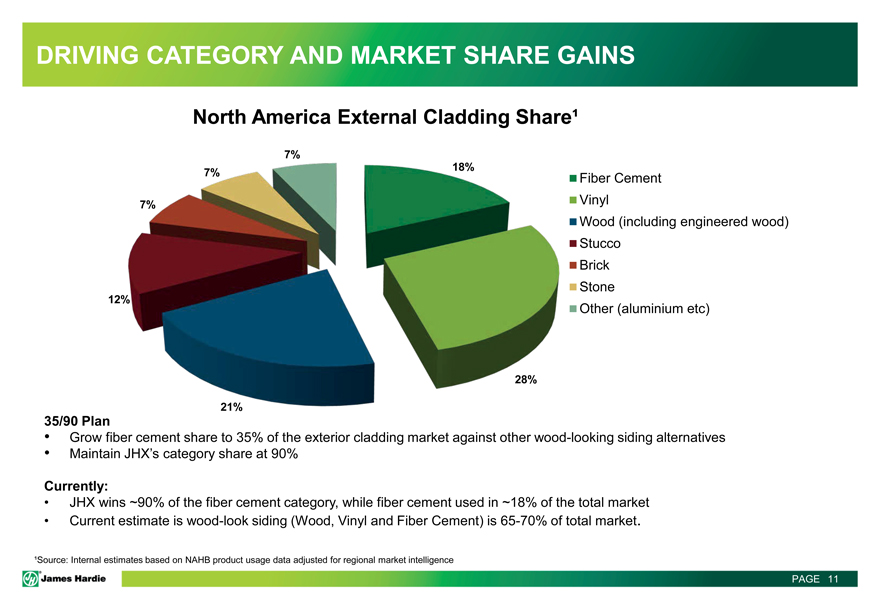

DRIVING CATEGORY AND MARKET SHARE GAINS

North America External Cladding Share¹

7%

7% 18% 7%

12%

28%

21%

Fiber Cement Vinyl

Wood (including engineered wood) Stucco Brick Stone Other (aluminium etc)

35/90 Plan

Grow fiber cement share to 35% of the exterior cladding market against other wood-looking siding alternatives Maintain JHX’s category share at 90%

Currently:

JHX wins ~90% of the fiber cement category, while fiber cement used in ~18% of the total market Current estimate is wood-look siding (Wood, Vinyl and Fiber Cement) is 65-70% of total market.

¹Source: Internal estimates based on NAHB product usage data adjusted for regional market intelligence

PAGE 11

|

|

DELIVERING SUPERIOR PRODUCT PERFORMANCE

Fiber cement is more durable than wood and engineered wood, looks and performs better than vinyl, and is more cost effective and quicker to build with than brick

Fiber Cement Vinyl Engineered Wood

Fire resistant

Hail resistant

Resists warping

Resists buckling

Lasting color

Dimensional stability

Can be repainted

PAGE 12

|

|

BUILDING A PORTFOLIO OF PRODUCTS AND BRANDS

Primary Products

Trim / Commercial Interior Walls / Soffit Backerboard Siding Flooring Fascia Exteriors Ceilings

U.S. & Europe

Asia Pacific

Brand Portfolio

PAGE 13

|

|

USA AND EUROPE FIBER CEMENT SEGMENT

USA Plant Locations

Tacoma, WA

Reno, NV Peru, IL

Pulaski, VA Fontana, CA Summerville, Waxahachie, SC

TX Cleburne, TX

Plant City, FL

Largest fiber cement producer in North America

2,269 employees

9 manufacturing plants¹

2 research and development facilities

HY FY16 HY FY15

Net Sales US$698.9m US$656.9m

EBIT US$178.9m US$142.8m

EBIT Margin 25.6% 21.7%

(US$)

¹ Production was suspended at the Summerville plant in November 2008

PAGE 14

|

|

AGGRESSIVELY GROWING DEMAND FOR OUR PRODUCTS

USA Fiber Cement

Top Line Growth1

3,000 2,800 2,600 2,400 2,200 2,000 1,800 1,600 1,400 1,200 1,000 800 600 400 200 0

$ 1,300

$ 1,200

$ 1,100

$ 1,000

$ 900

$ 800

$ 700

$ 600

$ 500

$ 400

$ 300

$ 200

$ 100

$ 0

’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’15 Revenue (US$M) JH Volume (mmsf), Starts (000s Units) 1Rolling 12 month average of seasonally adjusted estimate of housing starts by US Census Bureau

JH Volume Housing Starts JH Revenue

PAGE 15

|

|

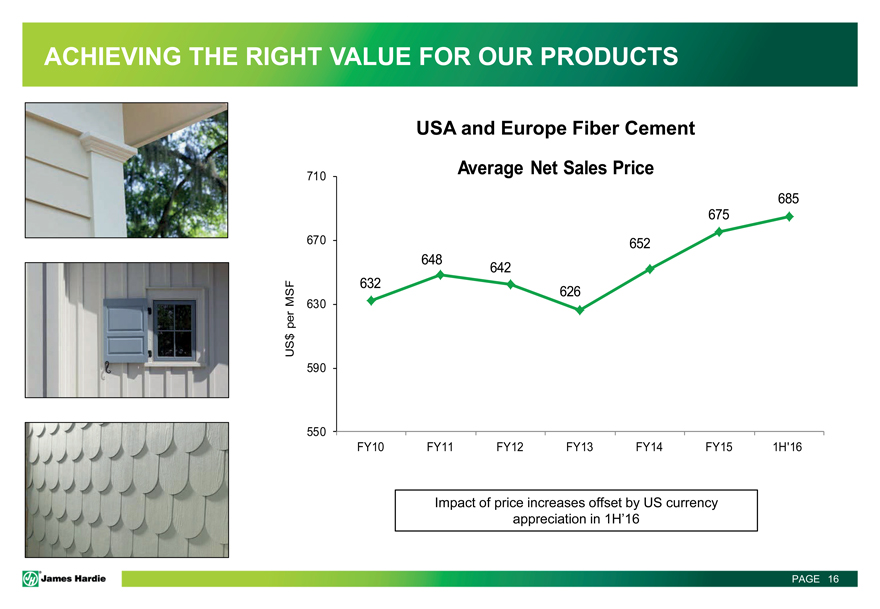

ACHIEVING THE RIGHT VALUE FOR OUR PRODUCTS

USA and Europe Fiber Cement

710 Average Net Sales Price

685 675

670 652 648 642 632 626

630

590

550

FY10 FY11 FY12 FY13 FY14 FY15 1H’16

Impact of price increases offset by US currency appreciation in 1H’16

PAGE 16

US$ per MSF

|

|

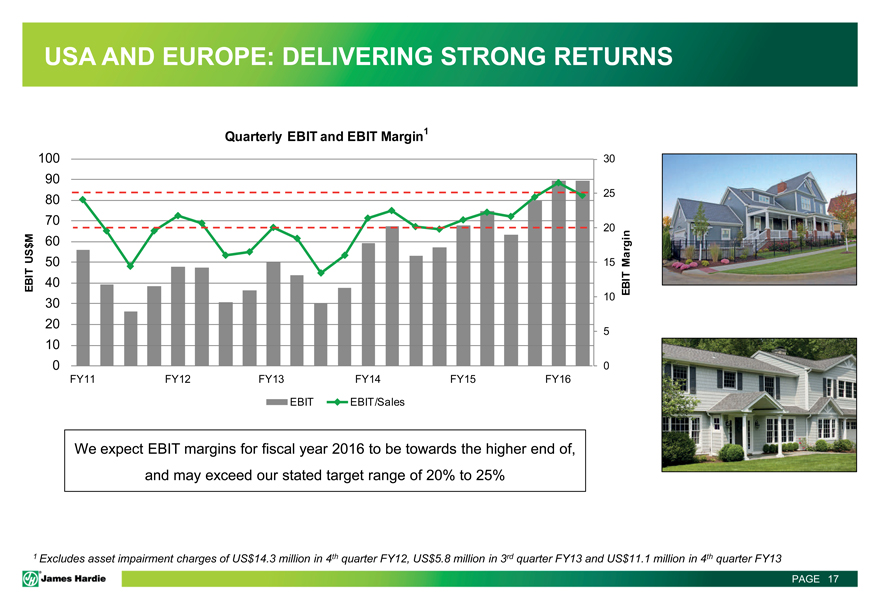

USA AND EUROPE: DELIVERING STRONG RETURNS

Quarterly EBIT and EBIT Margin1

30 25 20 15 10 5 0

EBIT Margin

100 90 80 70 60 50 40 30 20 10 0

EBIT US$M

FY11 FY12 FY13 FY14 FY15 FY16 EBIT EBIT/Sales

We expect EBIT margins for fiscal year 2016 to be towards the higher end of, and may exceed our stated target range of 20% to 25%

1 Excludes asset impairment charges of US$14.3 million in 4th quarter FY12, US$5.8 million in 3rd quarter FY13 and US$11.1 million in 4th quarter FY13

PAGE 17

|

|

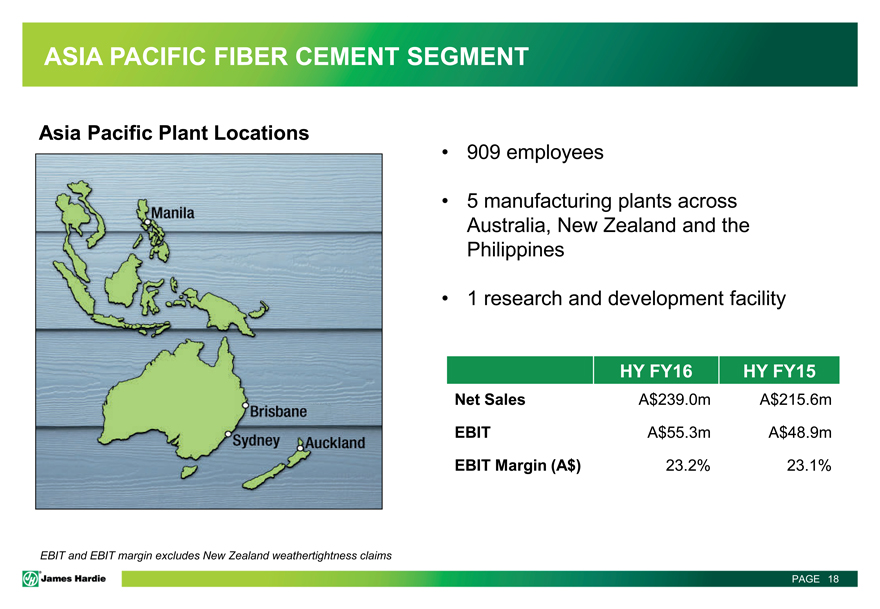

ASIA PACIFIC FIBER CEMENT SEGMENT

Asia Pacific Plant Locations

909 employees

5 manufacturing plants across Australia, New Zealand and the Philippines

1 research and development facility

HY FY16 HY FY15

Net Sales A$239.0m A$215.6m

EBIT A$55.3m A$48.9m

EBIT Margin (A$) 23.2% 23.1%

Manila Brisbane Sydney AucklandEBIT and EBIT margin excludes New Zealand weathertightness claims

PAGE 18

|

|

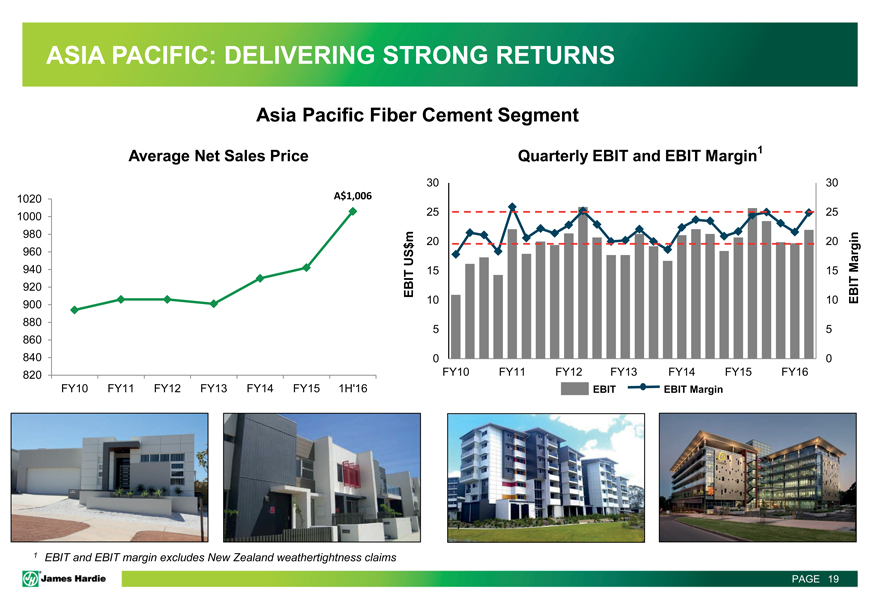

ASIA PACIFIC: DELIVERING STRONG RETURNS

Asia Pacific Fiber Cement Segment

Average Net Sales Price Quarterly EBIT and EBIT Margin1

1020 1000 980 960 940 920 900 880 860 840 820

A$1,006

FY10 FY11 FY12 FY13 FY14 FY15 1H’16

EBIT US$m

30 25 20 15 10 5 0

FY10 FY11 FY12 FY13 FY14 FY15 FY16

EBIT EBIT Margin

EBIT Margin

30 25 20 15 10 5 0

1 EBIT and EBIT margin excludes New Zealand weathertightness claims

PAGE 19

|

|

TARGETING THE RIGHT PRODUCT INTO THE RIGHT MARKET

Asia Pacific Core Markets

Ceilings and partitions Philippines Interior walls New Zealand

Exterior cladding

Australia

General purpose flooring

Australia

PAGE 20

|

|

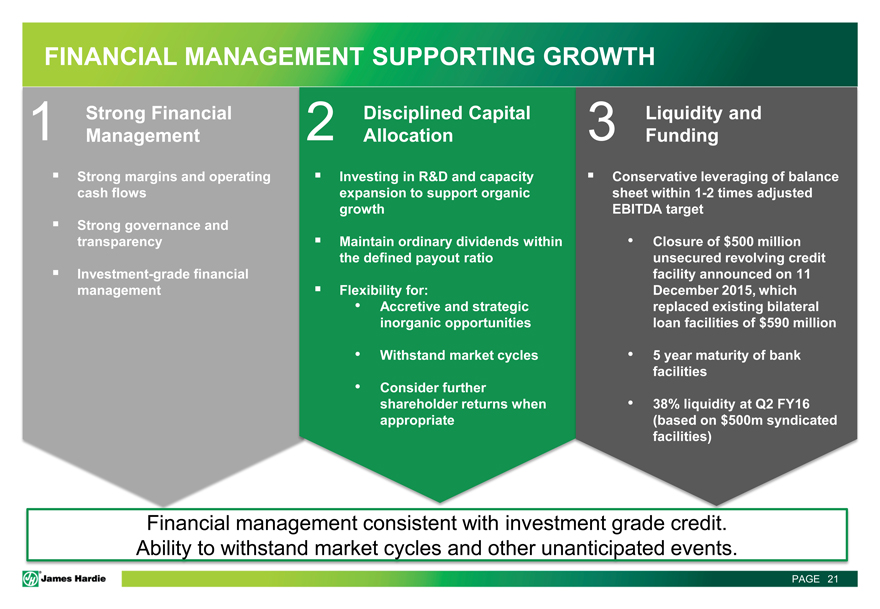

FINANCIAL MANAGEMENT SUPPORTING GROWTH

1

Strong Financial

Management

Strong margins and operating

cash flows

Strong governance and

transparency

Investment-grade financial

management

2 Disciplined Capital

Allocation

Investing in R&D and capacity

expansion to support organic

growth

Maintain ordinary dividends within

the defined payout ratio

Flexibility for:

Accretive and strategic

inorganic opportunities

Withstand market cycles

Consider further

shareholder returns when

appropriate

3 Liquidity and

Funding

Conservative leveraging of balance

sheet within 1-2 times adjusted

EBITDA target

Closure of $500 million

unsecured revolving credit

facility announced on 11

December 2015, which

replaced existing bilateral

loan facilities of $590 million

5 year maturity of bank

facilities

38% liquidity at Q2 FY16

(based on $500m syndicated

facilities)

Financial management consistent with investment grade credit. Ability to withstand market cycles and other unanticipated events.

PAGE 21

|

|

FY2016 GUIDANCE

Management expects full year Adjusted net operating profit to be between US$230 million and

US$250 million assuming, among other things, housing conditions in the United States continue to improve in line with our assumed forecast of new construction starts between 1.1 and 1.2 million, input prices remaining stable and an average USD/AUD exchange rate that is at or near current levels for the remainder of the year

Management cautions that although US housing activity has been improving, market conditions remain somewhat uncertain and some input costs remain volatile. Management is unable to forecast the comparable US GAAP financial measure due to uncertainty regarding the impact of actuarial estimates on asbestos-related assets and liabilities in future periods

PAGE 22

|

|

APPENDIX

|

|

U.S. MARKETPLACE

PAGE 24

|

|

AUSTRALIA & NEW ZEALAND MARKETPLACE

PAGE 25

|

|

FINANCIAL SUMMARY

Three Months and Half Year Ended 30 September

US$ Millions Q2’16 Q2’15 % Change 1H’16 1H’15 % Change

Net Sales

USA and Europe Fiber Cement $ 361.9 $ 335.4 8 $ 698.9 $ 656.9 6

Asia Pacific Fiber Cement 88.3 105.0 (16) 179.6 200.3 (10)

Total Net Sales $ 450.2 $ 440.4 2 $ 878.5 $ 857.2 2

EBIT—US$ Millions

USA and Europe Fiber Cement $ 89.4 $ 74.8 20 $ 178.9 $ 142.8 25

Asia Pacific Fiber Cement1 22.0 25.7 (14) 41.7 46.4 (10)

Research & Development (6.0) (6.8) 12 (12.0) (13.6) 12

General Corporate2 (10.1) (8.6) (17) (23.6) (19.3) (22)

Adjusted EBIT $ 95.3 $ 85.1 12 $ 185.0 $ 156.3 18

Net interest expense excluding AICF interest income (6.5) (1.6) (12.5) (2.5)

Other (expense) income (0.6) — 2.1 (3.7)

Adjusted income tax expense (22.9) (18.1) (27) (45.8) (34.6) (32)

Adjusted net operating profit $ 65.3 $ 65.4—$ 128.8 $ 115.5 12

1 Asia Pacific Fiber Cement EBIT excludes New Zealand weathertightness claims

2 Excludes Asbestos related expenses and adjustments

PAGE 26

|

|

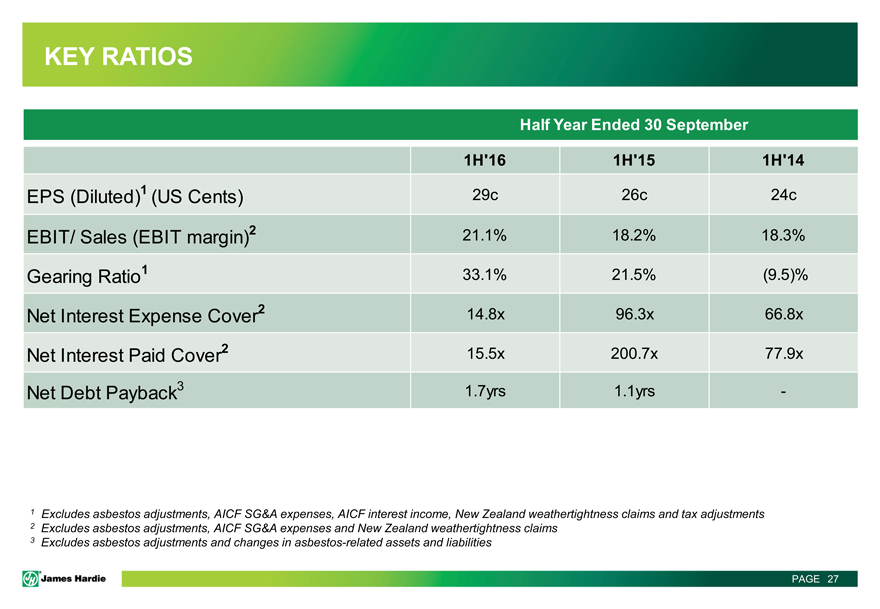

KEY RATIOS

Half Year Ended 30 September

1H’16 1H’15 1H’14

EPS (Diluted)1 (US Cents) 29c 26c 24c

EBIT/ Sales (EBIT margin)2 21.1% 18.2% 18.3%

Gearing Ratio1 33.1% 21.5% (9.5)%

Net Interest Expense Cover2 14.8x 96.3x 66.8x

Net Interest Paid Cover2 15.5x 200.7x 77.9x

Net Debt Payback3 1.7yrs 1.1yrs—

1 Excludes asbestos adjustments, AICF SG&A expenses, AICF interest income, New Zealand weathertightness claims and tax adjustments

2 Excludes asbestos adjustments, AICF SG&A expenses and New Zealand weathertightness claims

3 Excludes asbestos adjustments and changes in asbestos-related assets and liabilities

PAGE 27

|

|

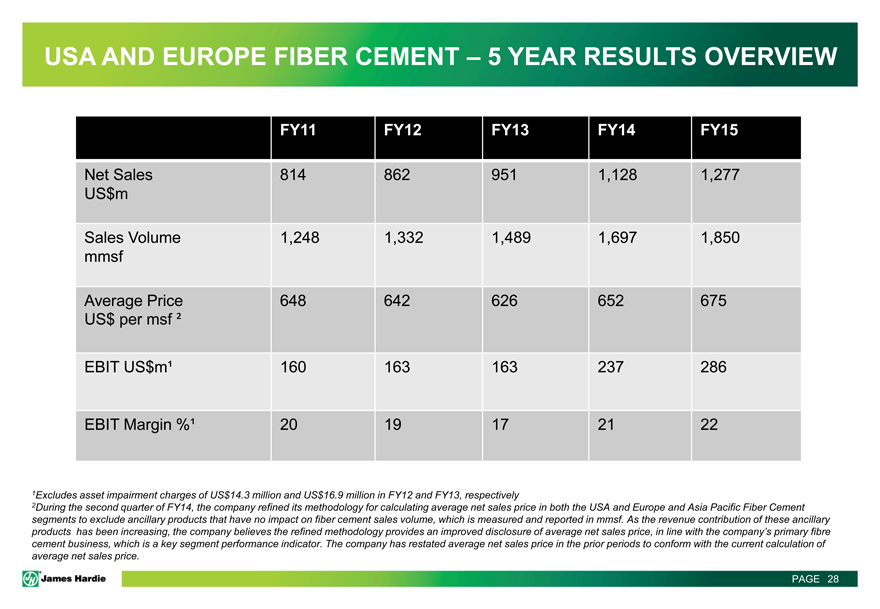

USA AND EUROPE FIBER CEMENT – 5 YEAR RESULTS OVERVIEW

FY11 FY12 FY13 FY14 FY15

Net Sales 814 862 951 1,128 1,277

US$m

Sales Volume 1,248 1,332 1,489 1,697 1,850

mmsf

Average Price 648 642 626 652 675

US$ per msf ²

EBIT US$m¹ 160 163 163 237 286

EBIT Margin %¹ 20 19 17 21 22

1Excludes asset impairment charges of US$14.3 million and US$16.9 million in FY12 and FY13, respectively

2During the second quarter of FY14, the company refined its methodology for calculating average net sales price in both the USA and Europe and Asia Pacific Fiber Cement

segments to exclude ancillary products that have no impact on fiber cement sales volume, which is measured and reported in mmsf. As the revenue contribution of these ancillary

products has been increasing, the company believes the refined methodology provides an improved disclosure of average net sales price, in line with the company’s primary fibre

cement business, which is a key segment performance indicator. The company has restated average net sales price in the prior periods to conform with the current calculation of

average net sales price.

PAGE 28

|

|

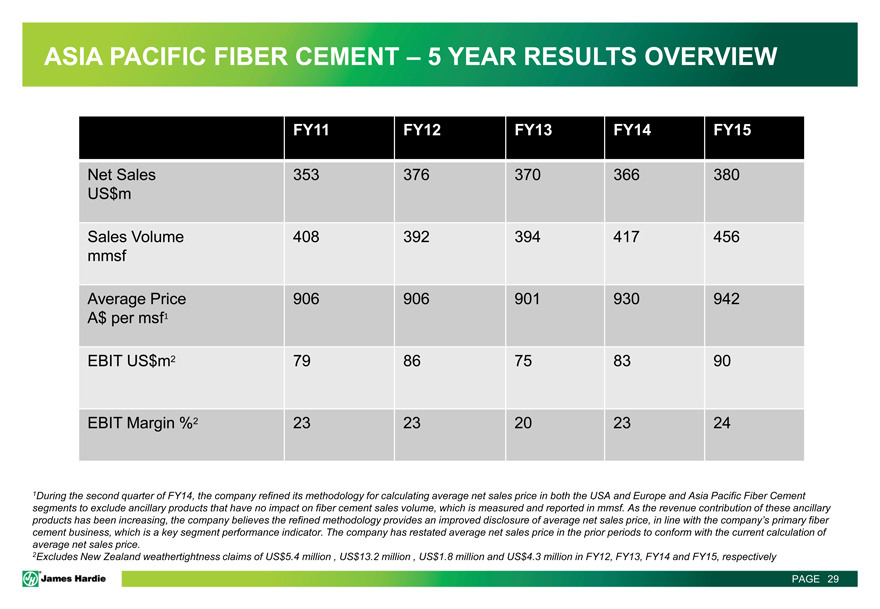

ASIA PACIFIC FIBER CEMENT – 5 YEAR RESULTS OVERVIEW

FY11 FY12 FY13 FY14 FY15

Net Sales 353 376 370 366 380

US$m

Sales Volume 408 392 394 417 456

mmsf

Average Price 906 906 901 930 942

A$ per msf1

EBIT US$m2 79 86 75 83 90

EBIT Margin %2 23 23 20 23 24

1During the second quarter of FY14, the company refined its methodology for calculating average net sales price in both the USA and Europe and Asia Pacific Fiber Cement

segments to exclude ancillary products that have no impact on fiber cement sales volume, which is measured and reported in mmsf. As the revenue contribution of these ancillary

products has been increasing, the company believes the refined methodology provides an improved disclosure of average net sales price, in line with the company’s primary fiber

cement business, which is a key segment performance indicator. The company has restated average net sales price in the prior periods to conform with the current calculation of

average net sales price.

2Excludes New Zealand weathertightness claims of US$5.4 million , US$13.2 million , US$1.8 million and US$4.3 million in FY12, FY13, FY14 and FY15, respectively

PAGE 29

|

|

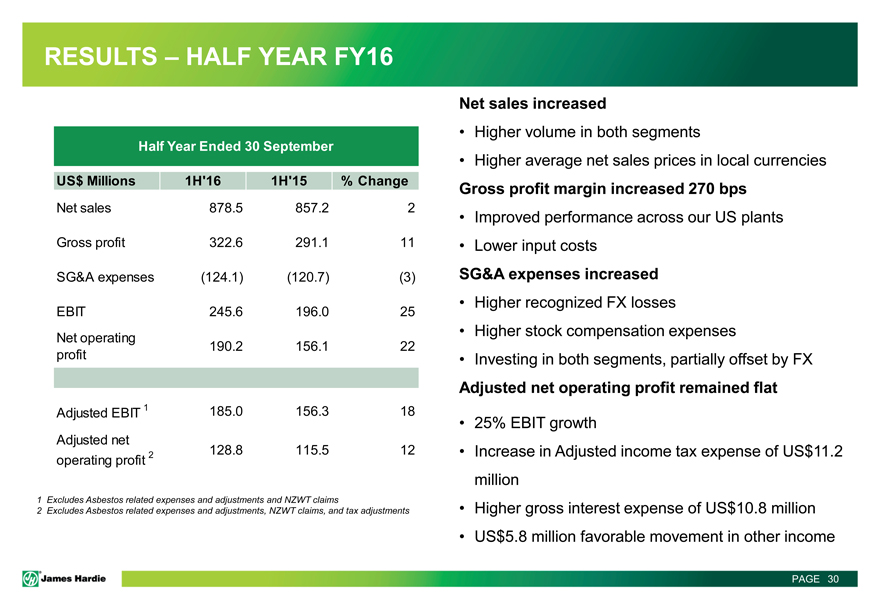

RESULTS – HALF YEAR FY16

Half Year Ended 30 September

US$ Millions 1H’16 1H’15 % Change

Net sales 878.5 857.2 2

Gross profit 322.6 291.1 11

SG&A expenses (124.1) (120.7) (3)

EBIT 245.6 196.0 25

Net operating

profit 190.2 156.1 22

Adjusted EBIT 1 185.0 156.3 18

Adjusted net

operating profit 2 128.8 115.5 12

1 Excludes Asbestos related expenses and adjustments and NZWT claims

2 Excludes Asbestos related expenses and adjustments, NZWT claims, and tax adjustments

Net sales increased

Higher volume in both segments

Higher average net sales prices in local currencies

Gross profit margin increased 270 bps

Improved performance across our US plants

Lower input costs

SG&A expenses increased

Higher recognized FX losses

Higher stock compensation expenses

Investing in both segments, partially offset by FX

Adjusted net operating profit remained flat

25% EBIT growth

Increase in Adjusted income tax expense of US$11.2

million

Higher gross interest expense of US$10.8 million

US$5.8 million favorable movement in other income

PAGE 30

|

|

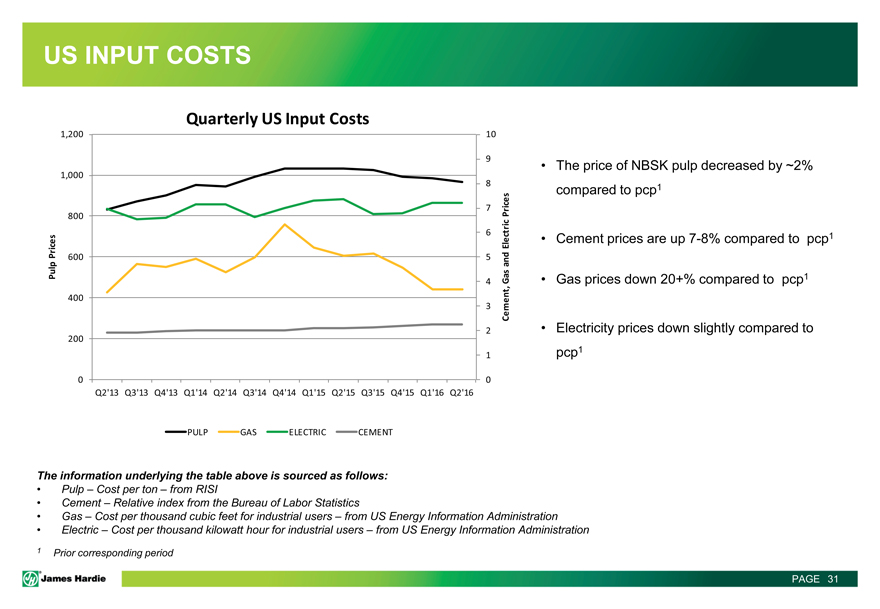

US INPUT COSTS

Quarterly US Input Costs

Pulp Prices

1,200 1,000 800 600 400 200 0

Q2’13 Q3’13 Q4’13 Q1’14 Q2’14 Q3’14 Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16

PULP GAS ELECTRIC CEMENT

10 9 8 7 6 5 4 3 2 1 0

Cement, Gas and Electric Prices

The price of NBSK pulp decreased by ~2% compared to pcp1

Cement prices are up 7-8% compared to pcp1

Gas prices down 20+% compared to pcp1

Electricity prices down slightly compared to pcp1

The information underlying the table above is sourced as follows:

Pulp – Cost per ton – from RISI

Cement – Relative index from the Bureau of Labor Statistics

Gas – Cost per thousand cubic feet for industrial users – from US Energy Information Administration

Electric – Cost per thousand kilowatt hour for industrial users – from US Energy Information Administration

1 Prior corresponding period

PAGE 31

|

|

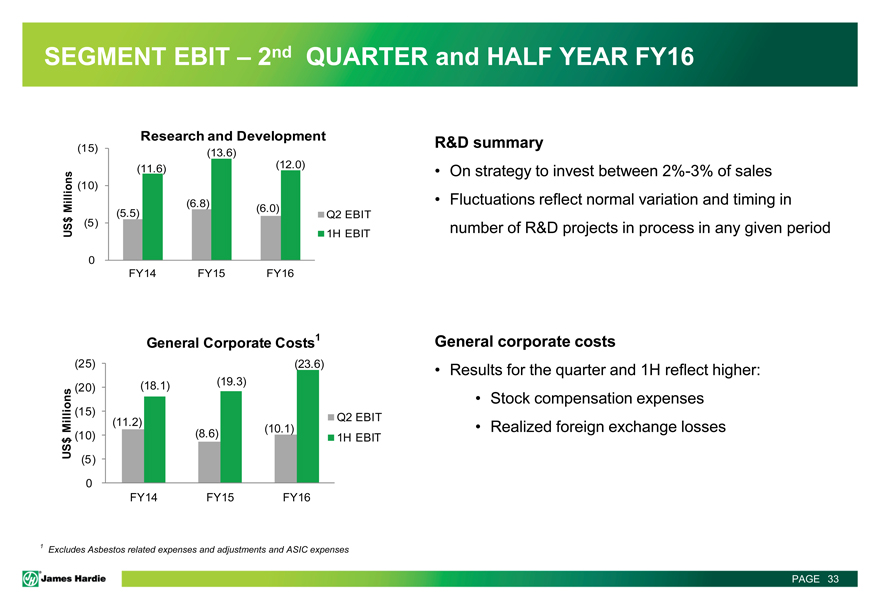

SEGMENT EBIT – 2nd QUARTER and HALF YEAR FY16

USA and Europe Fiber Cement

200

178.9

150 142.8

126.7

100 89.4 Q2 EBIT

67.3 74.8 1H EBIT

50

0

FY14 FY15 FY16

Asia Pacific Fiber Cement1

60 55.4

49.9

50 45.3

40

30 27.7 30.0 Q2 EBIT

23.9 1H EBIT

20

10

0

FY14 FY15 FY16

A$ Millions US$ Millions

1 Excludes New Zealand weathertightness claims

2 Excludes Australian Pipes business which was sold in Q1 FY16

USA and Europe Fiber Cement EBIT summary

Quarter and 1H EBIT increased by 20% and 25%,

respectively when compared to pcp

Primarily driven by plant performance and lower input

costs

Asia Pacific Fiber Cement EBIT1 summary

EBIT in local currency for the quarter and 1H increased

8% and 11%, respectively when compared to pcp

Increase reflects higher volume2 and price, partially offset

by production costs

PAGE 32

|

|

SEGMENT EBIT – 2nd QUARTER and HALF YEAR FY16

US$ Millions

US$ Millions

Research and Development

(15) (13.6)

(11.6) (12.0)

(10)

(6.8) (6.0)

(5.5) Q2 EBIT

(5)

1H EBIT

0

FY14 FY15 FY16

General Corporate Costs1

(25) (23.6)

(20) (18.1) (19.3)

(15)

(11.2) Q2 EBIT

(10) (8.6) (10.1) 1H EBIT

(5)

0

FY14 FY15 FY16

R&D summary

On strategy to invest between 2%-3% of sales

Fluctuations reflect normal variation and timing in

number of R&D projects in process in any given period

General corporate costs

Results for the quarter and 1H reflect higher:

Stock compensation expenses

Realized foreign exchange losses

1 Excludes Asbestos related expenses and adjustments and ASIC expenses

PAGE 33

|

|

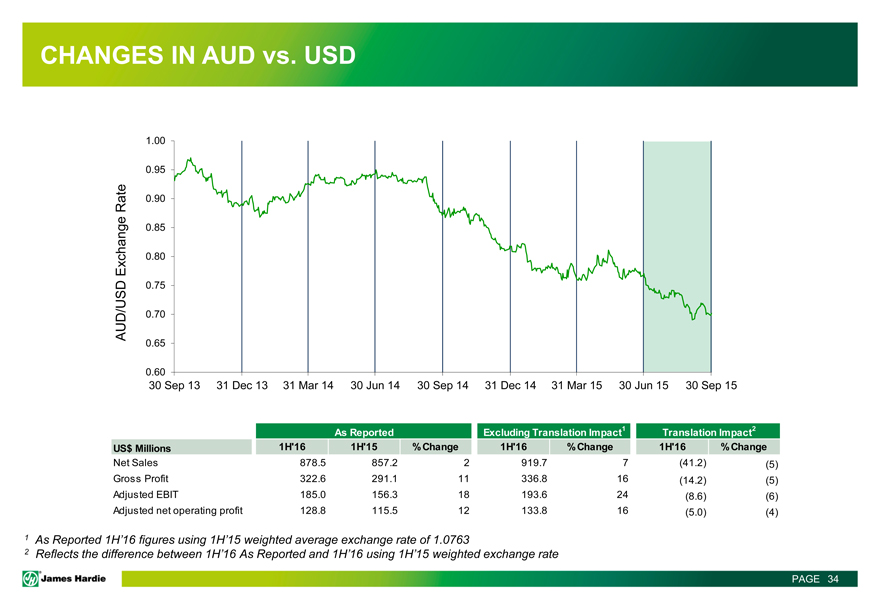

CHANGES IN AUD vs. USD

AUD/USD Exchange Rate

1.00

0.95

0.90

0.85

0.80

0.75

0.70

0.65

0.60

30 Sep 13 31 Dec 13 31 Mar 14 30 Jun 14 30 Sep 14 31 Dec 14 31 Mar 15 30 Jun 15 30 Sep 15

As Reported Excluding Translation Impact1 Translation Impact2

US$ Millions 1H’16 1H’15 % Change 1H’16 % Change 1H’16 % Change

Net Sales 878.5 857.2 2 919.7 7 (41.2) (5)

Gross Profit 322.6 291.1 11 336.8 16 (14.2) (5)

Adjusted EBIT 185.0 156.3 18 193.6 24 (8.6) (6)

Adjusted net operating profit 128.8 115.5 12 133.8 16 (5.0) (4)

1 As Reported 1H’16 figures using 1H’15 weighted average exchange rate of 1.0763

2 Reflects the difference between 1H’16 As Reported and 1H’16 using 1H’15 weighted exchange rate

PAGE 34

|

|

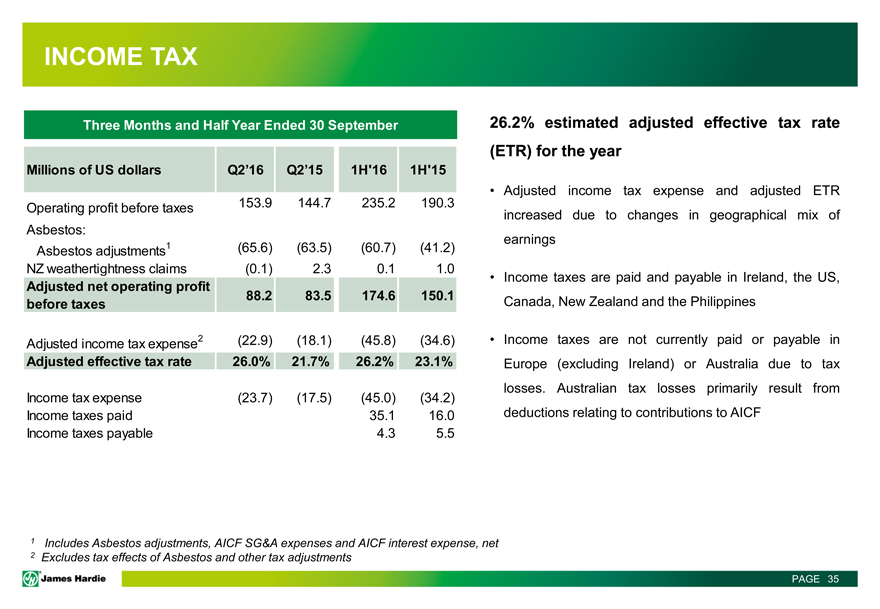

INCOME TAX

Three Months and Half Year Ended 30 September

Millions of US dollars Q2’16 Q2’15 1H’16 1H’15

Operating profit before taxes 153.9 144.7 235.2 190.3

Asbestos:

Asbestos adjustments1 (65.6) (63.5) (60.7) (41.2)

NZ weathertightness claims (0.1) 2.3 0.1 1.0

Adjusted net operating profit

before taxes 88.2 83.5 174.6 150.1

Adjusted income tax expense2 (22.9) (18.1) (45.8) (34.6)

Adjusted effective tax rate 26.0% 21.7% 26.2% 23.1%

Income tax expense (23.7) (17.5) (45.0) (34.2)

Income taxes paid 35.1 16.0

Income taxes payable 4.3 5.5

26.2% estimated adjusted effective tax rate

(ETR) for the year

Adjusted income tax expense and adjusted ETR

increased due to changes in geographical mix of

earnings

Income taxes are paid and payable in Ireland, the US,

Canada, New Zealand and the Philippines

Income taxes are not currently paid or payable in

Europe (excluding Ireland) or Australia due to tax

losses. Australian tax losses primarily result from

deductions relating to contributions to AICF

1 Includes Asbestos adjustments, AICF SG&A expenses and AICF interest expense, net 2 Excludes tax effects of Asbestos and other tax adjustments

PAGE 35

|

|

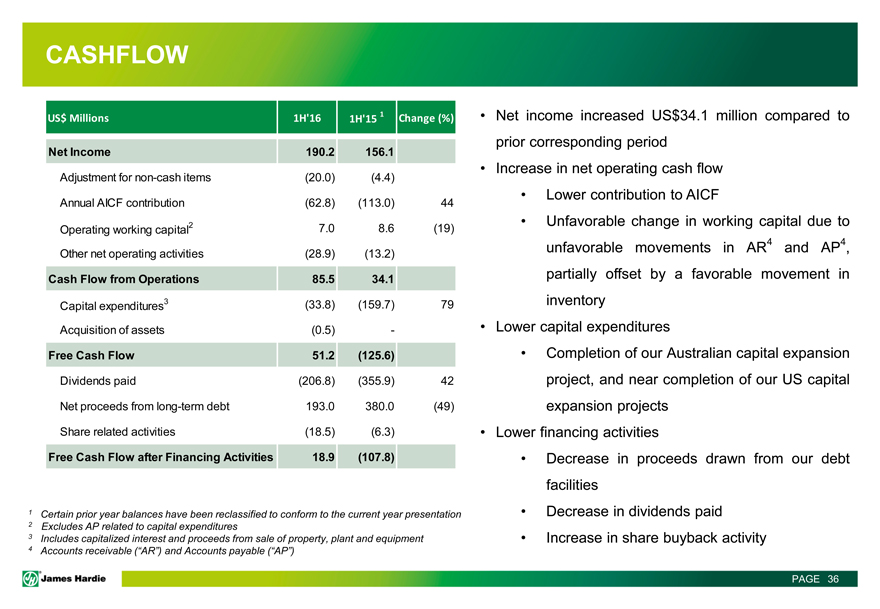

CASHFLOW

US$ Millions 1H’16 1H’15 1 Change (%)

Net Income 190.2 156.1

Adjustment for non-cash items (20.0) (4.4)

Annual AICF contribution (62.8) (113.0) 44

Operating working capital2 7.0 8.6 (19)

Other net operating activities (28.9) (13.2)

Cash Flow from Operations 85.5 34.1

Capital expenditures3 (33.8) (159.7) 79

Acquisition of assets (0.5)—

Free Cash Flow 51.2 (125.6)

Dividends paid (206.8) (355.9) 42

Net proceeds from long-term debt 193.0 380.0 (49)

Share related activities (18.5) (6.3)

Free Cash Flow after Financing Activities 18.9 (107.8)

1 Certain prior year balances have been reclassified to conform to the current year presentation

2 Excludes AP related to capital expenditures

3 Includes capitalized interest and proceeds from sale of property, plant and equipment

4 Accounts receivable (“AR”) and Accounts payable (“AP”)

Net income increased US$34.1 million compared to

prior corresponding period

Increase in net operating cash flow

Lower contribution to AICF

Unfavorable change in working capital due to

unfavorable movements in AR4 and AP4,

partially offset by a favorable movement in

inventory

Lower capital expenditures

Completion of our Australian capital expansion

project, and near completion of our US capital

expansion projects

Lower financing activities

Decrease in proceeds drawn from our debt

facilities

Decrease in dividends paid

Increase in share buyback activity

PAGE 36

|

|

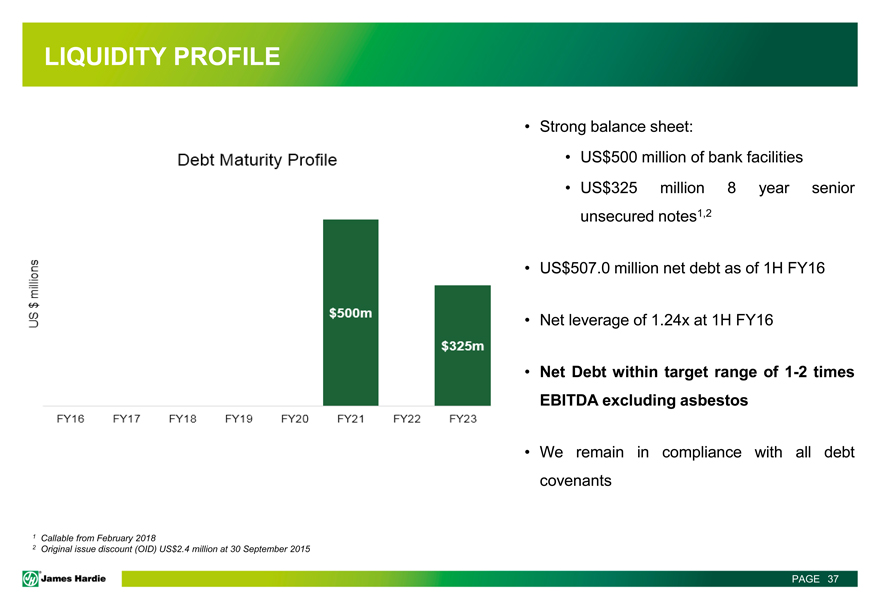

LIQUIDITY PROFILE

Debt Maturity Profile $500m $325m US$ millions

FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 1 Callable from February 2018

2 Original issue discount (OID) US$2.4 million at 30 September 2015

Strong balance sheet:

US$500 million of bank facilities

US$325 million 8 year senior

unsecured notes1,2

US$507.0 million net debt as of 1H FY16

Net leverage of 1.24x at 1H FY16

Net Debt within target range of 1-2 times

EBITDA excluding asbestos

We remain in compliance with all debt

covenants

PAGE 37

|

|

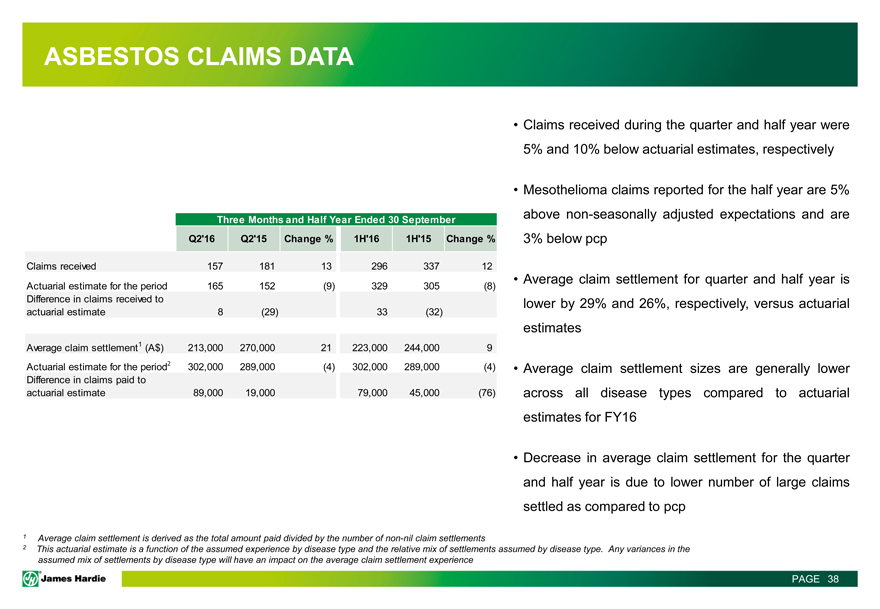

ASBESTOS CLAIMS DATA

Three Months and Half Year Ended 30 September

Q2’16 Q2’15 Change % 1H’16 1H’15 Change %

Claims received 157 181 13 296 337 12

Actuarial estimate for the period 165 152 (9) 329 305 (8)

Difference in claims received to

actuarial estimate 8 (29) 33 (32)

Average claim settlement1 (A$) 213,000 270,000 21 223,000 244,000 9

Actuarial estimate for the period2 302,000 289,000 (4) 302,000 289,000 (4)

Difference in claims paid to

actuarial estimate 89,000 19,000 79,000 45,000 (76)

Claims received during the quarter and half year were 5% and 10% below actuarial estimates, respectively

Mesothelioma claims reported for the half year are 5% above non-seasonally adjusted expectations and are 3% below pcp

Average claim settlement for quarter and half year is lower by 29% and 26%, respectively, versus actuarial estimates

Average claim settlement sizes are generally lower across all disease types compared to actuarial estimates for FY16

Decrease in average claim settlement for the quarter and half year is due to lower number of large claims settled as compared to pcp

1 Average claim settlement is derived as the total amount paid divided by the number of non-nil claim settlements

2 This actuarial estimate is a function of the assumed experience by disease type and the relative mix of settlements assumed by disease type. Any variances in the assumed mix of settlements by disease type will have an impact on the average claim settlement experience

PAGE 38

|

|

DEFINITIONS AND OTHER TERMS

This Management Presentation forms part of a package of information about the company’s results. It should be read in conjunction with the other parts of this package, including the Management’s Analysis of Results, Media Release and Consolidated Financial Statements

Definitions

Non-financial Terms

AFFA –Amended and Restated Final Funding Agreement

AICF –Asbestos Injuries Compensation Fund Ltd

NBSK –Northern Bleached Soft Kraft; the company’s benchmark grade of pulp

Legacy New Zealand weathertightness claims (“New Zealand weathertightness claims”) –Expenses arising from defending and resolving claims in New Zealand that allege poor building design, inadequate certification of plans, inadequate construction review and compliance certification and deficient work by sub-contractors

PAGE 39

|

|

DEFINITIONS AND OTHER TERMS

Financial Measures – US GAAP equivalents

This document contains financial statement line item descriptions that are considered to be non-US GAAP, but are consistent with those used by Australian companies. Because the company prepares its Consolidated Financial Statements under US GAAP, the following table cross-references each non-US GAAP line item description, as used in Management’s Analysis of Results and Media Release, to the equivalent US GAAP financial statement line item description used in the company’s Condensed Consolidated Financial Statements:

Management’s Analysis of Results and Media Release

Net sales

Cost of goods sold Gross profit

Selling, general and administrative expenses Research and development expenses

Asbestos adjustments EBIT*

Net interest income (expense)*

Other income (expense)

Operating profit (loss) before income taxes*

Income tax (expense) benefit

Net operating profit (loss)*

Consolidated Statements of Operations and Other Comprehensive Income (Loss) (US GAAP)

Net sales

Cost of goods sold Gross profit

Selling, general and administrative expenses Research and development expenses

Asbestos adjustments Operating income (loss)

Sum of interest expense and interest income

Other income (expenses)

Income (loss) before income taxes

Income tax (expense) benefit

Net income (loss)

*- Represents non-us GAAP descriptions used by Australian companies. PAGE 40

|

|

DEFINITIONS AND OTHER TERMS

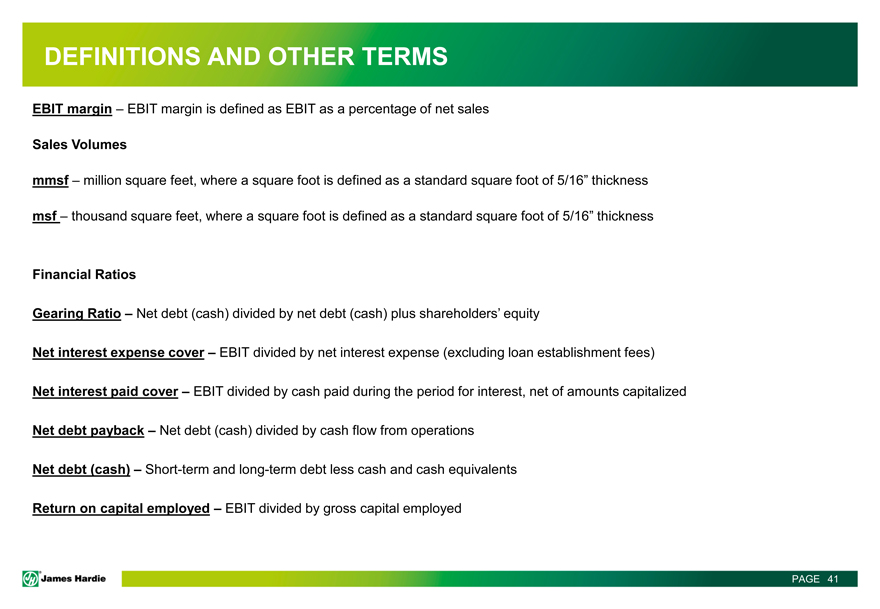

EBIT margin – EBIT margin is defined as EBIT as a percentage of net sales

Sales Volumes mmsf –million square feet, where a square foot is defined as a standard square foot of 5/16” thickness msf –thousand square feet, where a square foot is defined as a standard square foot of 5/16” thickness

Financial Ratios

Gearing Ratio –Net debt (cash) divided by net debt (cash) plus shareholders’ equity

Net interest expense cover –EBIT divided by net interest expense (excluding loan establishment fees) Net interest paid cover –EBIT divided by cash paid during the period for interest, net of amounts capitalized Net debt payback –Net debt (cash) divided by cash flow from operations Net debt (cash) –Short-term and long-term debt less cash and cash equivalents Return on capital employed –EBIT divided by gross capital employed

PAGE 41

|

|

NON-US GAAP FINANCIAL MEASURES

Adjusted EBIT and Adjusted EBIT margin –Adjusted EBIT and Adjusted EBIT margin are not measures of financial performance under

US GAAP and should not be considered to be more meaningful than EBIT and EBIT margin. Management has included these financial

measures to provide investors with an alternative method for assessing its operating results in a manner that is focused on the

performance of its ongoing operations and provides useful information regarding its financial condition and results of operations.

Management uses these non-US GAAP measures for the same purposes.

US$ Millions Three Months and Half Year Ended 30 September

Q2’16 Q2’15 1H’16 1H’15

EBIT $ 161.1 $ 145.6 $ 245.6 $ 196.0

Asbestos:

Asbestos adjustments (66.0) (63.5) (61.5) (42.0)

AICF SG&A expenses 0.3 0.7 0.8 1.3

New Zealand weathertightness claims (0.1) 2.3 0.1 1.0

Adjusted EBIT 95.3 85.1 185.0 156.3

Net sales $ 450.2 $ 440.4 $ 878.5 $ 857.2

Adjusted EBIT margin 21.2% 19.3% 21.1% 18.2%

PAGE 42

|

|

NON-US GAAP FINANCIAL MEASURES

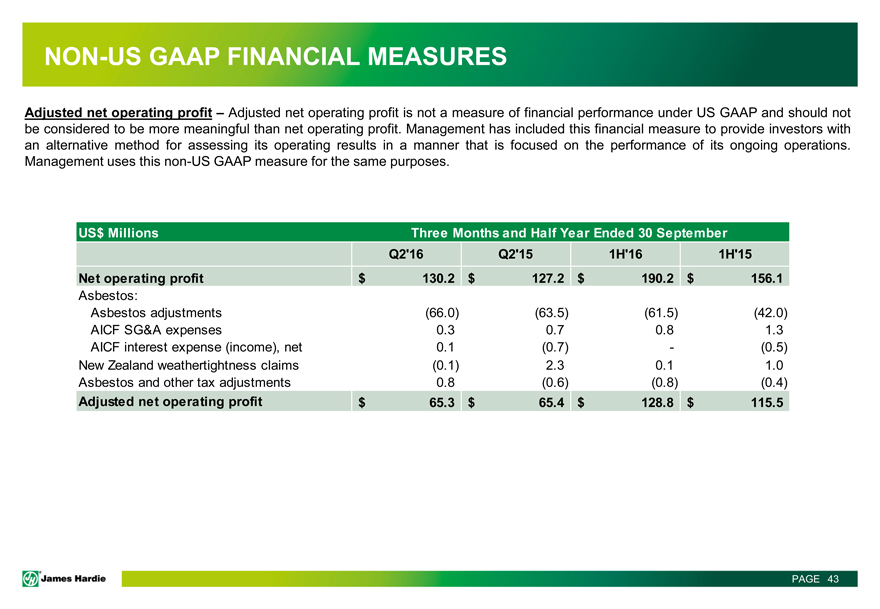

Adjusted net operating profit –Adjusted net operating profit is not a measure of financial performance under US GAAP and should not

be considered to be more meaningful than net operating profit. Management has included this financial measure to provide investors with

an alternative method for assessing its operating results in a manner that is focused on the performance of its ongoing operations.

Management uses this non-US GAAP measure for the same purposes.

US$ Millions Three Months and Half Year Ended 30 September

Q2’16 Q2’15 1H’16 1H’15

Net operating profit $ 130.2 $ 127.2 $ 190.2 $ 156.1

Asbestos:

Asbestos adjustments (66.0) (63.5) (61.5) (42.0)

AICF SG&A expenses 0.3 0.7 0.8 1.3

AICF interest expense (income), net 0.1 (0.7) — (0.5)

New Zealand weathertightness claims (0.1) 2.3 0.1 1.0

Asbestos and other tax adjustments 0.8 (0.6) (0.8) (0.4)

Adjusted net operating profit $ 65.3 $ 65.4 $ 128.8 $ 115.5

PAGE 43

|

|

NON-US GAAP FINANCIAL MEASURES

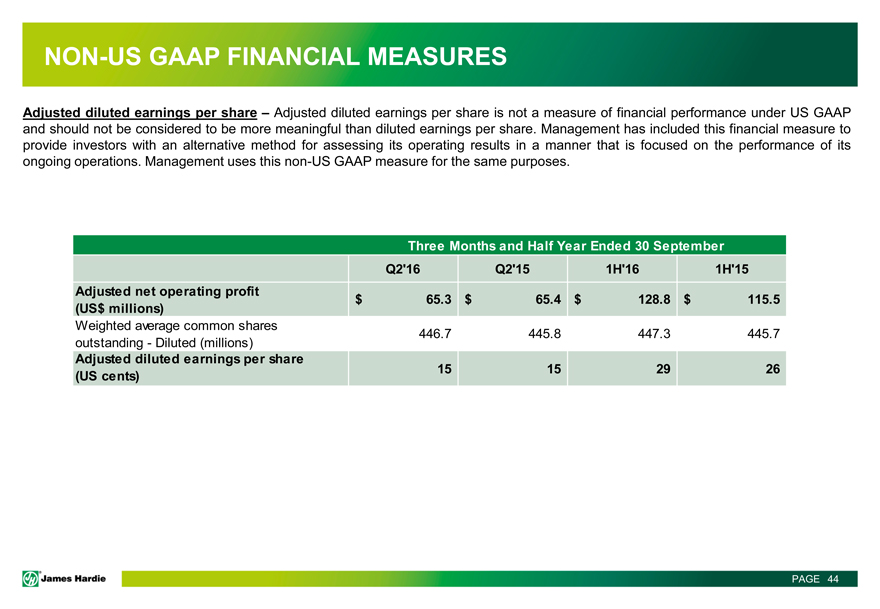

Adjusted diluted earnings per share –Adjusted diluted earnings per share is not a measure of financial performance under US GAAP

and should not be considered to be more meaningful than diluted earnings per share. Management has included this financial measure to

provide investors with an alternative method for assessing its operating results in a manner that is focused on the performance of its

ongoing operations. Management uses this non-US GAAP measure for the same purposes.

Three Months and Half Year Ended 30 September

Q2’16 Q2’15 1H’16 1H’15

Adjusted net operating profit $ 65.3 $ 65.4 $ 128.8 $ 115.5

(US$ millions)

Weighted average common shares 446.7 445.8 447.3 445.7

outstanding—Diluted (millions)

Adjusted diluted earnings per share

(US cents) 15 15 29 26

PAGE 44

|

|

NON-US GAAP FINANCIAL MEASURES

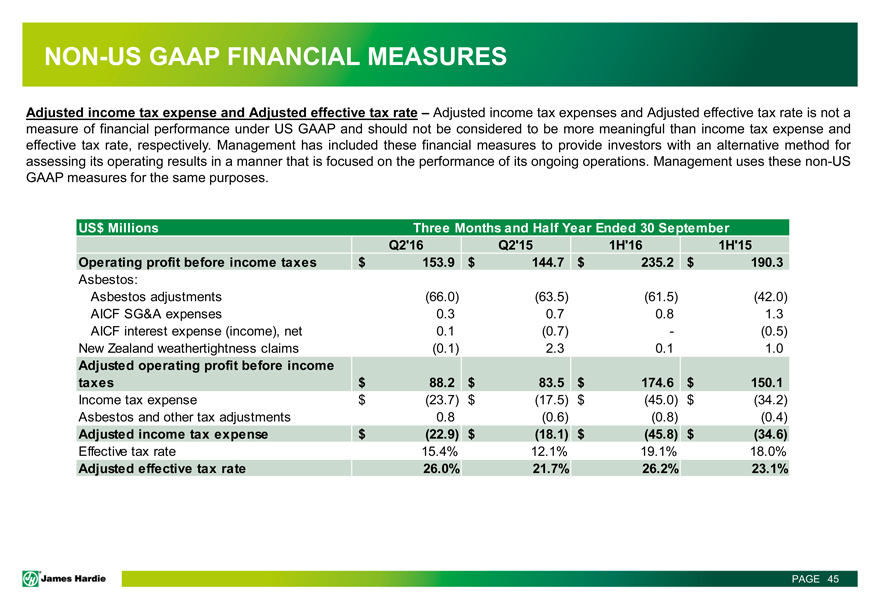

Adjusted income tax expense and Adjusted effective tax rate –Adjusted income tax expenses and Adjusted effective tax rate is not a

measure of financial performance under US GAAP and should not be considered to be more meaningful than income tax expense and

effective tax rate, respectively. Management has included these financial measures to provide investors with an alternative method for

assessing its operating results in a manner that is focused on the performance of its ongoing operations. Management uses these non-US

GAAP measures for the same purposes.

US$ Millions Three Months and Half Year Ended 30 September

Q2’16 Q2’15 1H’16 1H’15

Operating profit before income taxes $ 153.9 $ 144.7 $ 235.2 $ 190.3

Asbestos:

Asbestos adjustments (66.0) (63.5) (61.5) (42.0)

AICF SG&A expenses 0.3 0.7 0.8 1.3

AICF interest expense (income), net 0.1 (0.7) — (0.5)

New Zealand weathertightness claims (0.1) 2.3 0.1 1.0

Adjusted operating profit before income

taxes $ 88.2 $ 83.5 $ 174.6 $ 150.1

Income tax expense $ (23.7) $ (17.5) $ (45.0) $ (34.2)

Asbestos and other tax adjustments 0.8 (0.6) (0.8) (0.4)

Adjusted income tax expense $ (22.9) $ (18.1) $ (45.8) $ (34.6)

Effective tax rate 15.4% 12.1% 19.1% 18.0%

Adjusted effective tax rate 26.0% 21.7% 26.2% 23.1%

PAGE 45

|

|

NON-US GAAP FINANCIAL MEASURES

Adjusted EBITDA – is not a measure of financial performance under US GAAP and should not be considered an alternative to,

or more meaningful than, income from operations, net income or cash flows as defined by US GAAP or as a measure of

profitability or liquidity. Not all companies calculate Adjusted EBITDA in the same manner as James Hardie has and, accordingly,

Adjusted EBITDA may not be comparable with other companies. Management has included information concerning Adjusted

EBITDA because it believes that this data is commonly used by investors to evaluate the ability of a company’s earnings from its

core business operations to satisfy its debt, capital expenditure and working capital requirements.

US$ Millions Three Months and Half Year Ended 30 September

Q2’16 Q2’15 1H’16 1H’15

EBIT $ 161.1 $ 145.6 $ 245.6 $ 196.0

Depreciation and amortization 17.6 17.5 35.8 34.1

Adjusted EBITDA $ 178.7 $ 163.1 $ 281.4 $ 230.1

PAGE 46

|

|

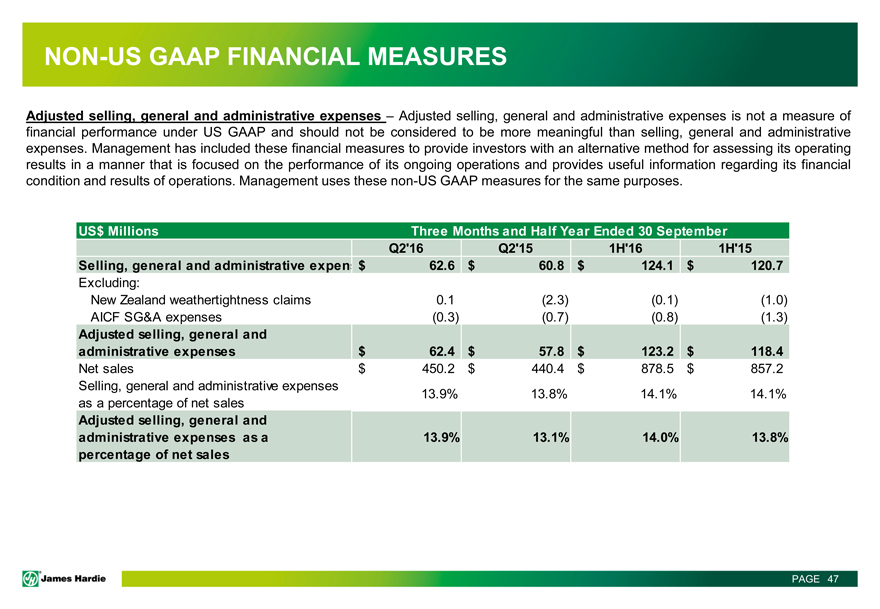

NON-US GAAP FINANCIAL MEASURES

Adjusted selling, general and administrative expenses – Adjusted selling, general and administrative expenses is not a measure of

financial performance under US GAAP and should not be considered to be more meaningful than selling, general and administrative

expenses. Management has included these financial measures to provide investors with an alternative method for assessing its operating

results in a manner that is focused on the performance of its ongoing operations and provides useful information regarding its financial

condition and results of operations. Management uses these non-US GAAP measures for the same purposes.

US$ Millions Three Months and Half Year Ended 30 September

Q2’16 Q2’15 1H’16 1H’15

Selling, general and administrative expen $ 62.6 $ 60.8 $ 124.1 $ 120.7

Excluding:

New Zealand weathertightness claims 0.1 (2.3) (0.1) (1.0)

AICF SG&A expenses (0.3) (0.7) (0.8) (1.3)

Adjusted selling, general and

administrative expenses $ 62.4 $ 57.8 $ 123.2 $ 118.4

Net sales $ 450.2 $ 440.4 $ 878.5 $ 857.2

Selling, general and administrative expenses 13.9% 13.8% 14.1% 14.1%

as a percentage of net sales

Adjusted selling, general and

administrative expenses as a 13.9% 13.1% 14.0% 13.8%

percentage of net sales

PAGE 47

|

|

INVESTOR PRESENTATION

JANUARY 2016