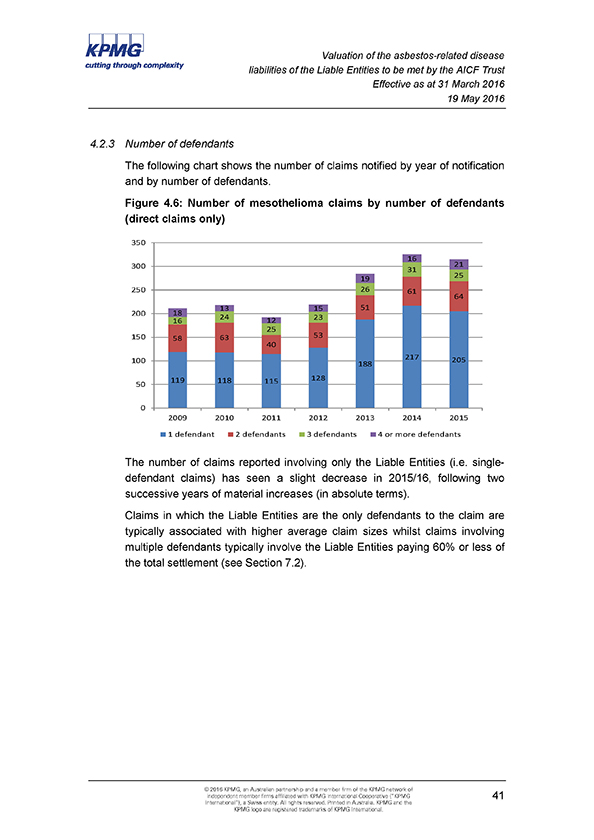

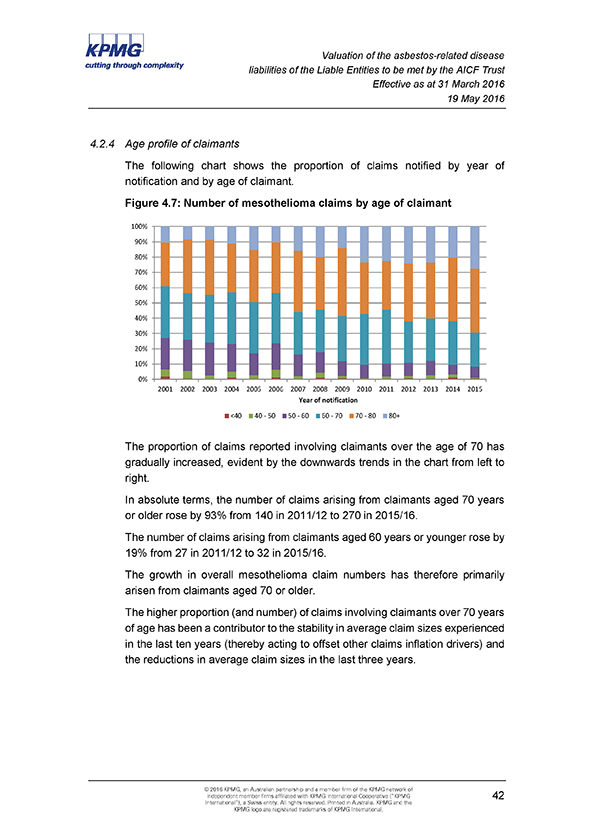

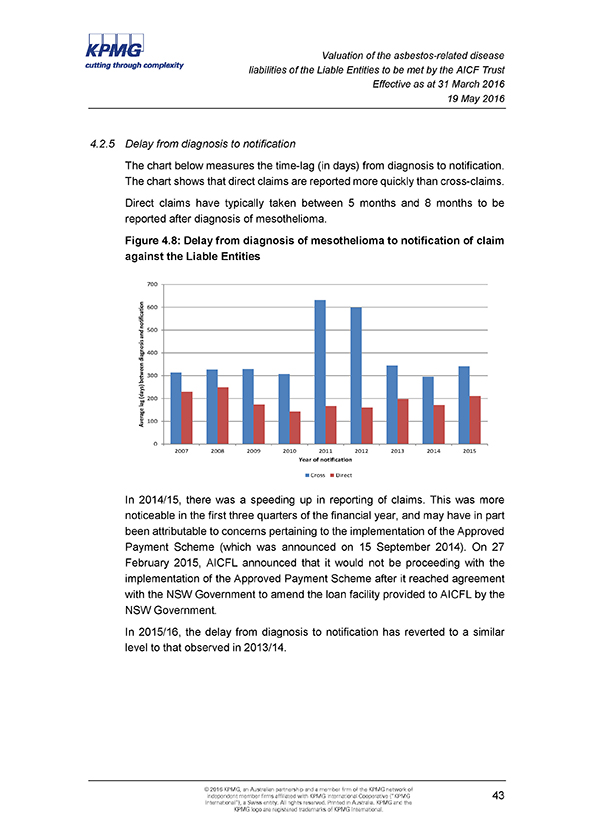

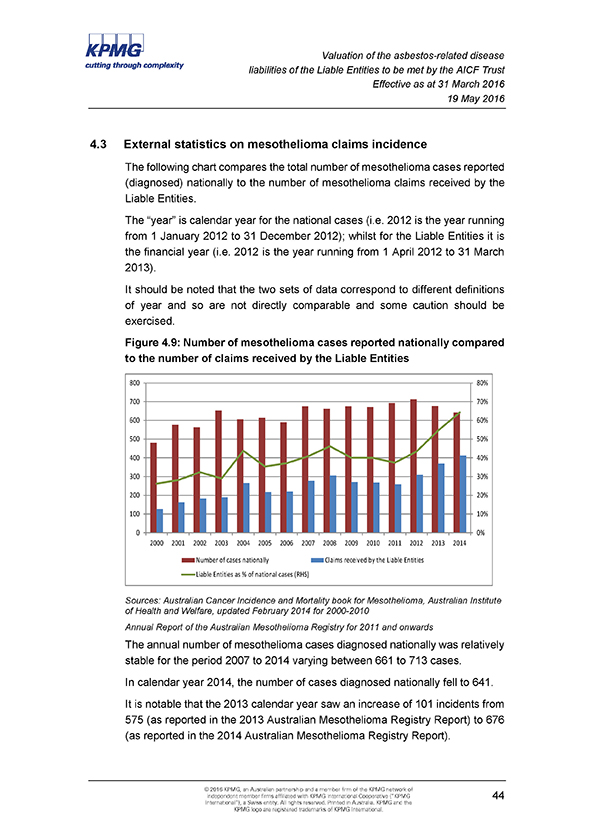

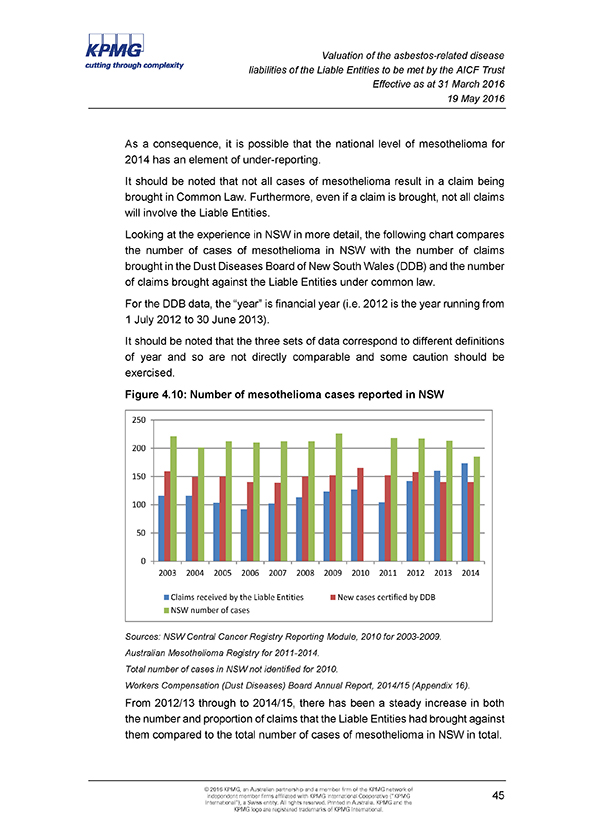

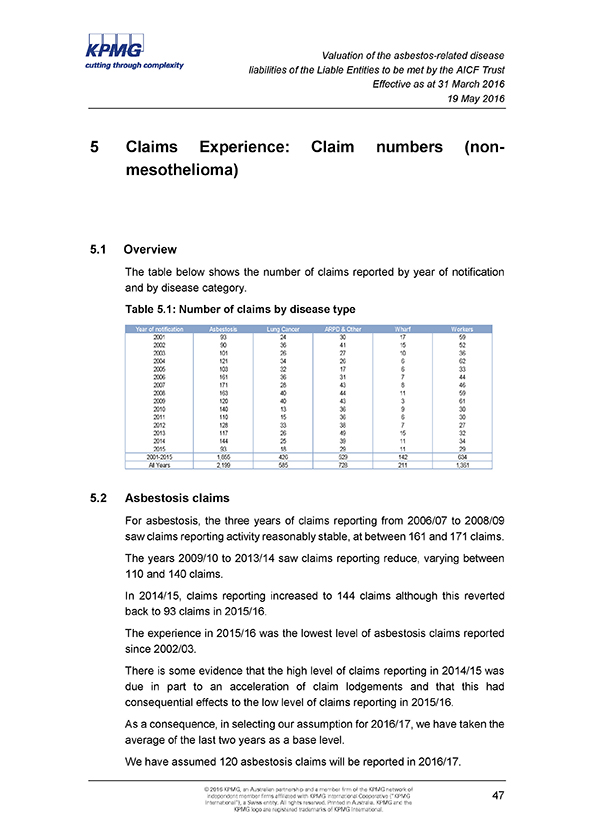

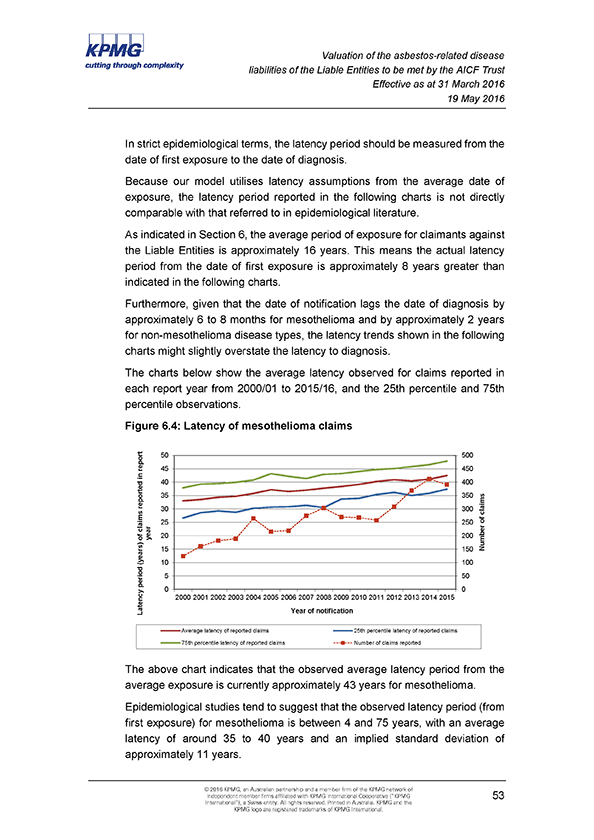

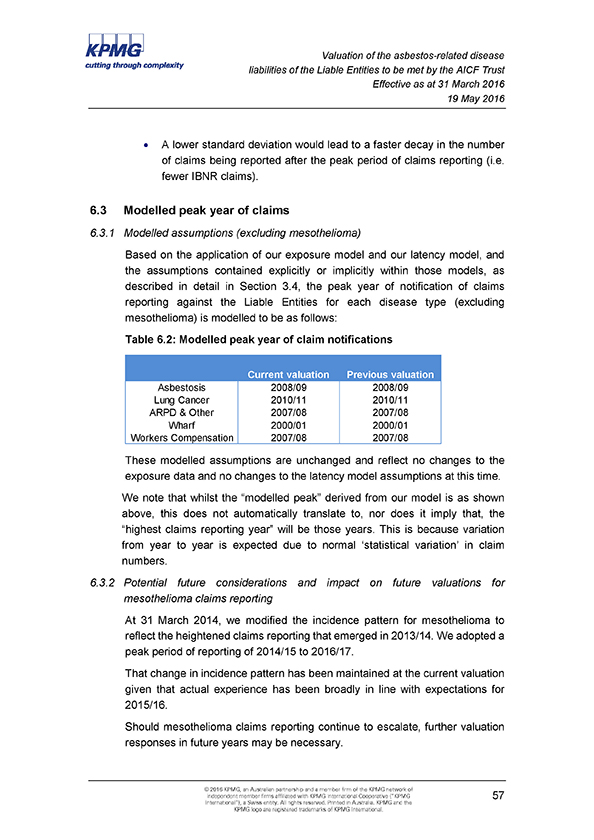

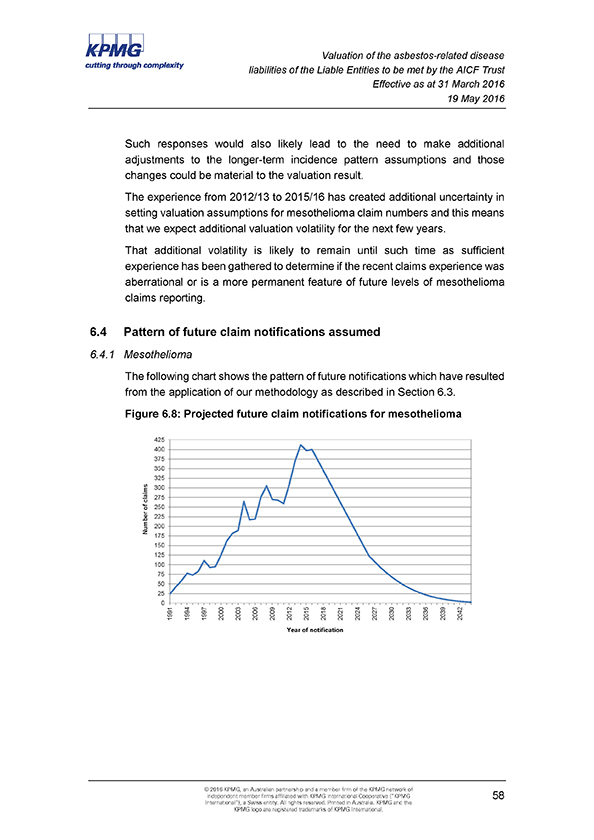

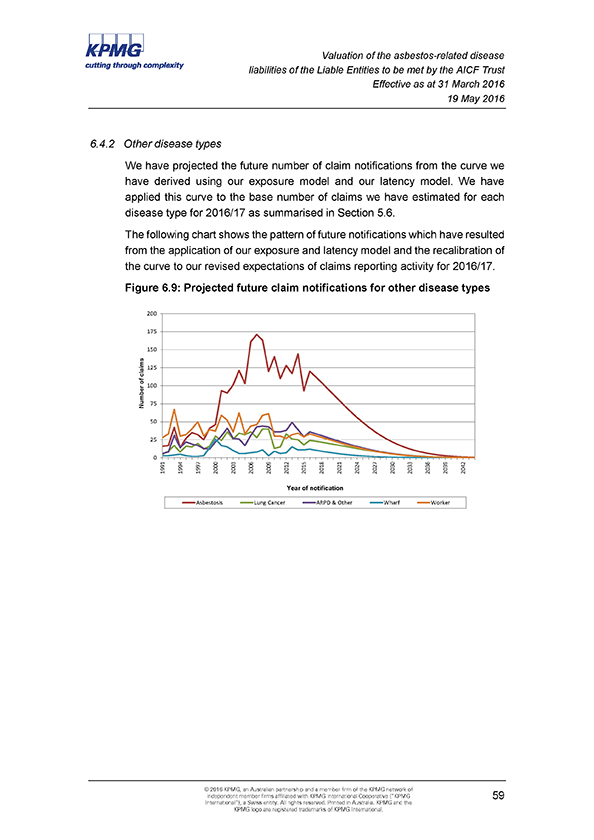

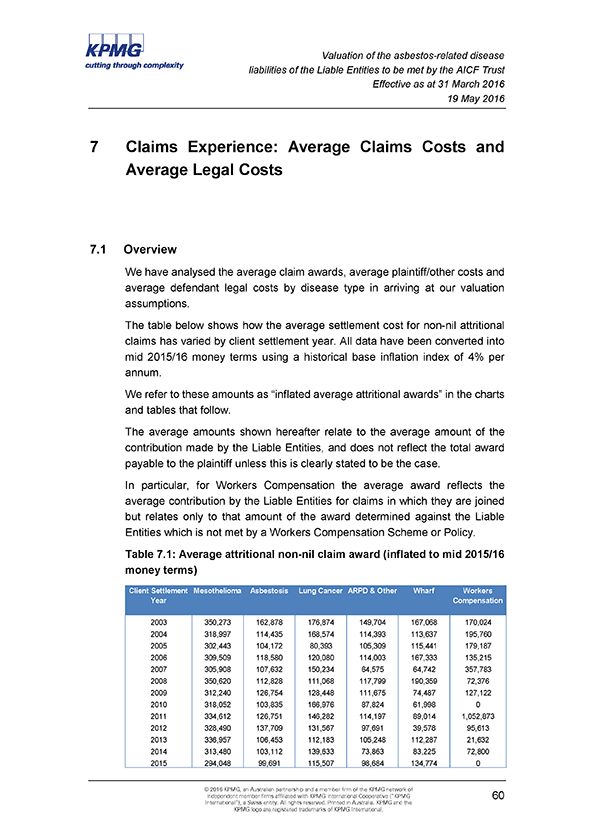

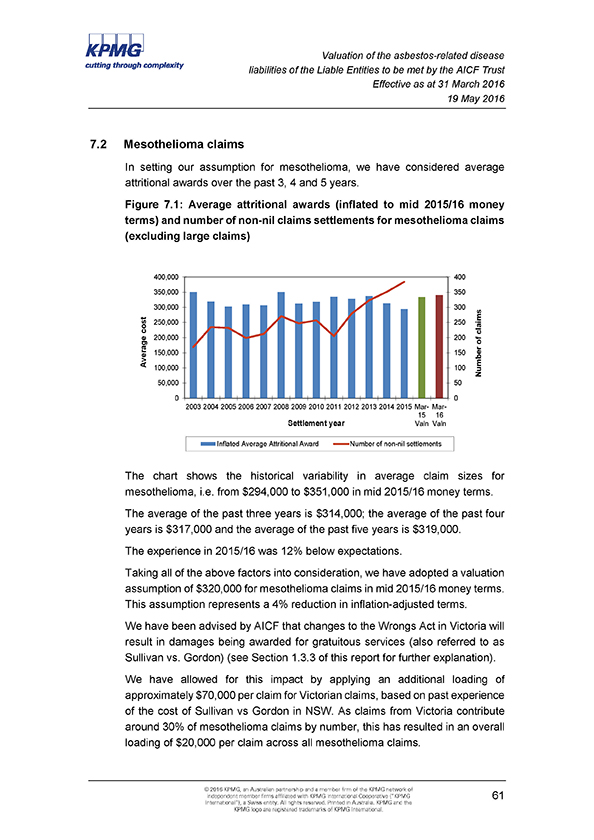

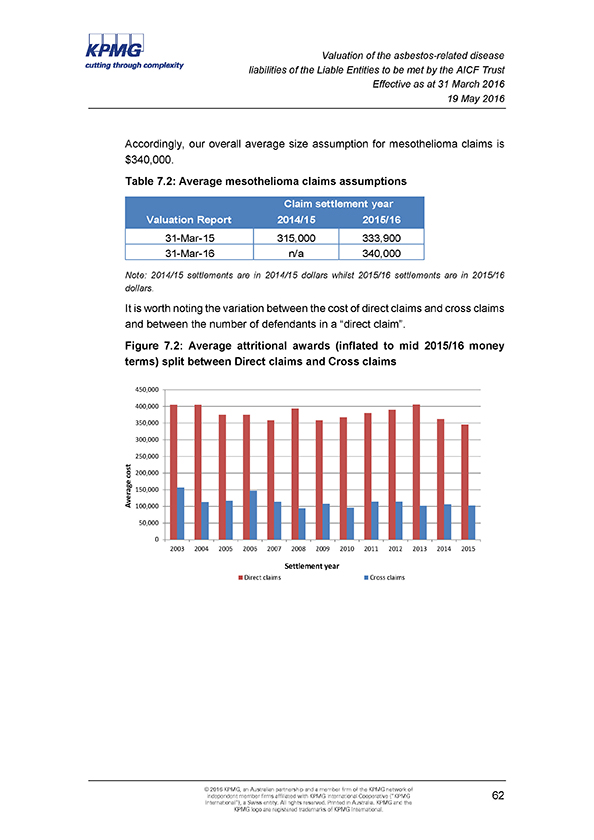

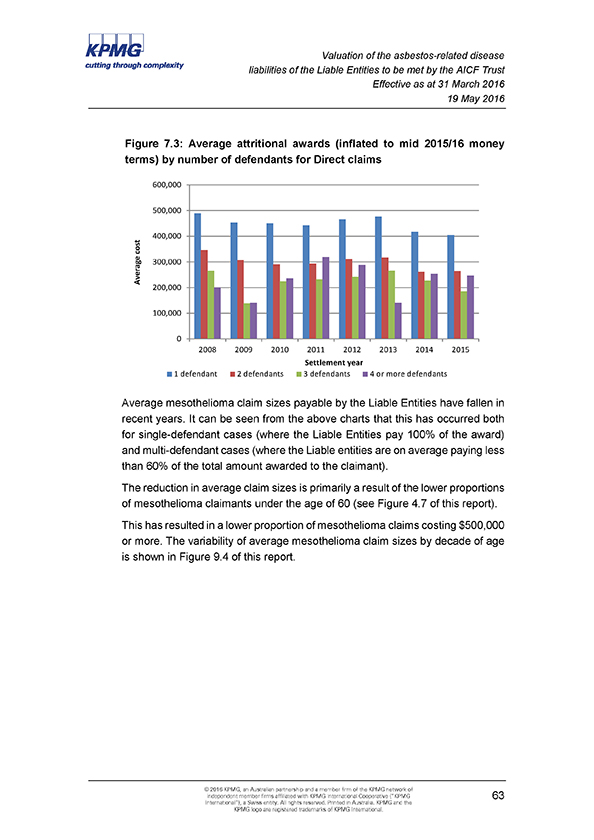

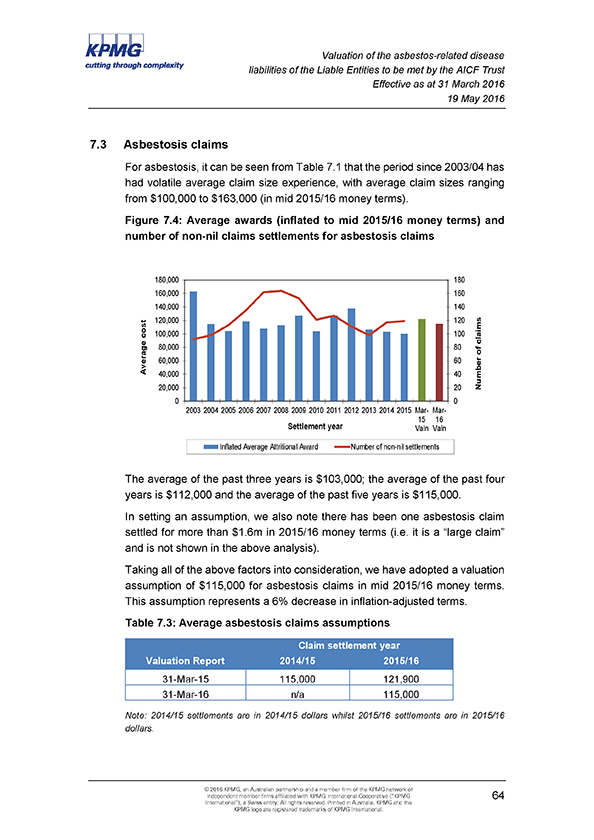

Exhibit 99.7

Valuation of Asbestos-Related Disease Liabilities of former James Hardie entities (“the Liable Entities”) to be met by the AICF Trust

Prepared for Asbestos Injuries Compensation Fund Limited (“AICFL”)

As at 31 March 2016

19 May 2016

V

aluation of Asbestos-Related Disease Liabilities of former James Hardie entities (“the Liable Entities”) to be met by the AICF Tr

ust Prepared for Asbestos Injuries Compensation Fund Limited (“AICFL”) As at 31 March 2016 19 May 2016 KPMG Actuarial Pty Ltd ABN: 91 144 686 046 Australian Financial Services Licence No. 392050 Telephone: +61 2 9335 7000 10 Shelley Street Facsimile: +61 2 9335 7001 Sydney NSW 2000 DX: 1056 Sydney www.kpmg.com.au PO Box H67 Australia Square NSW 1215 Australia 19 May 2016 Narreda Grimley General Manager Asbestos Injuries Compensation Fund Limited Suite 1, Level 6, 56 Clarence Street Sydney NSW 2000 Cc Matthew Marsh, Chief Financial Officer, James Hardie Industries plc Paul Miller, General Counsel, Department of Premier and Cabinet, The State of New South Wales The Board of Directors, Asbestos Injuries Compensation Fund Limited Dear Narreda VALUATION OF ASBESTOS-RELATED DISEASE LIABILITIES OF FORMER JAMES HARDIE ENTITIES (“THE LIABLE ENTITIES”) TO BE MET BY THE AICF TRUST We are pleased to provide you with our Annual Actuarial Report relating to the asbestos-related disease liabilities of the Liable Entities which are to be met by the AICF Trust. The report is effective as at 31 March 2016 and has taken into account claims data and information provided to us by AICFL as at 31 March 2016. If you have any questions with respect to the contents of this report, please do not hesitate to contact us. Yours sincerely Neil Donlevy MA FIA FIAA Jefferson Gibbs BSc FIA FIAA Executive, KPMG Actuarial Pty Ltd Executive, KPMG Actuarial Pty Ltd Fellow of the Institute of Actuaries (London) Fellow of the Institute of Actuaries (London) Fellow of the Institute of Actuaries of Fellow of the Institute of Actuaries of Australia Australia © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

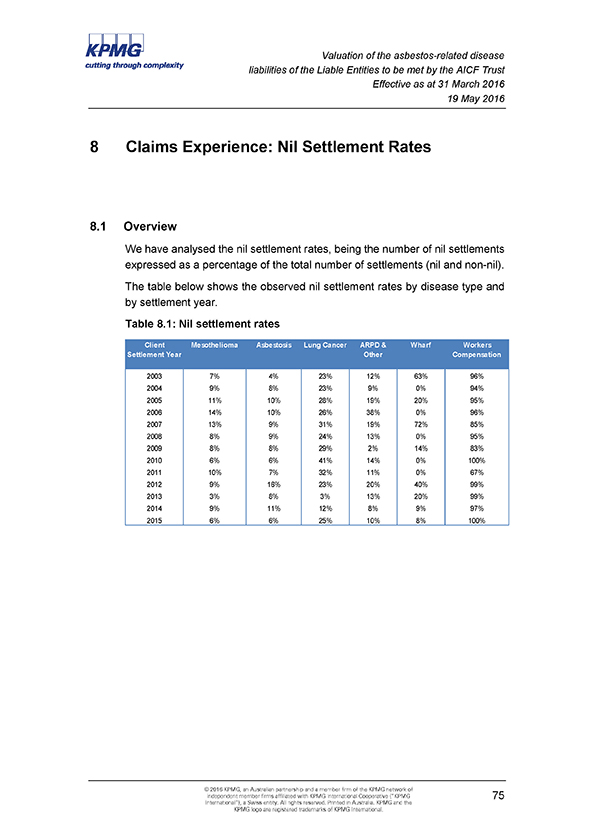

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Table of Contents Executive Summary . i 1 Scope and Purpose. 1 1.1 Introduction .1 1.2 Scope of report. 2 1.3 Areas of potential exposure . 6 1.4 Data reliances and limitations. 9 1.5 Uncertainty .9 1.6 Distribution and use. 10 1.7 Date labelling convention used in this Report . 10 1.8 Author of the report . 11 1.9 Professional standards and compliance . 11 1.10 Control processes and review . 12 1.11 Funding position of the AICF Trust . 12 1.12 Basis of preparation of Report . 12 2 Data . 13 2.1 Data provided to KPMG Actuarial . 13 2.2 Data limitations. 13 2.3 Data reconciliation and testing. 14 2.4 Data conclusion. 17 3 Valuation Methodology and Approach. 18 3.1 Previous valuation work and methodology changes . 18 3.2 Overview of current methodology . 18 3.3 Disease type and class subdivision . 20 3.4 Numbers of future claims notifications . 22 3.5 Incidence of claim settlements from future claim notifications. 27 3.6 Average claim costs of IBNR claims . 27 3.7 Proportion of claims settled for nil amounts . 28 3.8 Pending claims . 29 3.9 Insurance Recoveries. 30 3.10 Cross-claim recoveries . 34 3.11 Discounting cashflows . 35 4 Claims Experience: Mesothelioma Claim Numbers . 36 4.1 Overview . 36 4.2 Profile of mesothelioma claims . 39 4.3 External statistics on mesothelioma claims incidence. 44 4.4 Base valuation assumption for number of mesothelioma claims . 46 5 Claims Experience: Claim numbers (non-mesothelioma) . 47 5.1 Overview . 47 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

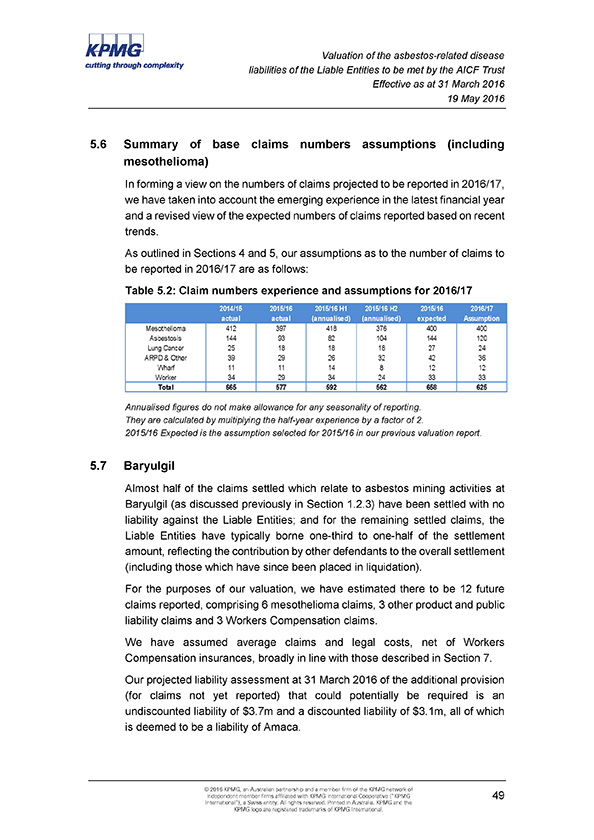

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 5.2 Asbestosis claims. 47 5.3 Lung cancer claims . 48 5.4 ARPD & Other claims . 48 5.5 Workers Compensation and Wharf claims. 48 5.6 Summary of base claims numbers assumptions (including mesothelioma). 49 5.7 Baryulgil . 49 6 Exposure and Latency Experience and Incidence Pattern Assumptions . 50 6.1 Exposure information. 50 6.2 Latency period of reported claims. 52 6.3 Modelled peak year of claims . 57 6.4 Pattern of future claim notifications assumed . 58 7 Claims Experience: Average Claims Costs and Average Legal Costs. 60 7.1 Overview . 60 7.2 Mesothelioma claims . 61 7.3 Asbestosis claims. 64 7.4 Lung cancer claims . 65 7.5 ARPD & Other claims . 66 7.6 Workers Compensation claims . 67 7.7 Wharf claims . 68 7.8 Mesothelioma large claim size and incidence rates . 69 7.9 Summary average claim cost assumptions. 71 7.10 Defence legal costs . 72 7.11 Summary average defendant legal costs assumptions . 74 8 Claims Experience: Nil Settlement Rates . 75 8.1 Overview . 75 8.2 Mesothelioma claims . 76 8.3 Asbestosis claims. 77 8.4 Lung cancer claims .. 78 8.5 ARPD & Other claims . 79 8.6 Workers Compensation claims . 80 8.7 Wharf claims . 81 8.8 Summary assumptions . 82 9 Economic and Other Assumptions . 83 9.1 Overview . 83 9.2 Claims inflation . 83 9.3 Superimposed inflation . 89 9.4 Discount rates: Commonwealth bond zero coupon yields. 92 9.5 Cross-claim recovery rates . 93 9.6 Settlement Patterns . 94 10 Valuation Results . 96 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 10.1 Central estimate liability. 96 10.2 Comparison with previous valuation . 97 10.3 Comparison of valuation results since 30 September 2006 . 99 10.4 Cashflow projections . 100 10.5 Amended Final Funding Agreement calculations. 102 10.6 Insurance Recoveries. 103 11 Uncertainty. 104 11.1 Overview . 104 11.2 Sensitivity testing. 105 11.3 Results of sensitivity testing. 107 Tables Table 2.1: Grouping of financial data from claims and accounting databases . 15 Table 2.2: Comparison of amounts from claims and accounting databases ($m). 16 Table 3.1: Change in cost of claims during 2015/16 financial year ($m) – claim award component only . 30 Table 5.1: Number of claims by disease type. 47 Table 5.2: Claim numbers experience and assumptions for 2016/17 . 49 Table 6.1: Assumed underlying latency distribution parameters from average date of exposure to date of notification . 56 Table 6.2: Modelled peak year of claim notifications . 57 Table 7.1: Average attritional non-nil claim award (inflated to mid 2015/16 money terms) . 60 Table 7.2: Average mesothelioma claims assumptions. 62 Table 7.3: Average asbestosis claims assumptions . 64 Table 7.4: Average lung cancer claims assumptions . 65 Table 7.5: Average ARPD & Other claims assumptions. 66 Table 7.6: Average Workers Compensation claims assumptions . 67 Table 7.7: Average wharf claims assumptions . 68 Table 7.8: Summary average claim cost assumptions . 71 Table 7.9: Summary average defendant legal costs assumptions. 74 Table 8.1: Nil settlement rates . 75 Table 8.2: Summary nil settlement rate assumptions . 82 Table 9.1: Base inflation assumptions. 89 Table 9.2: Settlement pattern of claims awards by delay from claim reporting . 95 Table 10.1: Comparison of central estimate of liabilities. 96 Table 10.2: Comparison of valuation results since 30 September 2006 . 99 Table 10.3: Amended Final Funding Agreement calculations. 102 Table 10.4: Insurance recoveries at 31 March 2016 . 103 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

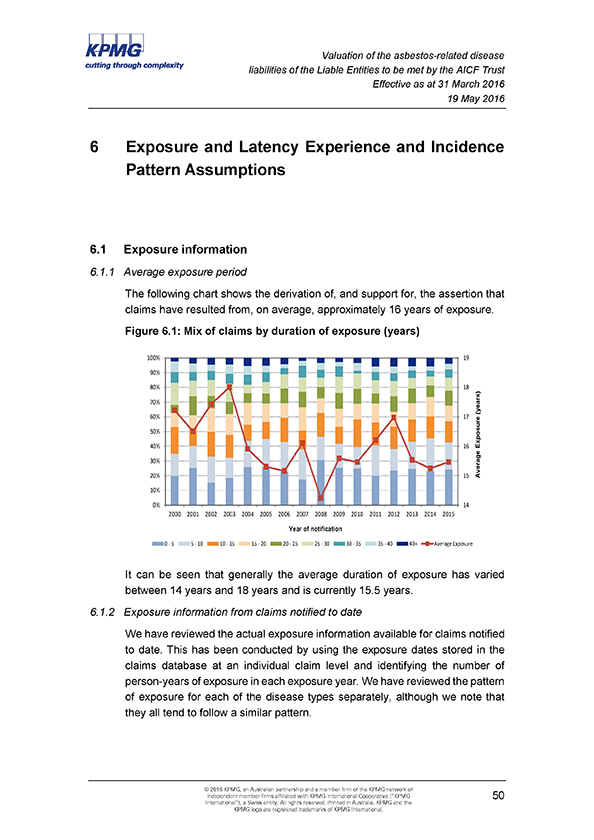

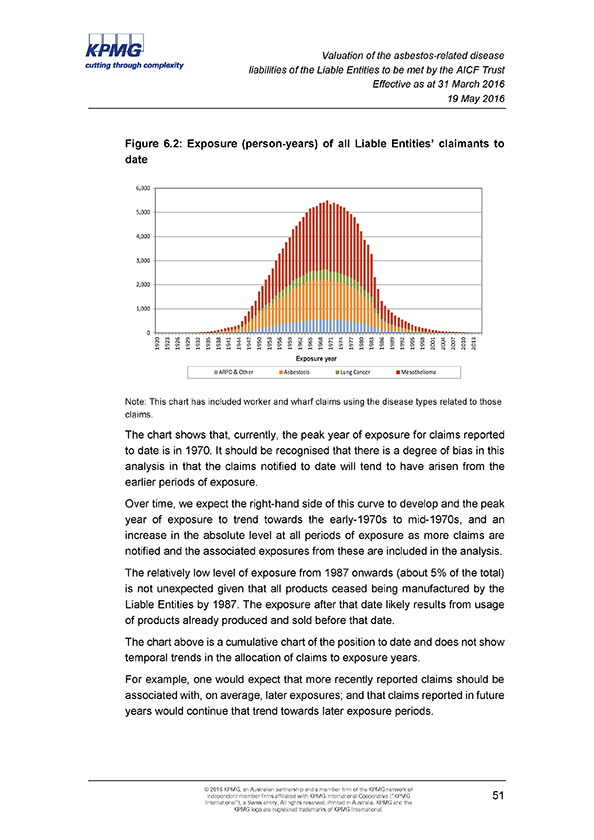

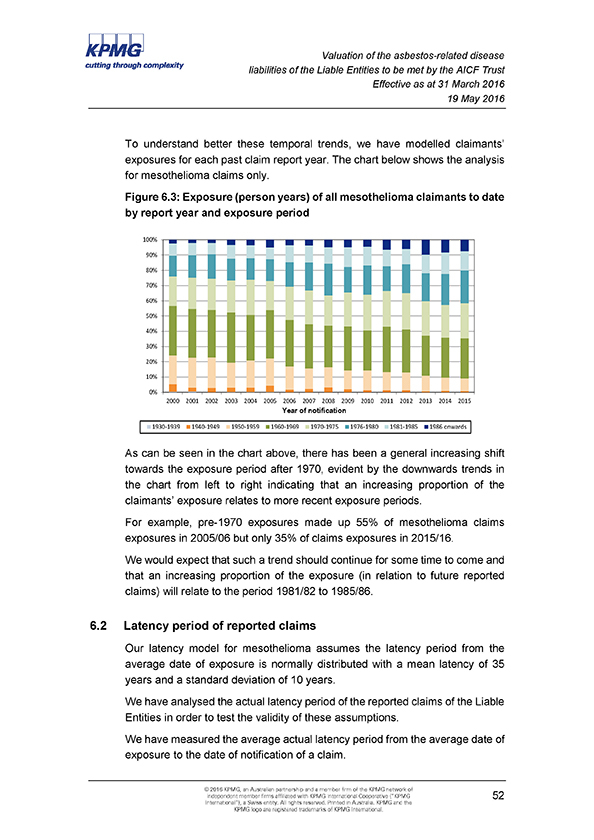

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Table 11.1: Summary results of sensitivity analysis ($m) . 108 Figures Figure 3.1: Illustration of timeline of exposure, latency and claim reporting (example shown is for mesothelioma) . 23 Figure 3.2: Consumption and production indices – Australia 1930-2002 . 24 Figure 4.1: Number of mesothelioma claims reported annually. 36 Figure 4.2: Monthly notifications of mesothelioma claims. 37 Figure 4.3: Rolling annualised averages of mesothelioma claim notifications . 38 Figure 4.4: Number of mesothelioma claims by State . 39 Figure 4.5: Number of mesothelioma claims by type of claim. 40 Figure 4.6: Number of mesothelioma claims by number of defendants (direct claims only) .41 Figure 4.7: Number of mesothelioma claims by age of claimant . 42 Figure 4.8: Delay from diagnosis of mesothelioma to notification of claim against the Liable Entities . 43 Figure 4.9: Number of mesothelioma cases reported nationally compared to the number of claims received by the Liable Entities . 44 Figure 4.10: Number of mesothelioma cases reported in NSW. 45 Figure 6.1: Mix of claims by duration of exposure (years) . 50 Figure 6.2: Exposure (person-years) of all Liable Entities’ claimants to date . 51 Figure 6.3: Exposure (person years) of all mesothelioma claimants to date by report year and exposure period . 52 Figure 6.4: Latency of mesothelioma claims . 53 Figure 6.5: Latency of asbestosis claims. 55 Figure 6.6: Latency of lung cancer claims . 55 Figure 6.7: Latency of ARPD & Other claims . 56 Figure 6.8: Projected future claim notifications for mesothelioma. 58 Figure 6.9: Projected future claim notifications for other disease types . 59 Figure 7.1: Average attritional awards (inflated to mid 2015/16 money terms) and number of non-nil claims settlements for mesothelioma claims (excluding large claims). 61 Figure 7.2: Average attritional awards (inflated to mid 2015/16 money terms) split between Direct claims and Cross claims. 62 Figure 7.3: Average attritional awards (inflated to mid 2015/16 money terms) by number of defendants for Direct claims. 63 Figure 7.4: Average awards (inflated to mid 2015/16 money terms) and number of non-nil claims settlements for asbestosis claims . 64 Figure 7.5: Average awards (inflated to mid 2015/16 money terms) and number of non-nil claims settlements for lung cancer claims . 65 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Figure 7.6: Average awards (inflated to mid 2015/16 money terms) and number of non-nil claims settlements for ARPD & Other claims. 66 Figure 7.7: Average awards (inflated to mid 2015/16 money terms) and number of non-nil claims settlements for Workers Compensation claims. 67 Figure 7.8: Average awards (inflated to mid 2015/16 money terms) and number of non-nil claims settlements for wharf claims . 68 Figure 7.9: Distribution of individual large claims by settlement year. 69 Figure 7.10: Number of mesothelioma large claims by year of notification . 70 Figure 7.11: Average defence legal costs (inflated to mid 2015/16 money terms) for non-nil claims settlements by settlement year . 72 Figure 7.12: Average defence legal costs (inflated to mid 2015/16 money terms) for nil claims settlements by settlement year . 73 Figure 8.1: Mesothelioma nil claims experience. 76 Figure 8.2: Asbestosis nil claims experience. 77 Figure 8.3: Lung cancer nil claims experience . 78 Figure 8.4: ARPD & Other nil claims experience. 79 Figure 8.5: Workers Compensation nil claims experience. 80 Figure 8.6: Wharf nil claims experience . 81 Figure 9.1: Trends in Bond Yields . 84 Figure 9.2: Trends in CPI and AWOTE . 85 Figure 9.3: Age profile of mesothelioma claimants by report year . 87 Figure 9.4: Average mesothelioma claim settlement amounts by decade of age (inflated to mid-2015/16 money terms) . 88 Figure 9.5: Average mesothelioma awards of the Liable Entities (uninflated). 91 Figure 9.6: Zero coupon yield curve by duration . 93 Figure 9.7: Cross-claim recovery experience . 93 Figure 9.8: Settlement pattern derivation for mesothelioma claims: paid as % of ultimate cost. 94 Figure 9.9: Settlement pattern derivation for non-mesothelioma claims: paid as % of ultimate cost . 94 Figure 10.1: Analysis of change in central estimate liability (discounted basis) . 98 Figure 10.2: Analysis of change in central estimate liability (undiscounted basis) . 98 Figure 10.3: Historical claim-related expenditure of the Liable Entities. 100 Figure 10.4: Annual cashflow projections – inflated and undiscounted ($m) . 101 Figure 11.1: Sensitivity testing results – Impact around the Discounted Central Estimate (in $m) . 107 Figure 11.2: Sensitivity testing results – Impact around the undiscounted central estimate (in $m) . 108 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

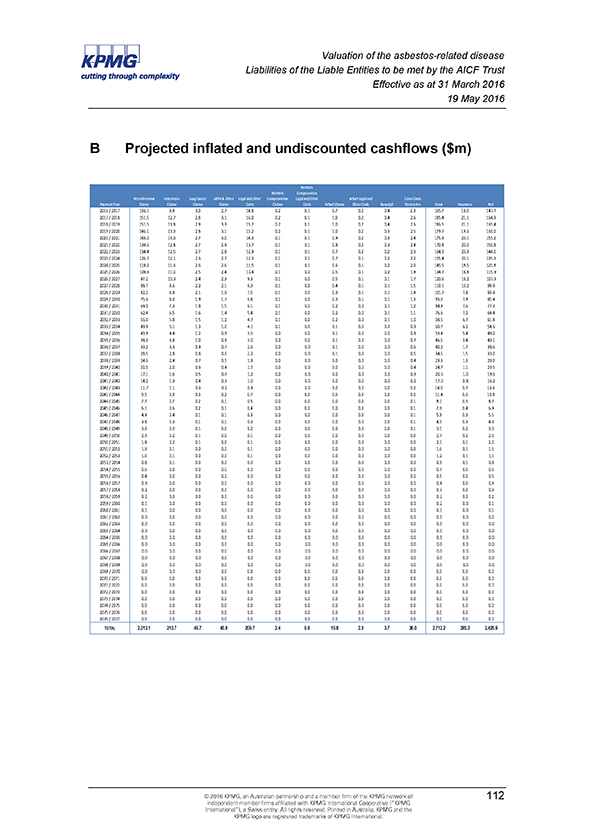

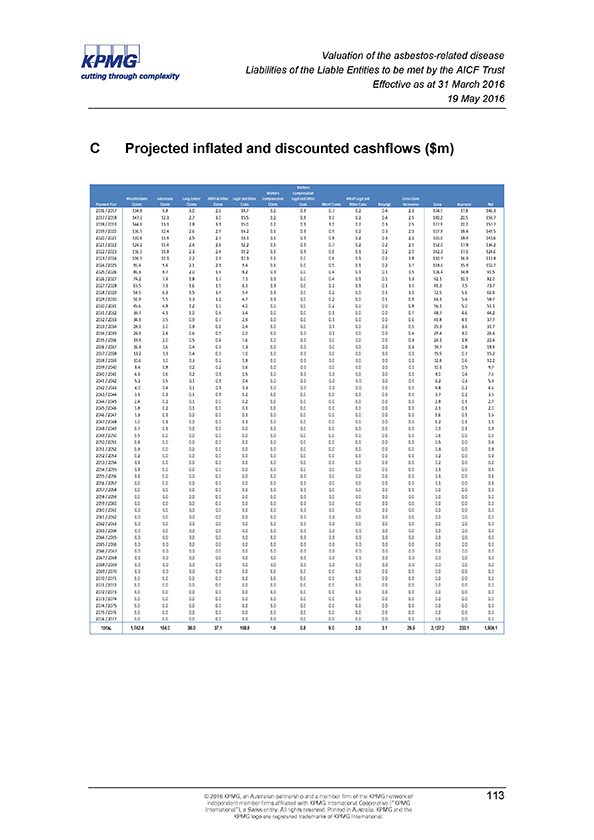

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Appendices APPENDICES. 110 A Credit rating default rates by duration. 111 B Projected inflated and undiscounted cashflows ($m) . 112 C Projected inflated and discounted cashflows ($m). 113 D Australian asbestos consumption and production data: 1930-2002 . 114 E Data provided by AICFL . 115 F Glossary of terms used in the Amended Final Funding Agreement . 117 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Executive Summary Important Note: Basis of Report This valuation report (“the Report”) has been prepared by KPMG Actuarial Pty Ltd (ABN 91 144 686 046) (“KPMG Actuarial”) in accordance with an “Amended and Restated Final Funding Agreement in respect of the provision of long-term funding for compensation arrangements for certain victims of Asbestos-related diseases in Australia” (hereafter referred to as the “the Amended Final Funding Agreement”) between James Hardie Industries NV (now known as James Hardie Industries plc) (hereafter referred to as “James Hardie”), James Hardie 117 Pty Limited, the State of New South Wales and Asbestos Injuries Compensation Fund Limited (“AICFL”) which was signed on 21 November 2006. This Report is intended to meet the requirements of the Amended Final Funding Agreement and values the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust. This Report is not intended to be used for any other purpose and may not be suitable, and should not be used, for any other purpose. Opinions and estimates contained in the Report constitute our judgment as of the date of the Report. The information contained in this Report is of a general nature and is not intended to address the objectives, financial situation or needs of any particular individual or entity. It is provided for information purposes only and does not constitute, nor should it be regarded in any manner whatsoever as, advice and is not intended to influence a person in making a decision in relation to any financial product or an interest in a financial product. No one should act on the information contained in this Report without obtaining appropriate professional advice after a thorough examination of the accuracy and appropriateness of the information contained in this Report having regard to their objectives, financial situation and needs. In preparing the Report, KPMG Actuarial has relied on information supplied to it from various sources and has assumed that the information is accurate and complete in all material respects. KPMG Actuarial has not independently verified the accuracy or completeness of the data and information used for this Report. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG i International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Except insofar as liability under statute cannot be excluded, KPMG Actuarial, its executives, directors, employees and agents will not be held liable for any loss or damage of any kind arising as a consequence of any use of the Report or purported reliance on the Report including any errors in, or omissions from, the valuation models. The Report must be read in its entirety. Individual sections of the Report, including the Executive Summary, could be misleading if considered in isolation. In particular, the opinions expressed in the Report are based on a number of assumptions and qualifications which are set out in the full Report. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG ii International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

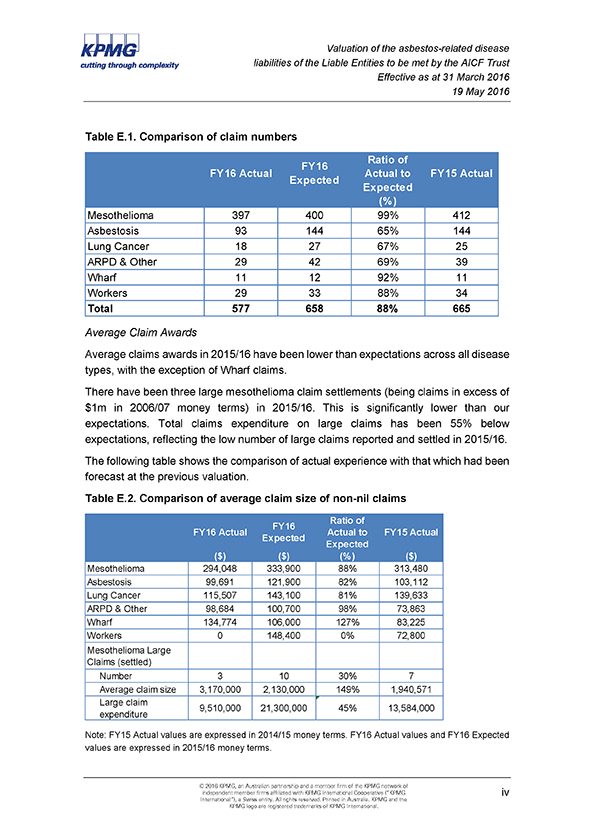

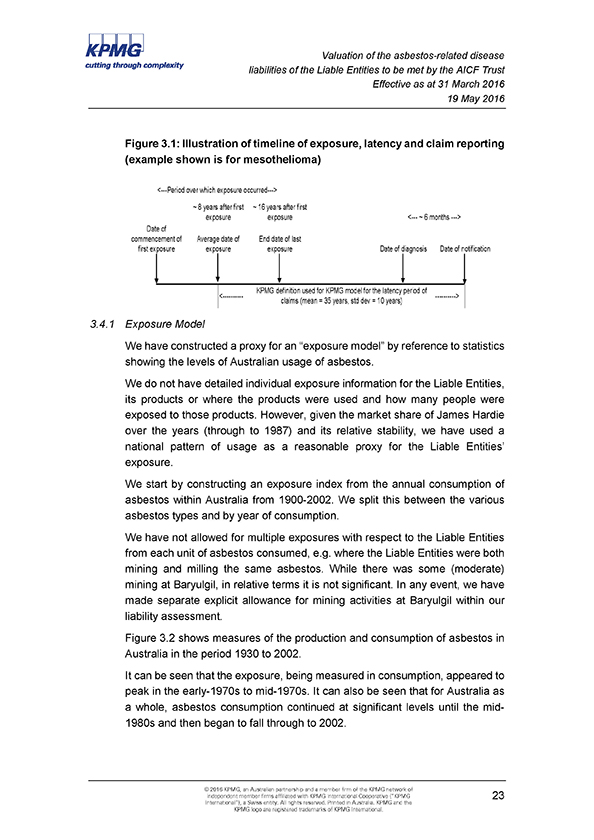

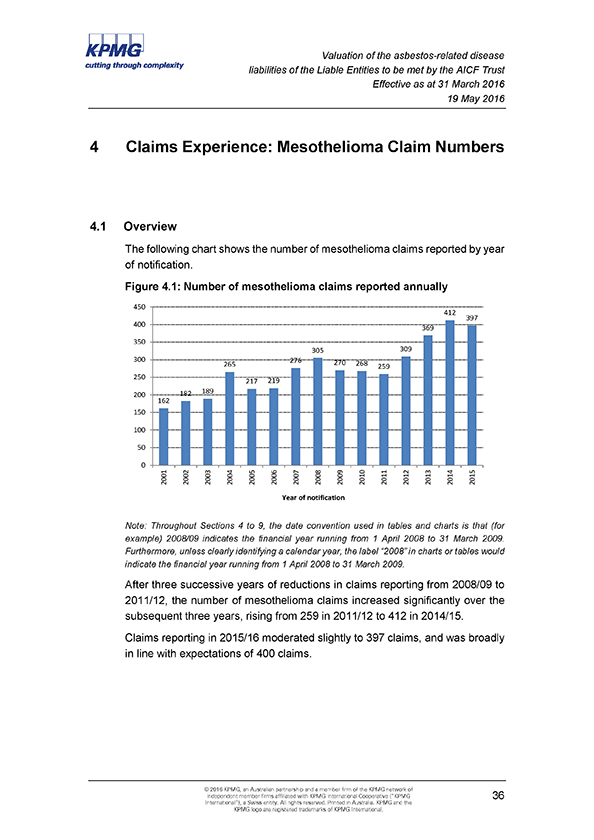

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Introduction The Amended Final Funding Agreement requires the completion of an Annual Actuarial Report evaluating the potential asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust. KPMG Actuarial has been retained by AICFL to provide this Annual Actuarial Report as required under the Amended Final Funding Agreement and this is detailed in our Engagement Letter dated 26 November 2015. The Liable Entities are defined as being the following entities: • Amaca Pty Ltd (formerly James Hardie & Coy); • Amaba Pty Ltd (formerly Jsekarb, James Hardie Brakes and Better Brakes); and • ABN60 Pty Ltd (formerly James Hardie Industries Ltd). In addition, the liability for Baryulgil claims is deemed to be a liability of Amaca by virtue of the James Hardie (Civil Liability) Act 2005 (NSW). Under Part 4 of that Act, Amaca is liable for the “Marlew Asbestos Claims” or “Marlew Contribution Claims” as defined in that Act. Our valuation is on a central estimate basis and is intended to be effective as at 31 March 2016. It has been based on claims data and information as at 31 March 2016 provided to us by AICFL. Overview of Recent Claims Experience and comparison with previous valuation projections In this section we compare the actual experience in 2015/16 (referred to in the following tables as “FY16 Actual”) with the projections for 2015/16 that were contained within our previous valuation report at 31 March 2015. We will refer to these projections for 2015/16 as “FY16 Expected” in the tables that follow. Claim numbers There have been 397 mesothelioma claims reported in 2015/16, a 4% decrease compared to the 412 mesothelioma claims reported in 2014/15. For non-mesothelioma claims (excluding workers compensation claims), there have been 151 claims reported in 2015/16 compared to 219 claims reported in 2014/15. The following table shows the comparison of actual experience with that which had been forecast at the previous valuation. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG iii International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Table E.1. Comparison of claim numbers Ratio of FY16 FY16 Actual Actual to FY15 Actual Expected Expected (%) Mesothelioma 397 400 99% 412 Asbestosis 93 144 65% 144 Lung Cancer 18 27 67% 25 ARPD & Other 29 42 69% 39 Wharf 11 12 92% 11 Workers 29 33 88% 34 Total 577 658 88% 665 Average Claim Awards Average claims awards in 2015/16 have been lower than expectations across all disease types, with the exception of Wharf claims. There have been three large mesothelioma claim settlements (being claims in excess of $1m in 2006/07 money terms) in 2015/16. This is significantly lower than our expectations. Total claims expenditure on large claims has been 55% below expectations, reflecting the low number of large claims reported and settled in 2015/16. The following table shows the comparison of actual experience with that which had been forecast at the previous valuation. Table E.2. Comparison of average claim size of non-nil claims Ratio of FY16 FY16 Actual Actual to FY15 Actual Expected Expected ($) ($) (%) ($) Mesothelioma 294,048 333,900 88% 313,480 Asbestosis 99,691 121,900 82% 103,112 Lung Cancer 115,507 143,100 81% 139,633 ARPD & Other 98,684 100,700 98% 73,863 Wharf 134,774 106,000 127% 83,225 Workers 0 148,400 0% 72,800 Mesothelioma Large Claims (settled) Number 3 10 30% 7 Average claim size 3,170,000 2,130,000 149% 1,940,571 Large claim 9,510,000 21,300,000 45% 13,584,000 expenditure Note: FY15 Actual values are expressed in 2014/15 money terms. FY16 Actual values and FY16 Expected values are expressed in 2015/16 money terms. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG iv International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

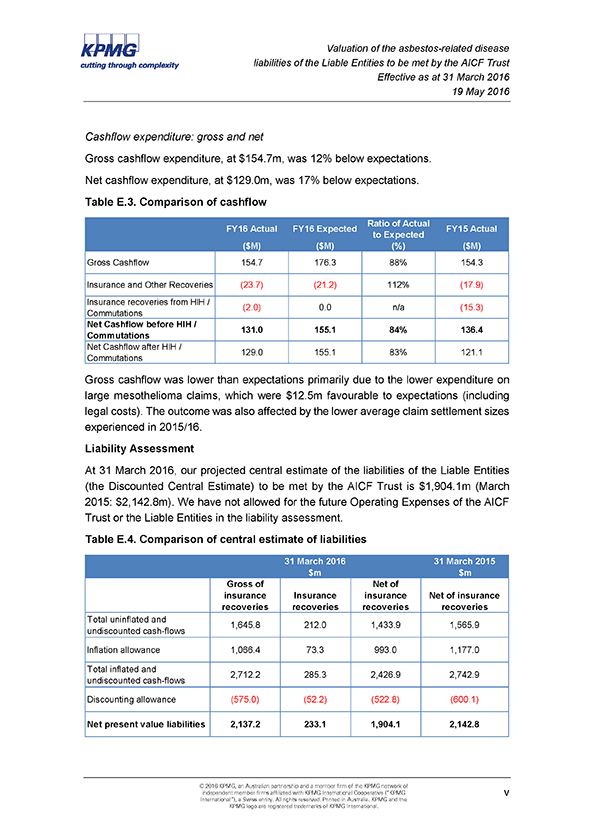

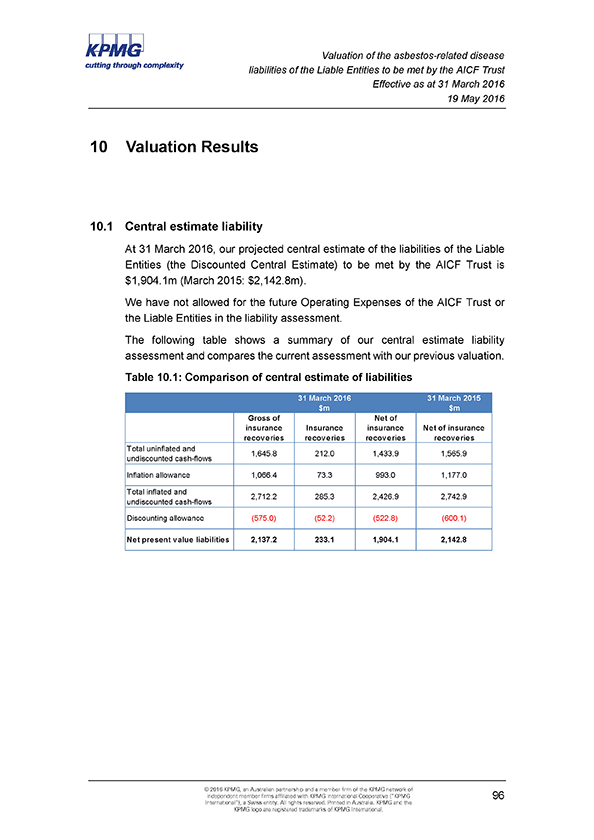

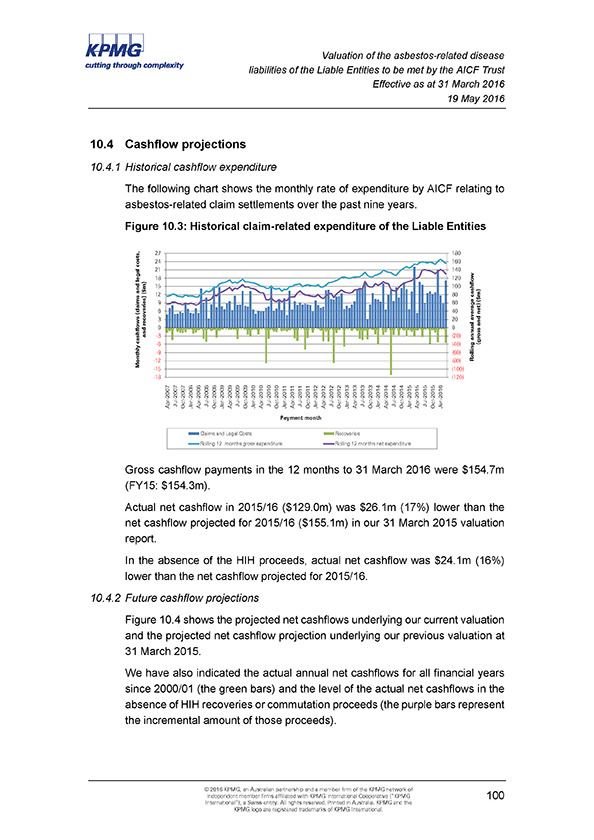

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Cashflow expenditure: gross and net Gross cashflow expenditure, at $154.7m, was 12% below expectations. Net cashflow expenditure, at $129.0m, was 17% below expectations. Table E.3. Comparison of cashflow Ratio of Actual FY16 Actual FY16 Expected FY15 Actual to Expected ($M) ($M) (%) ($M) Gross Cashflow 154.7 176.3 88% 154.3 Insurance and Other Recoveries (23.7) (21.2) 112% (17.9) Insurance recoveries from HIH / (2.0) 0.0 n/a (15.3) Commutations Net Cashflow before HIH / 131.0 155.1 84% 136.4 Commutations Net Cashflow after HIH / 129.0 155.1 83% 121.1 Commutations Gross cashflow was lower than expectations primarily due to the lower expenditure on large mesothelioma claims, which were $12.5m favourable to expectations (including legal costs). The outcome was also affected by the lower average claim settlement sizes experienced in 2015/16. Liability Assessment At 31 March 2016, our projected central estimate of the liabilities of the Liable Entities (the Discounted Central Estimate) to be met by the AICF Trust is $1,904.1m (March 2015: $2,142.8m). We have not allowed for the future Operating Expenses of the AICF Trust or the Liable Entities in the liability assessment. Table E.4. Comparison of central estimate of liabilities 31 March 2016 31 March 2015 $m $m Gross of Net of insurance Insurance insurance Net of insurance recoveries recoveries recoveries recoveries Total uninflated and 1,645.8 212.0 1,433.9 1,565.9 undiscounted cash-flows Inflation allowance 1,066.4 73.3 993.0 1,177.0 Total inflated and 2,712.2 285.3 2,426.9 2,742.9 undiscounted cash-flows Discounting allowance (575.0) (52.2) (522.8) (600.1) Net present value liabilities 2,137.2 233.1 1,904.1 2,142.8 © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG v International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

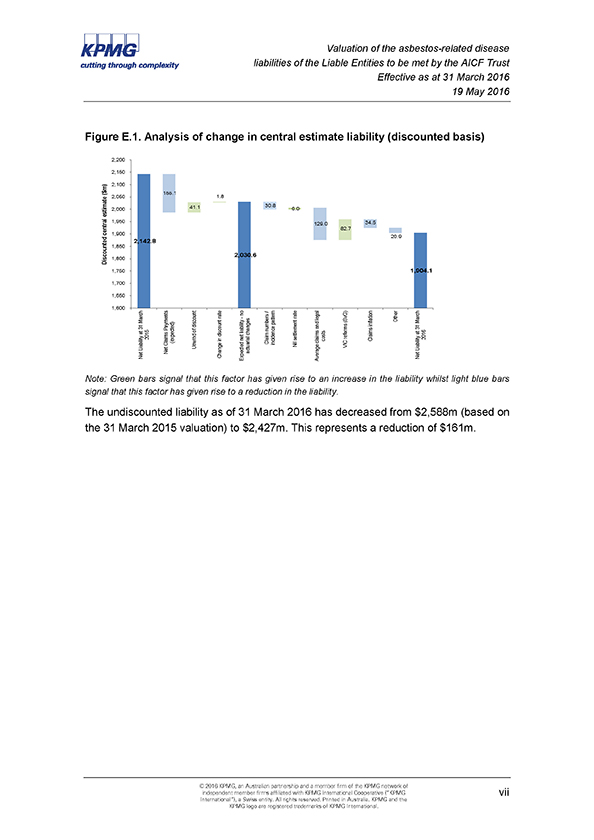

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Comparison with previous valuation In the absence of any change to the claim projection assumptions from our 31 March 2015 valuation, other than allowing for the changes in the discount rate, we would have projected a Discounted Central Estimate liability of $2,030.6m as at 31 March 2016, i.e. a reduction of $112.2m from our 31 March 2015 valuation result. This decrease of $112.2m is due to: • A reduction of $114.0m, being the net impact of expected claims payments (which reduce the liability) and the “unwind of discount” (which increases the liability and reflects the fact that cashflows are now one year nearer and therefore are discounted by one year less). • An increase of $1.8m resulting from changes to the yield curve between 31 March 2015 and 31 March 2016. Our liability assessment at 31 March 2016 of $1,904.1m represents a decrease of $126.5m, which arises from changes to the actuarial assumptions. The decrease of $126.5m is principally a consequence of: • Lower average claim sizes and defence legal cost assumptions across most disease types; • A reduction in the assumed number of large mesothelioma claims; • A reduction in the projected number of non-mesothelioma claims; • Lower claims inflation assumptions in the short-term (through to, and including, 2019/20); and • Favourable experience for claims that were pending at 31 March 2015. offset by • An allowance for the potential costs of Sullivan vs Gordon awards due to the amendments to the Wrongs Act in the State of Victoria. The following chart shows an analysis of the change in our liability assessments from 31 March 2015 to 31 March 2016 on a discounted basis. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG vi International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

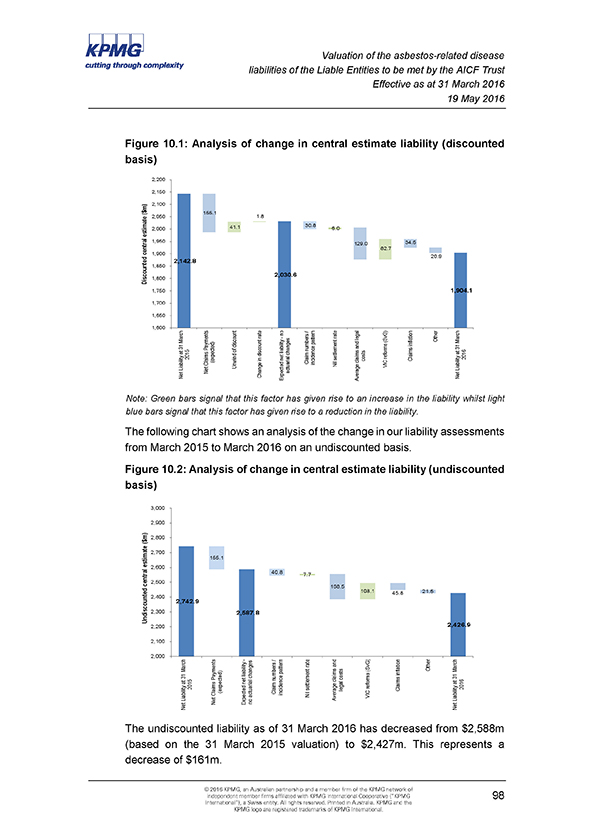

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Figure E.1. Analysis of change in central estimate liability (discounted basis) 2,200 2,150 2,100 $ m) 155.1 ( 2,050 1.8 41.1 30.8 estimate 2,000 6.0 1,950 129.0 34.5 central 82.7 1,900 20.9 1,850 2,142.8 2,030.6 Discounted 1,800 1,750 1,904.1 1,700 1,650 1,600 no/ rate—rate March legal (SvG) Other March pattern discount inflation 31 Payments and 31 of numbers at liability changes at 2015discount reforms 2016 in net settlement costs Claims (expected) Claim claims Claims incidence Liability Unwind Nil VIC Liability Net Net Change Expectedactuarial Average Net Note: Green bars signal that this factor has given rise to an increase in the liability whilst light blue bars signal that this factor has given rise to a reduction in the liability. The undiscounted liability as of 31 March 2016 has decreased from $2,588m (based on the 31 March 2015 valuation) to $2,427m. This represents a reduction of $161m. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG vii International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

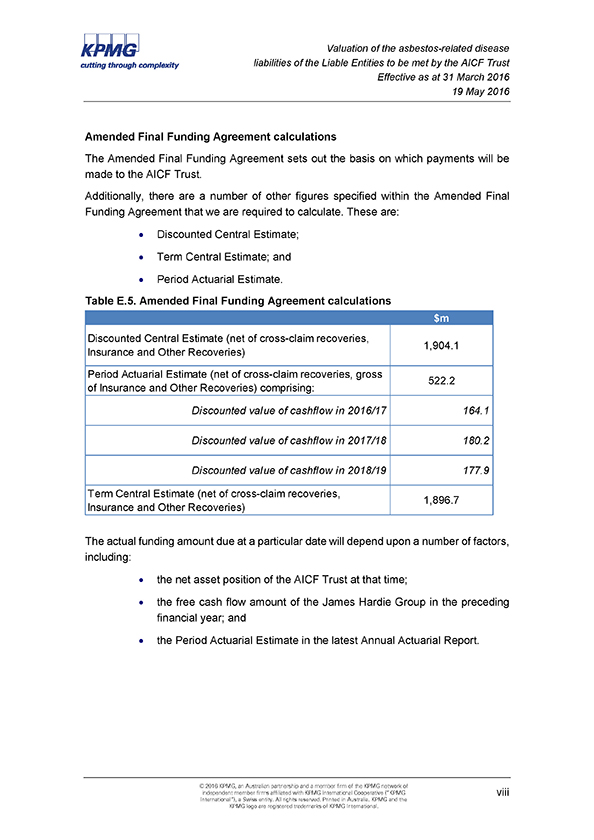

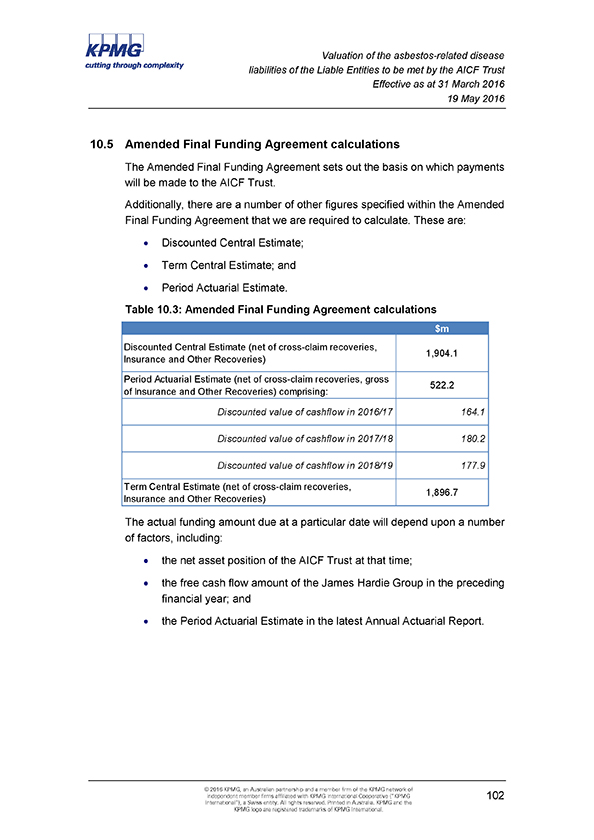

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Amended Final Funding Agreement calculations The Amended Final Funding Agreement sets out the basis on which payments will be made to the AICF Trust. Additionally, there are a number of other figures specified within the Amended Final Funding Agreement that we are required to calculate. These are: • Discounted Central Estimate; • Term Central Estimate; and • Period Actuarial Estimate. Table E.5. Amended Final Funding Agreement calculations $m Discounted Central Estimate (net of cross-claim recoveries, 1,904.1 Insurance and Other Recoveries) Period Actuarial Estimate (net of cross-claim recoveries, gross 522.2 of Insurance and Other Recoveries) comprising: Discounted value of cashflow in 2016/17 164.1 Discounted value of cashflow in 2017/18 180.2 Discounted value of cashflow in 2018/19 177.9 Term Central Estimate (net of cross-claim recoveries, 1,896.7 Insurance and Other Recoveries) The actual funding amount due at a particular date will depend upon a number of factors, including: • the net asset position of the AICF Trust at that time; • the free cash flow amount of the James Hardie Group in the preceding financial year; and • the Period Actuarial Estimate in the latest Annual Actuarial Report. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG viii International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

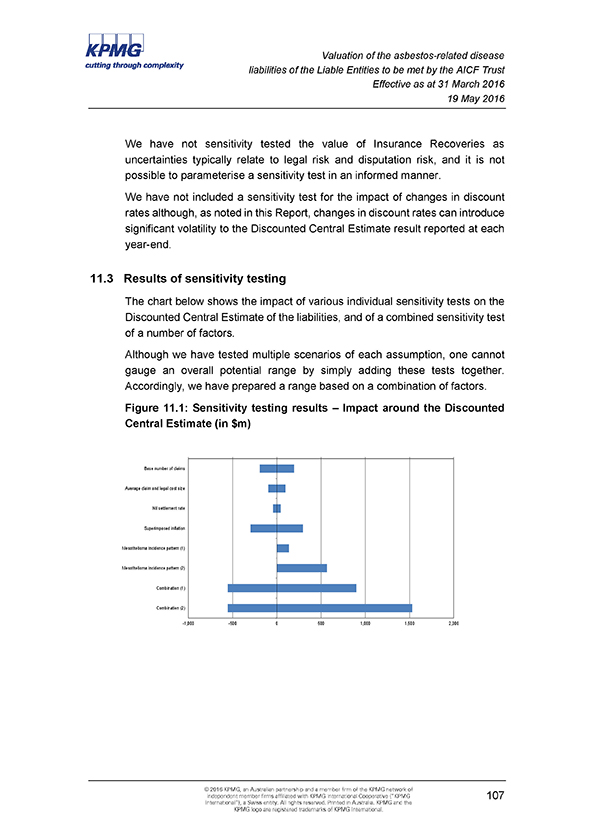

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Uncertainty Estimates of asbestos-related disease liabilities are subject to considerable uncertainty, significantly more than personal injury liabilities in relation to other causes, such as CTP or Workers Compensation claims. It should therefore be expected that the actual emergence of the liabilities will vary from any estimate. As indicated in Figure E.3, depending on the actual out-turn of experience relative to that currently forecast, the variation could potentially be substantial. Thus, no assurance can be given that the actual liabilities of the Liable Entities to be met by the AICF Trust will not ultimately exceed the estimates contained in this Report. Any such variation may be significant. We have performed sensitivity testing to identify the impact of different assumptions upon the size of the liabilities. The different scenarios selected are documented at Section 11.2 of this report. We have not included a sensitivity test for the impact of changes in discount rates although, as noted in this Report, changes in discount rates can introduce significant volatility to the Discounted Central Estimate result reported at each year-end. We note that these sensitivity test ranges are not intended to correspond to a specified probability of sufficiency, nor are they intended to indicate an upper bound or a lower bound of all possible outcomes. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG ix International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

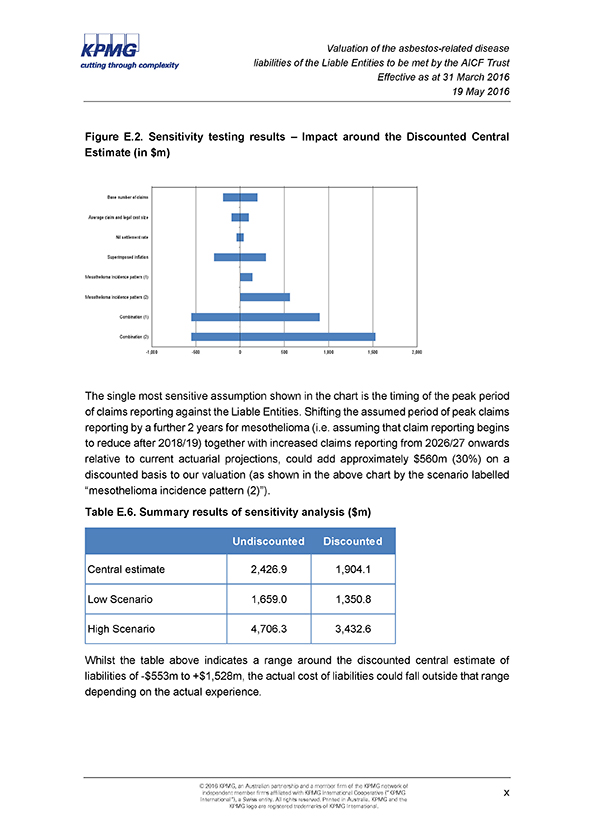

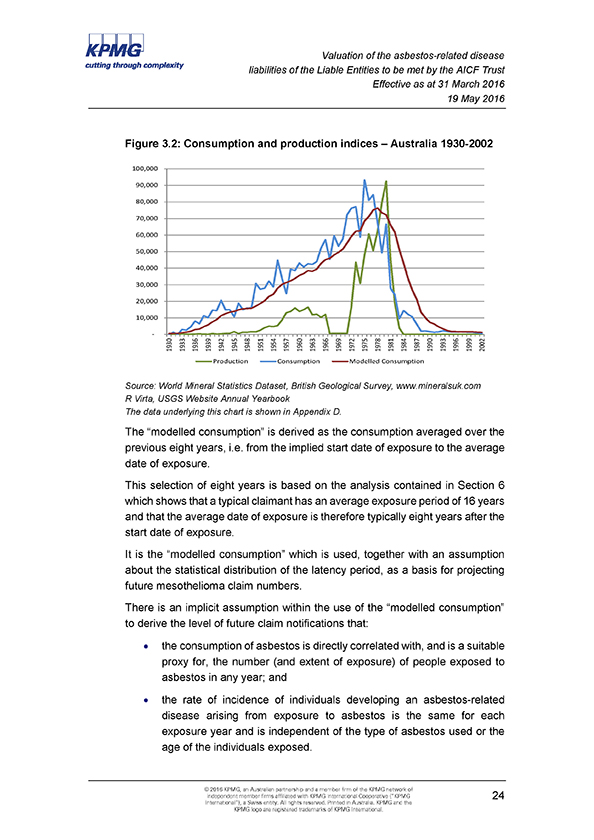

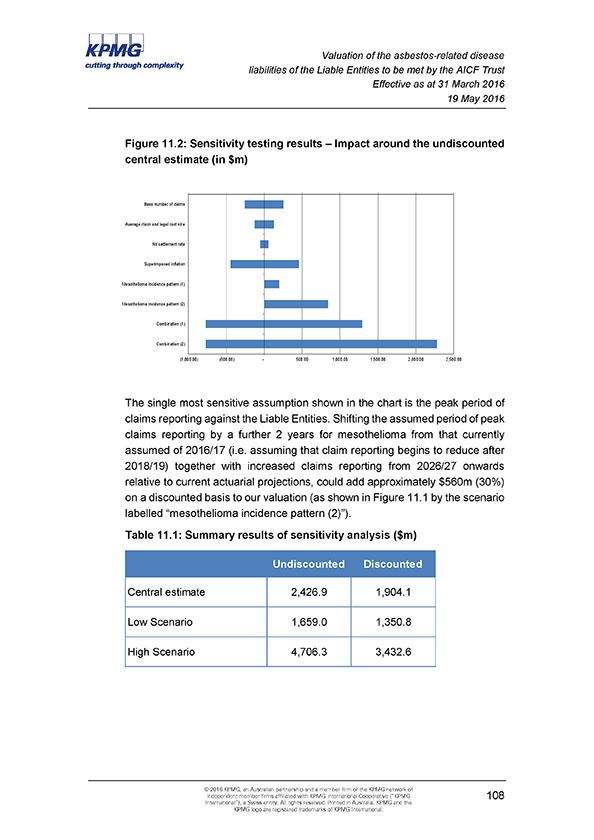

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Figure E.2. Sensitivity testing results – Impact around the Discounted Central Estimate (in $m) Base number of claims Average claim and legal cost size Nil settlement rate Superimposed inflation Mesothelioma incidence pattern (1) Mesothelioma incidence pattern (2) Combination (1) Combination (2) -1,000 -500 0 500 1,000 1,500 2,000 The single most sensitive assumption shown in the chart is the timing of the peak period of claims reporting against the Liable Entities. Shifting the assumed period of peak claims reporting by a further 2 years for mesothelioma (i.e. assuming that claim reporting begins to reduce after 2018/19) together with increased claims reporting from 2026/27 onwards relative to current actuarial projections, could add approximately $560m (30%) on a discounted basis to our valuation (as shown in the above chart by the scenario labelled “mesothelioma incidence pattern (2)”). Table E.6. Summary results of sensitivity analysis ($m) Undiscounted Discounted Central estimate 2,426.9 1,904.1 Low Scenario 1,659.0 1,350.8 High Scenario 4,706.3 3,432.6 Whilst the table above indicates a range around the discounted central estimate of liabilities of -$553m to +$1,528m, the actual cost of liabilities could fall outside that range depending on the actual experience. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG x International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

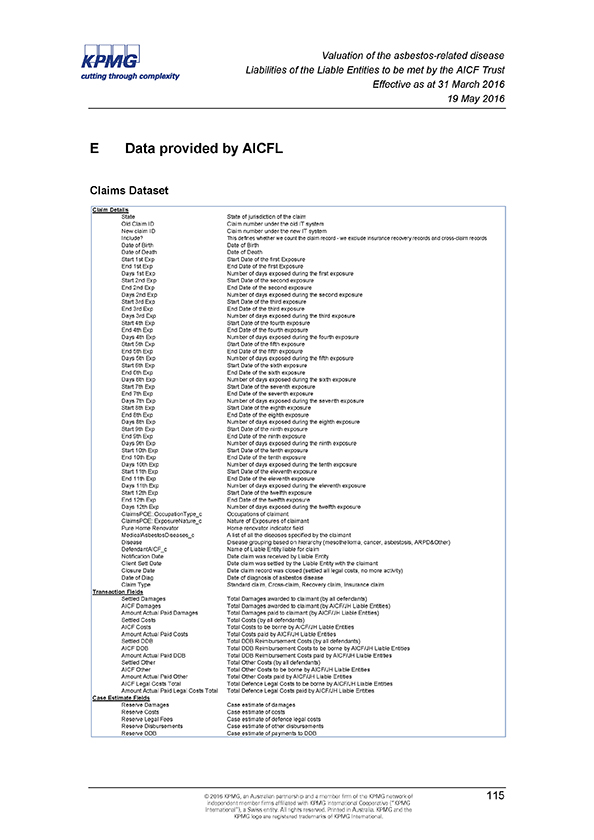

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Data, Reliances and Limitations We have been provided with the following data by AICFL: • Claims dataset at 31 March 2016 with individual claims listings; • Accounting transactions dataset at 31 March 2016 (which includes individual claims payment details); and • Detailed insurance bordereaux information (being a listing of claims filed with the insurers of the Liable Entities) produced by Randall & Quilter Investment Holdings as at 31 March 2016. While we have tested the consistency of the various data sets provided, we have not otherwise verified the data nor have we undertaken any auditing of the data at source. We have relied on the data provided as being complete and accurate in all material respects. Consequently, should there be material errors or incompleteness in the data, our assessment could be affected materially. Executive Summary Not Report Please note that this executive summary is intended as a brief overview of our Report. To properly understand our analysis and the basis of our liability assessment requires examination of our Report in full. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG xi International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 1 Scope and Purpose 1 1.1 Introduction The Amended Final Funding Agreement requires the completion of an Annual Actuarial Report evaluating the potential asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust. 1.1.1 Liable Entities The Liable Entities are defined as being the following entities: • Amaca Pty Ltd (formerly James Hardie & Coy); • Amaba Pty Ltd (formerly Jsekarb, James Hardie Brakes and Better Brakes); and • ABN60 Pty Ltd (formerly James Hardie Industries Ltd). In addition, the liability for Baryulgil claims is deemed to be a liability of Amaca by virtue of the James Hardie (Civil Liability) Act 2005 (NSW). Under Part 4 of that Act, Amaca is liable for “Marlew Asbestos Claims” or “Marlew Contribution Claims” as defined in that Act. 1.1.2 Personal asbestos claims Under the Amended Final Funding Agreement, the liabilities to be met by the AICF Trust relate to personal asbestos-related disease liabilities of the Liable Entities. Such claims must relate to exposure which took place in Australia and which have been brought in a Court in Australia. The precise scope of the liabilities is documented in Section 1.2 and in Appendix F of this Report. 1.1.3 Purpose of report KPMG Actuarial has been retained by AICFL to provide an Annual Actuarial Report as required under the Amended Final Funding Agreement and this is detailed in our Engagement Letter dated 26 November 2015. The prior written consent of KPMG Actuarial is required for any other use of this Report or the information contained in it. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 1 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Our valuation is effective as at 31 March 2016 and has been based on claims data and information as at 31 March 2016 provided to us by AICFL. 1.2 Scope of report We have been requested to provide an actuarial assessment as at 31 March 2016 of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust, consistent with the terms of the Amended Final Funding Agreement. The assessment is on a central estimate basis and is based on the claims experience as at 31 March 2016. A “central estimate” liability assessment is an estimate of the expected value of the range of potential future liability outcomes. In other words, if all the possible values of the liabilities are expressed as a statistical distribution, the central estimate is an estimate of the mean of that distribution. It is of note that our liability assessment: • Relates to the Liable Entities and Marlew (in relation to Marlew Claims arising from asbestos mining activities at Baryulgil). • Is intended to cover:—The amount of settlements, judgments or awards for all Personal Asbestos Claims.—Claims Legal Costs incurred by the AICF Trust in connection with the settlement of Personal Asbestos Claims. • Is not intended to cover:—Personal injury or death claims arising from exposure to asbestos which took place outside Australia.—Personal injury or death claims, arising from exposure to Asbestos, which are brought in Courts outside Australia.—Claims for economic loss, other than any economic loss forming part of an award for damages for personal injury and/or death.—Claims for loss of property, including those relating to land remediation.—The costs of asbestos or asbestos product removal relating to asbestos or asbestos products manufactured or used by or on behalf of the Liable Entities. • Includes an allowance for: © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 2 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 - Compensation to the NSW Dust Diseases Board or a Workers Compensation Scheme by way of a claim by such parties for contribution or reimbursement from the Liable Entities, but only to the extent that the cost of such claims is within the limits of funding for such claims as outlined within the Amended Final Funding Agreement.—Workers Compensation claims, being claims from former employees of the Liable Entities, but only to the extent that such liabilities are not met by a Workers Compensation Scheme or Policy (see section 1.2.1). • Assumes that the product and public liability insurance policies of the Liable Entities will continue to respond to claims as and when they fall due. We have not made any allowance for the impact of any disputation concerning Insurance Recoveries, nor for any legal costs that may be incurred in resolving such disputes. • Makes no allowance for:—potential Insurance Recoveries that could be made on product and public liability insurance policies placed from 1986 onwards which were placed on a “claims made” basis.—the future Operating Expenses of the Liable Entities or the AICF Trust. Separate allowance for future Operating Expenses should be considered by the management of AICFL.—the inherent uncertainty of the liability assessment. That is, no additional provision (or risk margin) has been included in excess of a central estimate. Readers of this Report may refer to our previous reports which are available at www.ir.jameshardie.com.au and www.aicf.org.au. 1.2.1 Workers Compensation Workers Compensation claims are claims made by former employees of the Liable Entities. Such past, current and future reported claims were insured with, amongst others, Allianz Australia Limited, QBE and the various State-based Workers Compensation Schemes. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 3 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Under the Amended Final Funding Agreement, the part of a future Workers Compensation claim that is met by a Workers Compensation Scheme or Policy of the Liable Entities is outside of the AICF Trust. The AICF Trust is, however, to provide for any part of a claim not covered by a Workers Compensation Scheme or Policy (e.g. as a result of the existence of limits of indemnity and policy deductibles on those policies of insurance). On this basis our liability assessment in relation to Workers Compensation claims and which relates to the AICF Trust, includes only the amount borne by the Liable Entities in excess of the anticipated recoveries due from a Workers Compensation Scheme or Policy. In making our assessment we have assumed that the Workers Compensation insurance programme will continue to respond to claims by former employees of the Liable Entities as and when they fall due. To the extent that they were not to respond owing to (say) insurer insolvency, Insurer Guarantee Funds may be available to meet such obligations. 1.2.2 Dust Disease Board and Other Reimbursements There exists a right under Section 8E (Reimbursement Provisions) of the Dust Diseases Act 1942 for the NSW Dust Diseases Board (“DDB”) to recover certain costs from common law defendants, excluding the employer of the claimant. This component of cost is implicitly included within our liability assessment as the claims awards made in recent periods and in recent settlements contain allowance for DDB reimbursement where applicable. Furthermore, currently reported open claims have an allowance within their case estimates for the costs of DDB reimbursement where relevant and applicable. The Amended Final Funding Agreement indicates that the AICF Trust is intended to meet Personal Asbestos Claims and that claims by the DDB or a Workers Compensation Scheme for reimbursement will only be met up to a certain specified limit (aggregated across the DDB and Workers Compensation Schemes), being: • In the first financial year (2006/07) a limit of $750,000 applied; • In respect of each financial year thereafter, that limit is indexed annually in line with the Consumer Price Index. At 31 March 2016, the annual limit is $954,936; • There is an overall unindexed aggregate cap of $30m; • At 31 March 2016, AICF has paid out $7,603,015 to the DDB. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 4 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 The cashflow and liability figures contained within this Report have already removed that component of any reimbursements that will not be met by the AICF Trust owing to the application of these limits and caps. 1.2.3 Baryulgil (“Marlew Claims”) “Marlew Asbestos Claims” and “Marlew Contribution Claims” are deemed to be liabilities of Amaca. These claims specifically include: • Claims made against Amaca Pty Ltd or ABN60 resulting from their past ownership of the mine; and, in the case of Amaca, includes claims made in relation to the joint venture (Asbestos Mines Pty Ltd) established with Wunderlich in 1944 to begin mining at Baryulgil. • Claims made against the subsequent owner of the mine (following its sale by James Hardie Industries to Woodsreef in 1976), being Marlew Mining Pty Ltd (“Marlew”) which is in liquidation, are to be met by the AICF Trust except where such claims are Excluded Marlew Claims, which are recoverable by the Claimant from other sources. These claims are discussed further in Section 5.7. 1.2.4 Risk Margins Australian-licensed insurance companies are required to hold, and many non-insurance companies elect to hold, insurance and self-insurance claims provisions at a level above the central estimate basis to reflect the uncertainty attaching to the liability assessment and to include an allowance in respect of that uncertainty. A risk margin is an additional amount held, above the central estimate, so as to increase the likelihood of adequacy of the provisions to meet the ultimate cost of settlement of those liabilities. We note that the Amended Final Funding Agreement envisages the ongoing financing of the AICF Trust is to be based on a “central estimate” approach and that the Annual Actuarial Report should provide a Discounted Central Estimate valuation. Accordingly, we have made no allowance for any risk margins within this Report. 1.2.5 Discounting We have determined a Discounted Central Estimate in this Report by discounting (to 31 March 2016) the projected future cashflows using yields on Commonwealth Government Bonds. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 5 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Conceptually, the Discounted Central Estimate at 31 March 2016 would normally represent an amount of money which, if fully provided in advance (i.e. as of 31 March 2016) and invested in risk-free assets (such as Commonwealth Government Bonds) of term and currency appropriate to the liabilities, would generate the necessary investment income such that (together with the capital value of those assets) it would be expected to be sufficient to pay for the liabilities as they fall due. To the extent that the actual investments are: • of different terms; and/or • in different currencies; and/or • provide different expected rates of return investment profits or losses would emerge. One of the uncertainties in our valuation is the fact that fixed interest Commonwealth Government Bonds do not exist at most of the durations of our cashflow projection. This means we need to take a long-term view on bond yields that is not measured by market-observable rates of return. We continue to note that the actual funding mechanism under the Amended Final Funding Agreement only provides for up to three years’ worth of projected Claims and Claims Legal Costs expenditure and one year’s worth of Operating Expenses at any one time. 1.3 Areas of potential exposure As identified in Section 1.2, there are other potential sources of claims exposure beyond those directly considered within this Report. However, in a number of cases they are unquantifiable even if they have the potential to generate claims. This is especially the case for those sources of future claim where there has been no evidence of claims to date. 1.3.1 General areas of potential exposure Areas of potential changes in claims exposure we have not explicitly allowed for in our valuation include, but are not limited to: • Future significant individual landmark and precedent-setting judicial decisions; • Significant medical advancements; © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 6 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 • Unimpaired claims, i.e. claims for fear, stress, pure nervous shock or psychological illness. In this regard, we note the 2010/11 decisions by the Supreme Court (in relation to two cases: Tamaresis v Amaca and Galea v Amaca) which indicated that the AICF Trust was not required to meet the cost of nervous shock claims brought by individuals who have not been exposed to asbestos; • A change in the basis of compensation for asymptomatic pleural plaques for which no associated physical impairment is exhibited; • A proliferation (compared to past and current levels of activity) of “third-wave” claims, i.e. claims arising as a result of indirect exposure such as home renovation, washing clothes of family members that worked with asbestos, or from workers involved in the removal of asbestos or the demolition of buildings containing asbestos; • Changes in legislation, especially those relating to tort reform for asbestos sufferers. Examples include the amendments under the Wrongs Act in Victoria (as noted in Section 1.3.3 of this Report) and the current consultation by the Law Reform Commission in Western Australia in relation to damages for gratuitous services and provisional damages; • Introduction of new, or elimination of existing, heads of damage; • Exemplary and aggravated or punitive damages (being damages awarded for personal injuries caused as a result of negligence or reckless conduct); • Changes in the basis of apportionment of awards for asbestos-related diseases for claimants who have smoked (we note the decisions in Amaca v Ellis [2010] HCA 5 and Evans v Queanbeyan City Council [2010] NSWDDT 7 which we understand are consistent with the previous decision in Judd v Amaca [2002] NSWDDT 25); • Changes to taxation; and • Future bankruptcies of other asbestos claim defendants (i.e. other liable manufacturers or distributors). Nonetheless, implicit allowance is made in respect of some of these items in the allowance for superimposed inflation included in our liability assessment. Furthermore, to the extent that some of these have emerged in past claims experience, they are reflected in our projections. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 7 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 1.3.2 New Zealand and other overseas exposures We have made no allowance for the risk of further development in relation to New Zealand exposures and the rights of claims from New Zealand claimants in Australian courts (as per Frost vs. Amaca Pty Ltd (2005), NSWDDT 36 although this decision was successfully appealed by Amaca in August 2006) nor for the risk of additional exposures from overseas. This is because, as noted in Section 1.2, the AICF Trust is not required to meet the cost of these claims as they are Excluded Claims. In relation to claimants where exposures have involved more than one country (e.g. UK and Australia), we have assumed that the AICF Trust will only meet that part of the cost which is attributable to the Australian-related exposure. 1.3.3 Victorian amendments to the Wrongs Act In 2015, the State of Victoria implemented amendments to the Wrongs Act (the Wrongs Amendment Act 2015) to incorporate the payment of Sullivan vs Gordon awards. These amendments came into force on 19 November 2015. The Department of Justice and Regulation of Victoria has recently advised AICF that it is making amendments to the current Regulations that apply to Dust Diseases, namely the Wrongs (Part VB) (Dust and Tobacco-Related Claims) Regulations 2006. We are advised that the effect of the various amendments is that from 10 May 2016, the AICF Trust will be required to pay for Sullivan vs Gordon awards (to the extent applicable) in relation to claims brought against the Liable Entities in Victoria. Such awards would then constitute Payable Liabilities under the Amended Final Funding Agreement. Therefore, we have made allowance for these awards in our valuation. We have allowed for such amounts over all future years over which claims are projected to emerge and settle. 1.3.4 Third-wave claims We have made allowance for so-called “third-wave” claims. These are defined as claims for personal injury and / or death arising from asbestos exposure during home renovations by individuals or to builders involved in such renovations. Such claims are allowed for within the projections to the extent to which they have arisen to date and to the extent our exposure model factors in these exposures in its projection. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 8 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 We have not allowed for a significant additional surge in third-wave claims (over and above current levels of activity) in the future arising from renovations, but conversely we have not allowed for a tempering of those third-wave claims already included within our projection as a result of improved education of individuals as to the risks of such home renovations, or of any local Councils or State Governments passing laws in this regard. It should be noted that claims for the cost of asbestos or asbestos product removal from homes and properties or any claims for economic loss arising from asbestos or asbestos products being within such homes and properties is not required to be met by the AICF Trust. 1.4 Data reliances and limitations KPMG Actuarial has relied upon the accuracy and completeness of the data with which it has been provided. KPMG Actuarial has not verified the accuracy or completeness of the data, although we have undertaken steps to test its consistency with data previously received. However, KPMG Actuarial has placed reliance on the data previously received, and currently provided, as being accurate and complete in all material respects. 1.5 Uncertainty It must be understood that estimates of asbestos-related disease liabilities are subject to considerable uncertainty. This is due to the fact that the ultimate disposition of future claims will be subject to the outcome of events that have not yet occurred. Examples of these events, as noted in Section 1.3, include jury decisions, court interpretations, legislative changes, epidemiological developments, medical advancements, public attitudes, potential additional third-wave exposures and social and economic conditions such as inflation. Therefore, it should be expected that the actual emergence of the liabilities will vary, perhaps materially, from any estimate. Thus, no assurance can be given that the actual liabilities of the Liable Entities to be met by the AICF Trust will not ultimately exceed the estimates contained herein. Any such variation may be significant. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 9 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 1.6 Distribution and use The purpose of this Report is as stated in Section 1.1. This Report should not be used for any purpose other than those specified. This Report will be provided to the Board and management of AICFL. This Report will also be provided to the Board and management of James Hardie, the NSW Government and to Ernst & Young in their capacity as auditors to both James Hardie and AICFL. We understand that this Report will be filed with the ASX and placed on James Hardie’s website in its entirety. We understand that this Report will also be placed on AICFL’s website in its entirety. KPMG Actuarial consents to this Report being made available to the above-mentioned parties and for the Report to be distributed in the manner described above. To the extent permitted by law, neither KPMG Actuarial nor its Executives, directors or employees will be responsible to any third parties for the consequences of any actions they take based upon the opinions expressed with this Report, including any use of or purported reliance upon this Report not contemplated in Section 1.2. Any reliance placed is that party’s sole responsibility. Where distribution of this Report is permitted by KPMG Actuarial, the Report may only be distributed in its entirety and judgements about the conclusions and comments drawn from this Report should only be made after considering the Report in its entirety and with necessary consultation with KPMG Actuarial. Readers are also advised to refer to the “Important Note: Basis of Report” section at the front of the Executive Summary of this Report. 1.7 Date labelling convention used in this Report In our analyses throughout this Report (unless otherwise stated), the “year” we refer to aligns with the financial year of AICFL and James Hardie and runs from 1 April to 31 March. A “2008” notified claim would be a claim notified in the period 1 April 2008 to 31 March 2009. This might also be referred to as “2008/09” or “FY09”. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 10 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Similarly, a “2015” claim settlement would be a claim settled in the period 1 April 2015 to 31 March 2016. This might also be referred to as “2015/16” or “FY16”. 1.8 Author of the report This Report is authored by Neil Donlevy, an Executive of KPMG Actuarial Pty Ltd, a Fellow of the Institute of Actuaries (London) and a Fellow of the Institute of Actuaries of Australia. This Report is co-authored by Jefferson Gibbs, an Executive of KPMG Actuarial Pty Ltd, a Fellow of the Institute of Actuaries (London) and a Fellow of the Institute of Actuaries of Australia. In relation to this Report, the primary regulator for both Neil Donlevy and Jefferson Gibbs is the Institute of Actuaries of Australia. 1.9 Professional standards and compliance This Report details a valuation of the outstanding claims liabilities of entities which hold liabilities with features similar to general insurance liabilities as self-insured entities, and which have purchased related insurance protection. In preparing this Report, we have complied with the Professional Standard 300 of the Institute of Actuaries of Australia (“PS300”), “Valuation of General Insurance Claims”. However, as we note in Section 1.2, this Report does not include an allowance for the future Operating Expenses of the AICF Trust (which are estimated by AICFL) and nor does it include any allowance for a risk margin to reflect the inherent uncertainty in the liability assessment. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 11 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 1.10 Control processes and review This valuation report and the underlying analyses have been subject to technical review and internal peer review. The technical review focuses on ensuring that the valuation models and supporting claims experience analyses that are carried out are performed correctly and that the calculations are being correctly applied. The technical review also focuses on ensuring that the data that is being used has been reconciled insofar as possible. Internal peer review involves a review of the approach, the methods, the assumptions selected and the professional judgments applied. Both the technical review and internal peer review processes are applied to the Report as well as the valuation models. 1.11 Funding position of the AICF Trust This Report does not analyse nor provide any opinion on the current, or prospective, funding position of the AICF Trust, nor of its likely funding needs and its potential use of the loan facility provided by the NSW Government. This is because to do so within this Report would require consideration, estimation and documentation of the future financial performance of James Hardie. This Report only provides analysis and opinion on the estimates of the future expenditure to be met by the AICF Trust. The cashflow estimates contained in this Report assume that all claims against the Liable Entities will continue to be paid in full as and when they fall due. 1.12 Basis of preparation of Report We have been advised by the management of AICFL to prepare the Report on a “going concern” basis (i.e. we should assume that AICFL will be able to meet any shortfall in the cost of the liabilities of the Liable Entities as they fall due). © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 12 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 2 Data 2 2.1 Data provided to KPMG Actuarial We have been provided with the following data by AICFL: • Claims dataset at 31 March 2016 with individual claims listings; • Accounting transactions dataset at 31 March 2016 (which includes individual claims payment details); and • Detailed insurance bordereaux information (being a listing of claims filed with the insurers of the Liable Entities) produced by Randall & Quilter Investment Holdings as at 31 March 2016. We have allowed for the benefits of the product and public liability insurance policies of the Liable Entities based on information provided to us by AICFL relating to the insurance programme’s structure, coverage and layers. We have also considered the claims data listings which formed the basis of our previous valuation assessments. The data structures for the claims and accounting databases provided to us by AICFL as of 31 March 2016 are detailed in Appendix E. 2.2 Data limitations We have tested the consistency of the various data sets provided to us at different valuation dates. Section 2.3 outlines the nature of the testing undertaken. However, we have not otherwise verified the data and have instead relied on the data provided as being complete and accurate in all material respects. We have relied upon the robustness of AICFL’s internal administration and systems as to the completeness of the data provided. Consequently, should there be material errors or incompleteness in the data, our assessment could also be affected materially. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 13 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

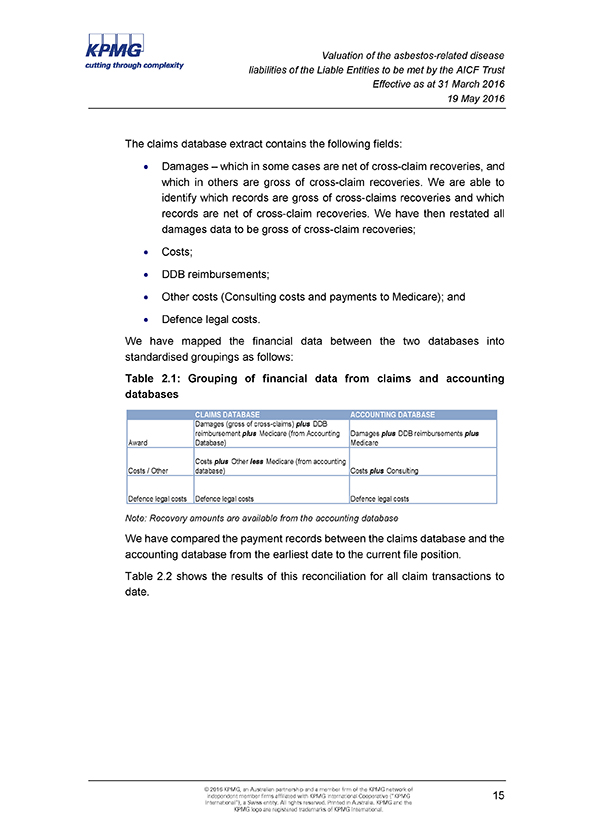

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 2.3 Data reconciliation and testing We have performed a reconciliation of the data provided at 31 March 2016 with the data provided at 31 March 2015. We have undertaken a number of tests and reconciliations to test the accuracy of the data to the extent possible, noting the limitations outlined above. 2.3.1 Reconciliation with previous valuation’s data We have performed a reconciliation of the claims database as at 31 March 2016 with that provided at 31 March 2015. Our findings are: • Claims notifications: There have been two claims with a report date prior to 31 March 2015 that were not present in the database at 31 March 2015. No claims changed notification date between the two databases. • Portfolio category: Five claims changed category. Of these, one related to claims reported in 2014/15, one related to 2013/14 and the remainder related to older periods of notification. • Settlement date: There have been three claims with a settlement date prior to 31 March 2015 that were not showing as being settled in the database at 31 March 2015. One additional claim changed its settlement date. Changing and developing data is not unexpected or to be considered as adverse. Indeed, changing data is common to all claims administration systems. We do not consider the number or extent of the changes noted above to be unreasonable, nor do we consider the changes to be material to the valuation. 2.3.2 Reconciliation of claims settlement amounts between claims and accounting databases The accounting database extract contains the following fields: • Damages – which are gross of cross-claim recoveries; • Costs; • DDB reimbursements; • Other costs; • Payments to Medicare; and • Defence legal costs. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 14 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 The claims database extract contains the following fields: • Damages – which in some cases are net of cross-claim recoveries, and which in others are gross of cross-claim recoveries. We are able to identify which records are gross of cross-claims recoveries and which records are net of cross-claim recoveries. We have then restated all damages data to be gross of cross-claim recoveries; • Costs; • DDB reimbursements; • Other costs (Consulting costs and payments to Medicare); and • Defence legal costs. We have mapped the financial data between the two databases into standardised groupings as follows: Table 2.1: Grouping of financial data from claims and accounting databases CLAIMS DATABASE ACCOUNTING DATABASE Damages (gross of cross-claims) plus DDB reimbursement plus Medicare (from Accounting Damages plus DDB reimbursements plus Award Database) Medicare Costs plus Other less Medicare (from accounting Costs / Other database) Costs plus Consulting Defence legal costs Defence legal costs Defence legal costs Note: Recovery amounts are available from the accounting database We have compared the payment records between the claims database and the accounting database from the earliest date to the current file position. Table 2.2 shows the results of this reconciliation for all claim transactions to date. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 15 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

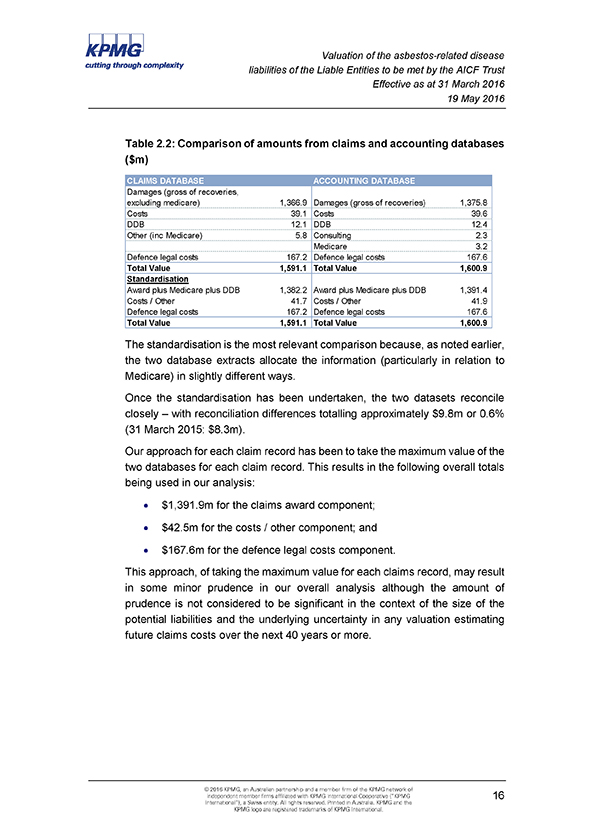

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 Table 2.2: Comparison of amounts from claims and accounting databases ($m) CLAIMS DATABASE ACCOUNTING DATABASE Damages (gross of recoveries, excluding medicare) 1,366.9 Damages (gross of recoveries) 1,375.8 Costs 39.1 Costs 39.6 DDB 12.1 DDB 12.4 Other (inc Medicare) 5.8 Consulting 2.3 Medicare 3.2 Defence legal costs 167.2 Defence legal costs 167.6 Total Value 1,591.1 Total Value 1,600.9 Standardisation Award plus Medicare plus DDB 1,382.2 Award plus Medicare plus DDB 1,391.4 Costs / Other 41.7 Costs / Other 41.9 Defence legal costs 167.2 Defence legal costs 167.6 Total Value 1,591.1 Total Value 1,600.9 The standardisation is the most relevant comparison because, as noted earlier, the two database extracts allocate the information (particularly in relation to Medicare) in slightly different ways. Once the standardisation has been undertaken, the two datasets reconcile closely – with reconciliation differences totalling approximately $9.8m or 0.6% (31 March 2015: $8.3m). Our approach for each claim record has been to take the maximum value of the two databases for each claim record. This results in the following overall totals being used in our analysis: • $1,391.9m for the claims award component; • $42.5m for the costs / other component; and • $167.6m for the defence legal costs component. This approach, of taking the maximum value for each claims record, may result in some minor prudence in our overall analysis although the amount of prudence is not considered to be significant in the context of the size of the potential liabilities and the underlying uncertainty in any valuation estimating future claims costs over the next 40 years or more. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 16 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 2.4 Data conclusion We have not verified the underlying data nor have we undertaken “auditing at source”. No material data issues have been identified and notified to us by the Approved Auditor of AICFL (Ernst & Young) during their testing. We have tested the data for internal consistency with the data provided at the previous valuation (31 March 2015). Based on that testing and reconciliation, and subject to the limitations described in Section 1.4, we have formed the view that: • Generally, the data is consistent between valuations, with any differences in the data being readily explainable; • The financial data appears to reconcile reasonably between the two data sources (the claims dataset and the accounting dataset); • Any data issues that have emerged are not significant in relation to the size of the liabilities; and • Therefore, the data is appropriate for use for the purposes of this Report. © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 17 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 3 Valuation Methodology and Approach 3 3.1 Previous valuation work and methodology changes We have, in broad terms, maintained the core valuation methodology adopted at our previous valuation at 31 March 2015. 3.2 Overview of current methodology The methodology involves assessing the liabilities in two separate components, being: • Allowance for the cost of settling claims which have already been reported but have not yet been settled (“pending claims”); and • Allowance for the cost of settling claims which have not yet been reported (“Incurred But Not Reported” or “IBNR” claims). For pending claims, we have used the case estimates (where available) with some adjustments to reflect the extent to which the case estimates (on average) tend to overstate the ultimate cost. For IBNR claims we have used what can best be described as an “average cost per claim method”. In brief, the overall methodology may be summarised as follows: • Project the future number of claims expected to be reported in each future year by disease type (for product and public liability) and for Workers Compensation and wharf claims taking into account the expected future incidence of mesothelioma and other diseases and also the past rate of co-joining of the Liable Entities; • Analyse past average attritional claim costs of non-nil claims in mid 2015/16 money terms. We have defined attritional claims to be claims which are less than $1m in 2006/07 money terms. We estimate a baseline attritional non-nil average claim cost in mid 2015/16 money terms. This represents the Liable Entities’ share of a claim rather than the total claim settlement. For Workers Compensation claims, the average cost represents only that part of a claim which is borne by the Liable Entities (i.e. it is net of any insurance proceeds from a Workers Compensation Scheme or Policy); © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 18 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.

Valuation of the asbestos-related disease liabilities of the Liable Entities to be met by the AICF Trust Effective as at 31 March 2016 19 May 2016 • Analyse past historical average plaintiff/other and defendant legal costs for non-nil claim settlements; • Analyse past historical average defendant legal costs for nil claim settlements; • Estimate a “large claims loading” for mesothelioma claims by estimating the frequency, or incidence rate, and average claim size and legal cost sizes of such claims (being claims which are in excess of $1m in 2006/07 money terms); • Project the pattern and incidence of future claims settlements from the claims reporting profile projected. This is done by using a settlement pattern derived from consideration of past experience of the pattern of delay between claim reporting and claim settlement for each disease type; • Estimate the proportion of claims which will be settled with no liability against the Liable Entities by reference to past proportions of claims settled for nil claim cost (we refer to this as the “nil settlement rate”); • Inflate average claim, plaintiff/other and defence legal costs and large claim costs to the date of settlement of claims allowing for base inflation and (where applicable) superimposed inflation; • Multiply the claims numbers which are expected to be settled for non-nil amounts in a period by the inflated average non-nil claim costs (including the “large claims loading”) and plaintiff/other and defence legal costs for that period; • Make allowance in defence legal costs for that proportion of settled claims which are expected to be settled for no liability but for which defence costs will be incurred; • Inflate average defence legal costs of nil claims to the date of settlement of claims allowing for base inflation; • Multiply the claims numbers which are expected to be settled for nil amounts in a period by the inflated average defence legal costs for nil claims for that period; • Add the expected claims and legal payments relating to pending claims (after allowance for the potential savings on case estimates) after making allowance for the assumed settlement pattern of pending claims; © 2016 KPMG, an Australian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG 19 International”), a Swiss entity. All rights reserved. Printed in Australia. KPMG and the KPMG logo are registered trademarks of KPMG International.