Exhibit 99.4

James Hardie

Q4 FY17

MANAGEMENT PRESENTATION

18 May 2017

CAUTIONARY NOTE ON FORWARD-LOOKING STATEMENTS

This Management Presentation contains forward-looking statements. James Hardie Industries plc (the “company”) may from time to time make forward-looking statements in its

periodic reports filed with or furnished to the Securities and Exchange Commission, on Forms 20-F and 6-K, in its annual reports to shareholders, in offering circulars,

invitation memoranda and prospectuses, in media releases and other written materials and in oral statements made by the company’s officers, directors or employees to analysts, institutional investors, existing and potential lenders,

representatives of the media and others. Statements that are not historical facts are forward-looking statements and such forward-looking statements are statements made pursuant to the Safe Harbor Provisions of the Private Securities Litigation

Reform Act of 1995.

Examples of forward-looking statements include:

statements about the company’s future performance;

projections of the

company’s results of operations or financial condition;

statements regarding the company’s plans, objectives or goals, including those relating to

strategies, initiatives, competition, acquisitions, dispositions and/or its products;

expectations concerning the costs associated with the suspension or closure

of operations at any of the company’s plants and future plans with respect to any such plants;

expectations concerning the costs associated with the

significant capital expenditure projects at any of the company’s plants and future plans with respect to any such projects;

expectations regarding the

extension or renewal of the company’s credit facilities including changes to terms, covenants or ratios;

expectations concerning dividend payments and share buy-backs;

statements concerning the company’s corporate and tax domiciles and structures and potential changes to them,

including potential tax charges;

statements regarding tax liabilities and related audits, reviews and proceedings;

statements regarding the possible consequences and/or potential outcome of legal proceedings brought against us and the potential liabilities, if any, associated with such

proceedings;

expectations about the timing and amount of contributions to Asbestos Injuries Compensation Fund (AICF), a special purpose fund for the compensation

of proven Australian asbestos-related personal injury and death claims;

expectations concerning the adequacy of the company’s warranty provisions and

estimates for future warranty-related costs;

statements regarding the company’s ability to manage legal and regulatory matters (including but not limited to

product liability, environmental, intellectual property and competition law matters) and to resolve any such pending legal and regulatory matters within current estimates and in anticipation of certain third-party recoveries; and

statements about economic conditions, such as changes in the US economic or housing market conditions or changes in the market conditions in the Asia Pacific region, the levels of

new home construction and home renovations, unemployment levels, changes in consumer income, changes or stability in housing values, the availability of mortgages and other financing, mortgage and other interest rates, housing affordability and

supply, the levels of foreclosures and home resales, currency exchange rates, and builder and consumer confidence.

James Hardie PAGE 2

CAUTIONARY NOTE ON FORWARD-LOOKING STATEMENTS (continued)

Words such as “believe,” “anticipate,” “plan,” “expect,” “intend,” “target,” “estimate,” “project,”

“predict,” “forecast,” “guideline,” “aim,” “will,” “should,” “likely,” “continue,” “may,” “objective,” “outlook” and similar expressions

are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Readers are cautioned not to place undue reliance on these forward-looking statements and all such forward-looking statements are

qualified in their entirety by reference to the following cautionary statements.

Forward-looking statements are based on the company’s current expectations,

estimates and assumptions and because forward-looking statements address future results, events and conditions, they, by their very nature, involve inherent risks and uncertainties, many of which are unforeseeable and beyond the company’s

control. Such known and unknown risks, uncertainties and other factors may cause actual results, performance or other achievements to differ materially from the anticipated results, performance or achievements expressed, projected or implied by

these forward-looking statements. These factors, some of which are discussed under “Risk Factors” in Section 3 of the Form 20-F filed with the Securities and Exchange Commission on 18 May

2017, include, but are not limited to: all matters relating to or arising out of the prior manufacture of products that contained asbestos by current and former company subsidiaries; required contributions to AICF, any shortfall in AICF and the

effect of currency exchange rate movements on the amount recorded in the company’s financial statements as an asbestos liability; governmental loan facility to AICF; compliance with and changes in tax laws and treatments; competition and

product pricing in the markets in which the company operates; the consequences of product failures or defects; exposure to environmental, asbestos, putative consumer class action or other legal proceedings; general economic and market conditions;

the supply and cost of raw materials; possible increases in competition and the potential that competitors could copy the company’s products; reliance on a small number of customers; a customer’s inability to pay; compliance with and

changes in environmental and health and safety laws; risks of conducting business internationally; compliance with and changes in laws and regulations; currency exchange risks; dependence on customer preference and the concentration of the

company’s customer base on large format retail customers, distributors and dealers; dependence on residential and commercial construction markets; the effect of adverse changes in climate or weather patterns; possible inability to renew credit

facilities on terms favorable to the company, or at all; acquisition or sale of businesses and business segments; changes in the company’s key management personnel; inherent limitations on internal controls; use of accounting estimates; and all

other risks identified in the company’s reports filed with Australian, Irish and US securities regulatory agencies and exchanges (as appropriate). The company cautions you that the foregoing list of factors is not exhaustive and that other

risks and uncertainties may cause actual results to differ materially from those referenced in the company’s forward-looking statements. Forward-looking statements speak only as of the date they are made and are statements of the company’s

current expectations concerning future results, events and conditions. The company assumes no obligation to update any forward-looking statements or information except as required by law.

James Hardie PAGE 3

NOTE TO THE READER

As of

30 June 2016, the Company changed its reportable operating segments. Previously, the Company reported on three operating segments: (i) North America and Europe Fiber Cement, (ii) Asia Pacific Fiber Cement, and (iii) Research and

Development. As of 30 June 2016, the Company began reporting on four operating segments: (i) North America Fiber Cement, (ii) International Fiber Cement, (iii) Other Businesses, and (iv) Research and Development. The

significant changes to how certain businesses are reported in the new segment structure are as follows: (i) our European business is now reported in the International Fiber Cement segment, along with the other businesses that were historically

reported in the Asia Pacific Fiber Cement segment, and (ii) business development, including some non-fiber cement operations, such as our windows business in North America, are now reported in the Other

Businesses segment as opposed to previously being reported in the North America and Europe Fiber Cement segment. The Company has provided its historical segment information for the fourth quarter and full year ended 31 March 2016 and 2015 to be

consistent with the new reportable segment structure. The change in reportable segments had no effect on the Company’s financial position, results of operations or cash flows for the periods presented. Readers are referred to Note 17 of our

consolidated financial statements for further information on our segments.

James Hardie PAGE 4

USE OF NON-GAAP FINANCIAL INFORMATION; AUSTRALIAN EQUIVALENT

TERMINOLOGY

This Management Presentation includes financial measures that are not considered a measure of financial performance under generally accepted accounting

principles in the United States (US GAAP). These financial measures are designed to provide investors with an alternative method for assessing our performance from on-going operations, capital efficiency and

profit generation. Management uses these financial measure for the same purposes. These financial measures include:

Adjusted EBIT;

Adjusted EBIT margin;

Adjusted net operating profit;

Adjusted diluted earnings per share;

Adjusted operating profit before income taxes;

Adjusted income tax expense;

Adjusted effective tax rate;

Adjusted EBITDA; and

Adjusted selling, general and administrative expenses (“Adjusted

SG&A”)

These financial measures are or may be non-US GAAP financial measures as defined in the rules of the U.S.

Securities and Exchange Commission and may exclude or include amounts that are included or excluded, as applicable, in the calculation of the most directly comparable financial measures calculated in accordance with US GAAP. These non-GAAP financial measures should not be considered to be more meaningful than the equivalent US GAAP measure. Management has included such measures to provide investors with an alternative method for

assessing its operating results in a manner that is focused on the performance of its ongoing operations and excludes the impact of certain legacy items, such as asbestos adjustments. Additionally, management uses such

non-GAAP financial measures for the same purposes. However, these non-GAAP financial measures are not prepared in accordance with US GAAP, may not be reported by

all of the Company’s competitors and may not be directly comparable to similarly titled measures of the Company’s competitors due to potential differences in the exact method of calculation. For additional information regarding the non-GAAP financial measures presented in this Management Presentation , including a reconciliation of each non-GAAP financial measure to the equivalent US GAAP measure,

see the slide titled “Non-US GAAP Financial Measures” included in the Appendix to this Management Presentation.

In addition, this Management Presentation includes financial measures and descriptions that are considered to not be in accordance with US GAAP, but which are

consistent with financial measures reported by Australian companies, such as operating profit, EBIT and EBIT margin. Since the Company prepares its Consolidated Financial Statements in accordance with US GAAP, the Company provides investors

with a table and definitions presenting cross-references between each US GAAP financial measure used in the Company’s Consolidated Financial Statements to the equivalent non-US GAAP financial measure

used in this Management Presentation. See the section titled “Non-US GAAP Financial Measures” included in the Appendix to this Management Presentation.

James Hardie PAGE 5

AGENDA

Overview and

Operating Review – Louis Gries, CEO

Financial Review – Matt Marsh, EVP and CFO

Questions and Answers

James Hardie PAGE 6

James Hardie

OVERVIEW AND

OPERATING REVIEW

Louis Gries, CEO

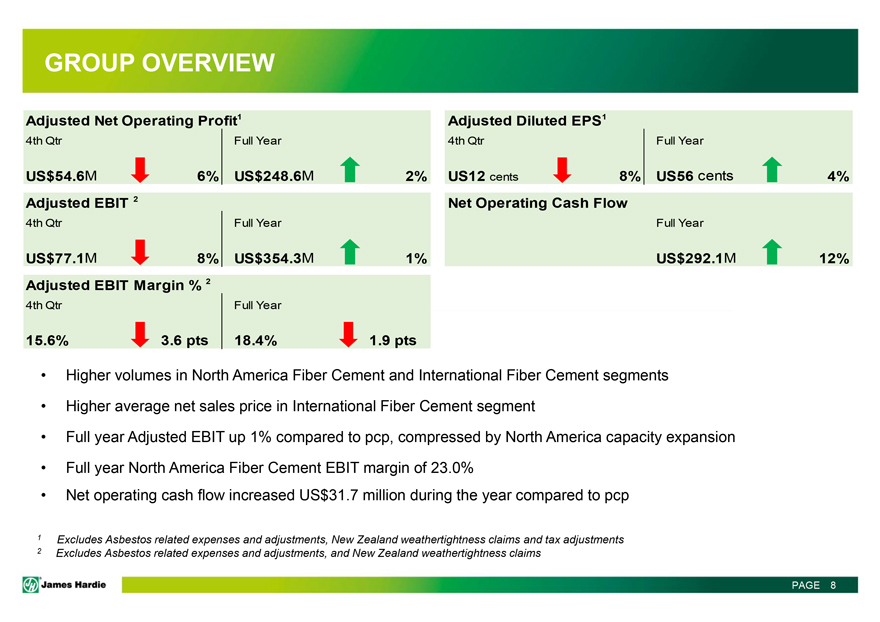

GROUP OVERVIEW

Adjusted

Net Operating Profit1

4th Qtr

Full Year

US$54.6M 6%

US$248.6M 2%

Adjusted EBIT

2

4th Qtr

Full Year

US$77.1M 8% US$354.3M

1%

Adjusted EBIT

Margin % 2

4th Qtr

Full Year

15.6%

3.6 pts

18.4%

1.9 pts

Adjusted Diluted EPS1

4th Qtr

Full Year

US12 cents

8%

US56 cents

4%

Net Operating Cash Flow

Full Year

US$292.1M

12%

Higher volumes in North America Fiber Cement and International Fiber Cement segments

Higher average net sales price in International Fiber Cement segment

Full

year Adjusted EBIT up 1% compared to pcp, compressed by North America capacity expansion

Full year North America Fiber Cement EBIT margin of 23.0%

Net operating cash flow increased US$31.7 million during the year compared to pcp

1

Excludes Asbestos related expenses and adjustments, New Zealand weathertightness claims and tax adjustments

2 Excludes Asbestos related expenses and adjustments,

and New Zealand weathertightness claims

James Hardie PAGE 8

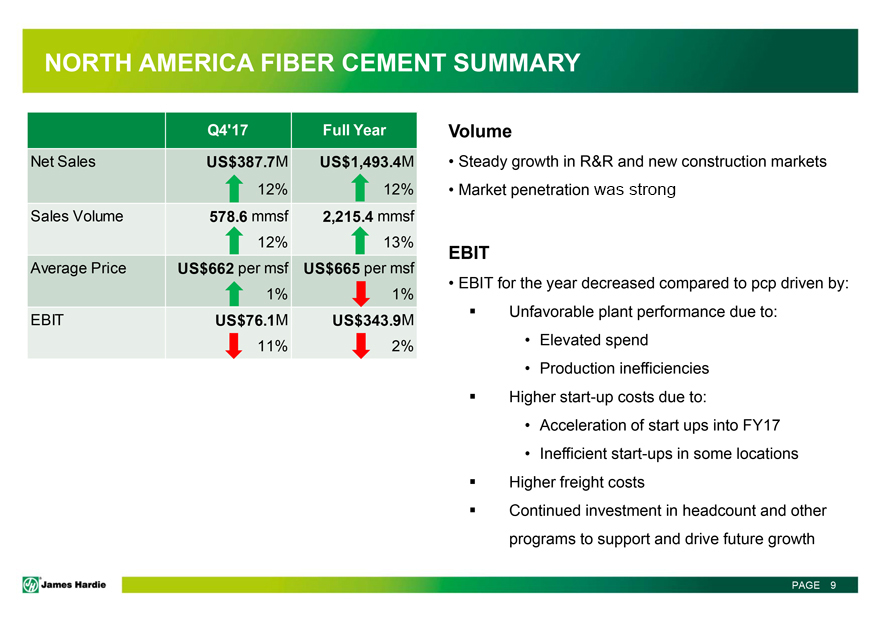

NORTH AMERICA FIBER CEMENT SUMMARY

Q4’17 Full Year

Net Sales

US$387.7M US$1,493.4M

12%

12%

Sales Volume

578.6 mmsf

2,215.4 mmsf

12%

13%

Average Price

US$662 per msf US$665 per msf

1%

1%

EBIT

US$76.1M US$343.9M

11%

2%

Volume

Steady growth in R&R and new construction markets

Market penetration was strong

EBIT

EBIT for the year decreased compared to pcp driven by:

Unfavorable plant performance due to:

Elevated spend

Production inefficiencies

Higher start-up costs due to:

Acceleration of start

ups into FY17

Inefficient start-ups in some locations

Higher freight costs

Continued investment in headcount and other programs to support and drive

future growth

James Hardie PAGE 9

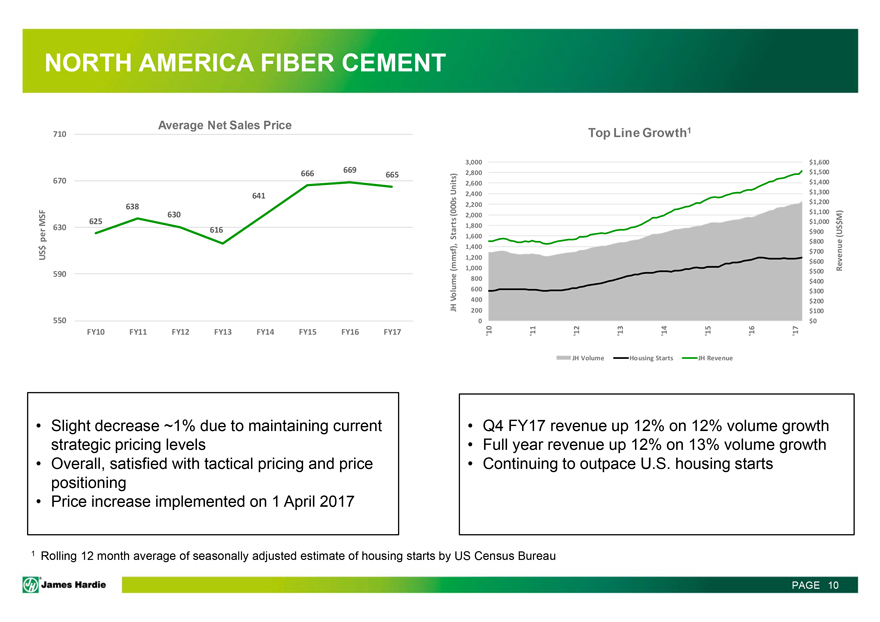

NORTH AMERICA FIBER CEMENT

US$ per MSF

Average Net Sales Price

710

670

630

590

550

669

666

665

641

638

630

625

616

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Slight decrease ~1% due to maintaining current strategic pricing levels

Overall, satisfied

with tactical pricing and price positioning

Price increase implemented on 1 April 2017

Top Line Growth1

JH Volume (mmsf), Starts (000s Units)

Revenue (US$M)

3,000

2,800

2,600

2,400

2,200

2,000

1,800

1,600

1,400

1,200

1,000

800

400

200

0

$1,600

$1,500

$1,400

$1,300

$1,200

$1,100

$1,000

$900

$800

$700

$600

$500

$400

$300

$200

$100

$0

‘10

‘11

‘12

‘13

‘14

‘15

‘16

‘17

JH Volume Housing Starts JH Revenue

Q4 FY17 revenue up 12% on 12% volume growth

Full year revenue up 12% on 13% volume growth

Continuing to outpace U.S. housing starts

1 Rolling 12 month average of

seasonally adjusted estimate of housing starts by US Census Bureau

JH James Hardie PAGE 10

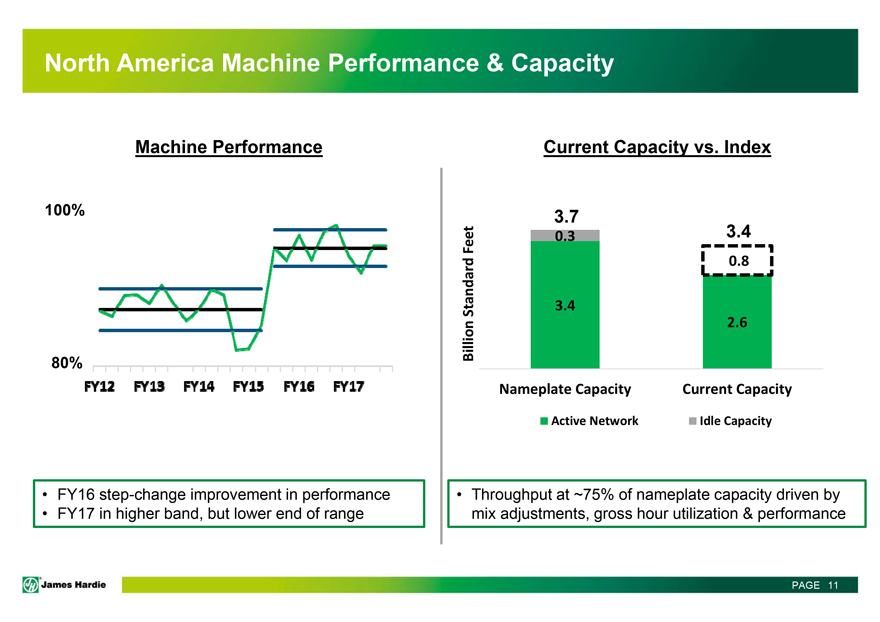

North America Machine Performance & Capacity

Machine Performance

100%

80%

FY12 FY13 FY14 FY15 FY16 FY17

FY16 step-change improvement in performance

FY17 in higher band, but lower end of range

Current Capacity vs. Index

Billion Standard Feet

3.7

0.3 3.4

0.8

3.4

2.6

Nameplate Capacity Current Capacity

Active Network Idle Capacity

Throughput at ~75% of nameplate capacity driven by mix

adjustments, gross hour utilization & performance

JH James Hardie PAGE 11

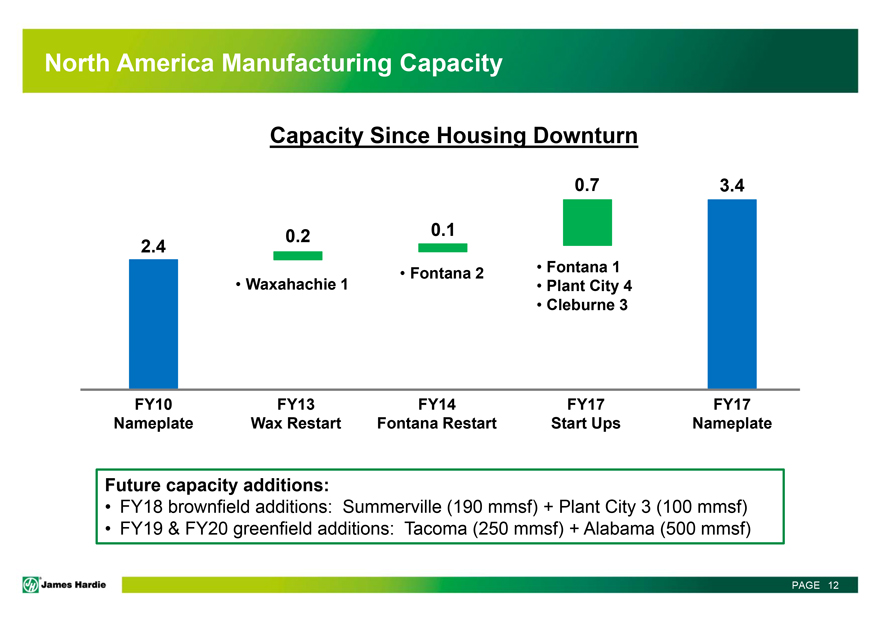

North America Manufacturing Capacity

Capacity Since Housing Downturn

0.7 3.4

0.2 0.1

2.4

Fontana 2 Fontana 1

Waxahachie 1 Plant City 4

Cleburne 3

FY10 FY13 FY14 FY17 FY17

Nameplate Wax Restart Fontana Restart Start Ups Nameplate

Future capacity additions:

FY18 brownfield additions: Summerville (190 mmsf) + Plant City 3 (100 mmsf)

FY19 & FY20 greenfield additions: Tacoma (250 mmsf) + Alabama (500 mmsf)

JH James Hardie PAGE 12

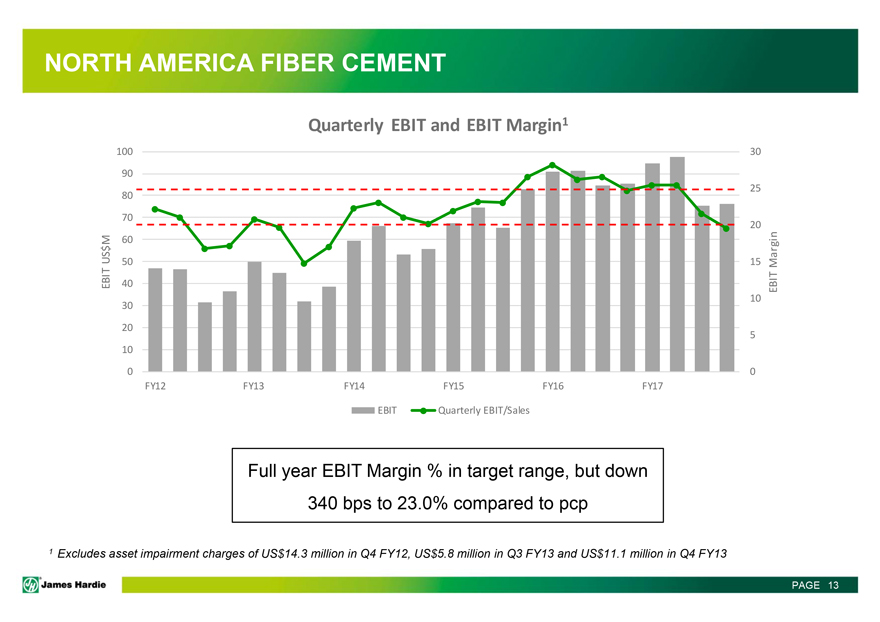

NORTH AMERICA FIBER CEMENT

Quarterly EBIT and EBIT Margin1

EBIT US$M

EBIT Margin

100

90

80

70

60

50

40

30

20

10

0

30

25

20

15

10

5

0

FY12

FY13 FY14 FY15 FY16 FY17

EBIT Quarterly EBIT/Sales

Full year EBIT Margin

% in target range, but down 340 bps to 23.0% compared to pcp

1 Excludes asset impairment charges of US$14.3 million in Q4 FY12, US$5.8 million in Q3 FY13

and US$11.1 million in Q4 FY13

JH James Hardie PAGE 13

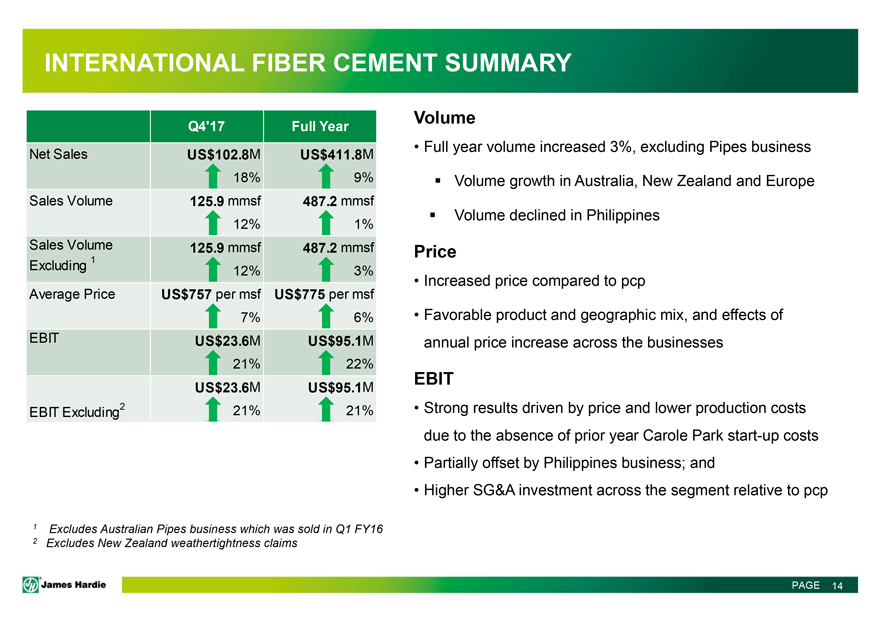

INTERNATIONAL FIBER CEMENT SUMMARY

Q4’17 Full Year

Net SalesUS$102.8M US$411.8M

18% 9%

Sales Volume 125.9 mmsf 487.2 mmsf

12% 1%

Sales Volume 125.9 mmsf 487.2 mmsf

Excluding 1 12% 3%

Average Price US$757 per msf US$775 per msf

7% 6%

EBIT US$23.6M US$95.1M

21% 22%

US$23.6M US$95.1M

EBIT Excluding2 21% 21%

Volume

Full year volume increased 3%, excluding Pipes business

Volume growth in Australia, New

Zealand and Europe

Volume declined in Philippines

Price

Increased price compared to pcp

Favorable product and geographic mix, and effects of annual

price increase across the businesses

EBIT

Strong results driven by price and

lower production costs due to the absence of prior year Carole Park start-up costs

Partially offset by Philippines

business; and

Higher SG&A investment across the segment relative to pcp

1

Excludes Australian Pipes business which was sold in Q1 FY16

2 Excludes New Zealand weathertightness claims

JH James Hardie PAGE 14

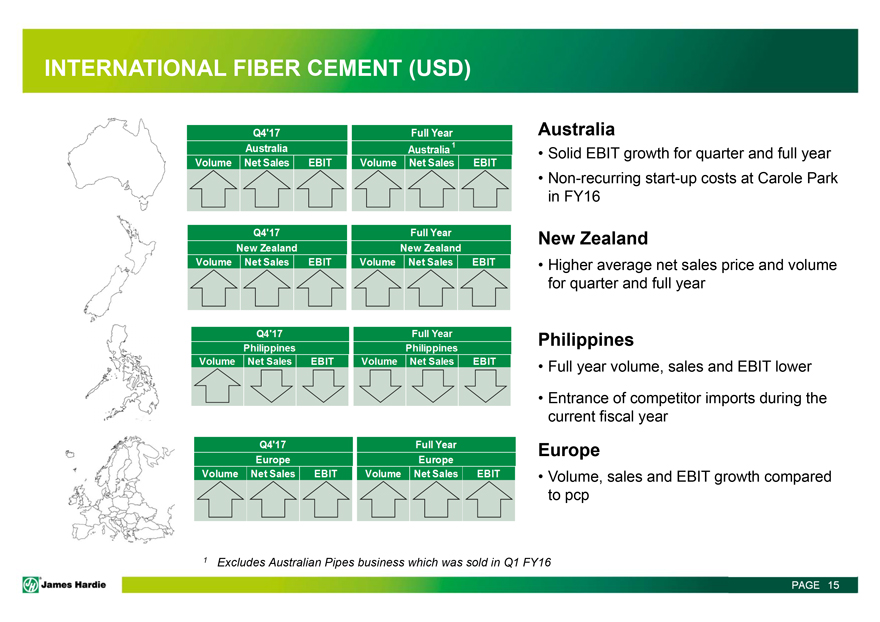

INTERNATIONAL FIBER CEMENT (USD)

Q4’17 Full Year

Australia Australia1

Volume Net Sales EBIT Volume Net Sales EBIT

Q4’17 Full Year

New Zealand New Zealand

Volume Net Sales EBIT Volume Net Sales EBIT

Q4’17 Full Year

Philippines Philippines

Volume Net Sales EBIT Volume Net Sales EBIT

Q4’17 Full Year

Europe Europe

Volume Net Sales EBIT Volume Net Sales EBIT

Australia

Solid EBIT growth for quarter and full year

Non-recurring start-up costs at Carole Park in FY16

New Zealand

Higher average net sales price and volume for quarter and full year

Philippines

Full year volume, sales and EBIT lower

Entrance of competitor imports during the current

fiscal year

Europe

Volume, sales and EBIT growth compared to pcp

1 Excludes Australian Pipes business which was sold in Q1 FY16

James Hardie PAGE 15

JH James Hardie

FINANCIAL

REVIEW

Matt Marsh, EVP and CFO

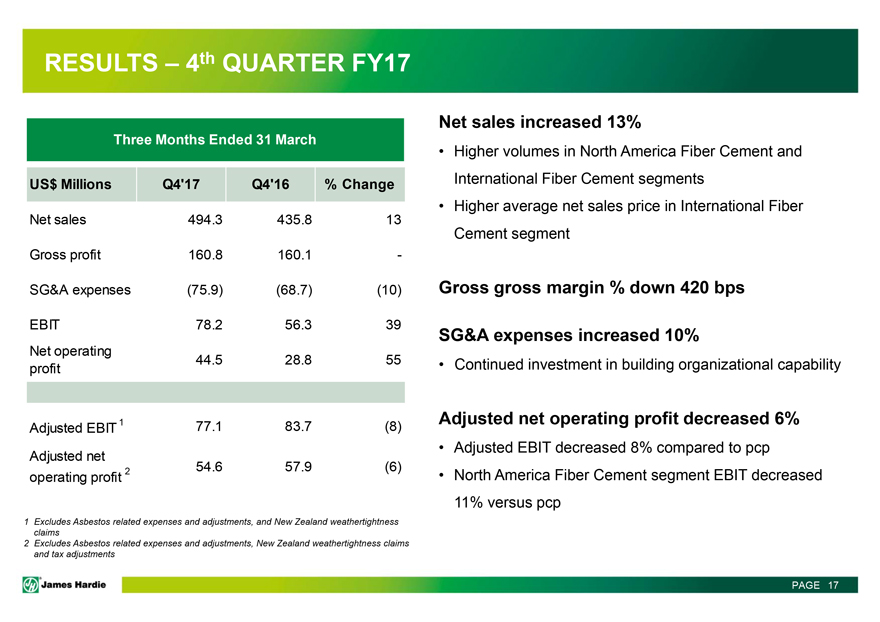

RESULTS – 4th QUARTER FY17

Three Months Ended 31 March

US$ Millions Q4’17 Q4’16 % Change

Net sales 494.3 435.8 13

Gross profit 160.8 160.1 -

SG&A expenses (75.9) (68.7) (10)

EBIT 78.2 56.3 39

Net operating 44.5 28.8 55

profit

Adjusted EBIT 1 77.1 83.7 (8)

Adjusted net

2 54.6 57.9 (6)

operating profit

Net sales increased 13%

Higher volumes in North America Fiber Cement and International Fiber

Cement segments

Higher average net sales price in International Fiber Cement segment

Gross gross margin % down 420 bps

SG&A expenses increased 10%

Continued investment in building organizational capability

Adjusted net operating profit

decreased 6%

Adjusted EBIT decreased 8% compared to pcp

North America Fiber

Cement segment EBIT decreased 11% versus pcp

1 Excludes Asbestos related expenses and adjustments, and New Zealand weathertightness claims

2 Excludes Asbestos related expenses and adjustments, New Zealand weathertightness claims and tax adjustments

JH James Hardie PAGE 17

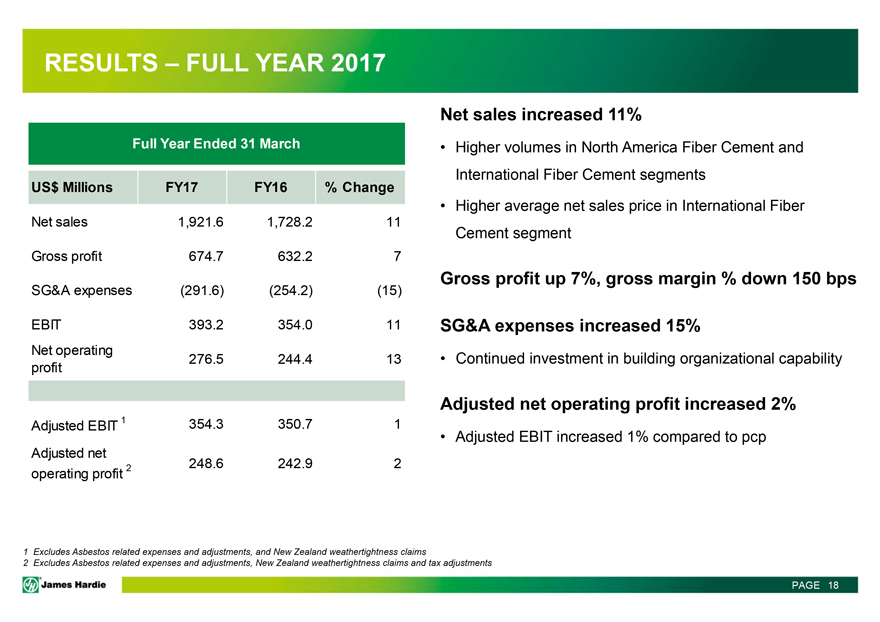

RESULTS – FULL YEAR 2017

Full Year Ended 31 March

US$ Millions FY17 FY16 % Change

Net sales 1,921.6 1,728.2 11

Gross profit 674.7 632.2 7

SG&A expenses (291.6) (254.2) (15)

EBIT 393.2 354.0 11

Net operating profit 276.5 244.4 13

Adjusted EBIT 1 354.3 350.7 1

Adjusted net

2 248.6 242.9 2

operating profit

Net sales increased 11%

Higher volumes in North America Fiber Cement and International Fiber Cement segments

Higher

average net sales price in International Fiber Cement segment

Gross profit up 7%, gross margin % down 150 bps

SG&A expenses increased 15%

Continued investment in building organizational capability

Adjusted net operating profit increased 2%

Adjusted EBIT increased 1%

compared to pcp

1 Excludes Asbestos related expenses and adjustments, and New Zealand weathertightness claims

2 Excludes Asbestos related expenses and adjustments, New Zealand weathertightness claims and tax adjustments

JH James Hardie PAGE 18

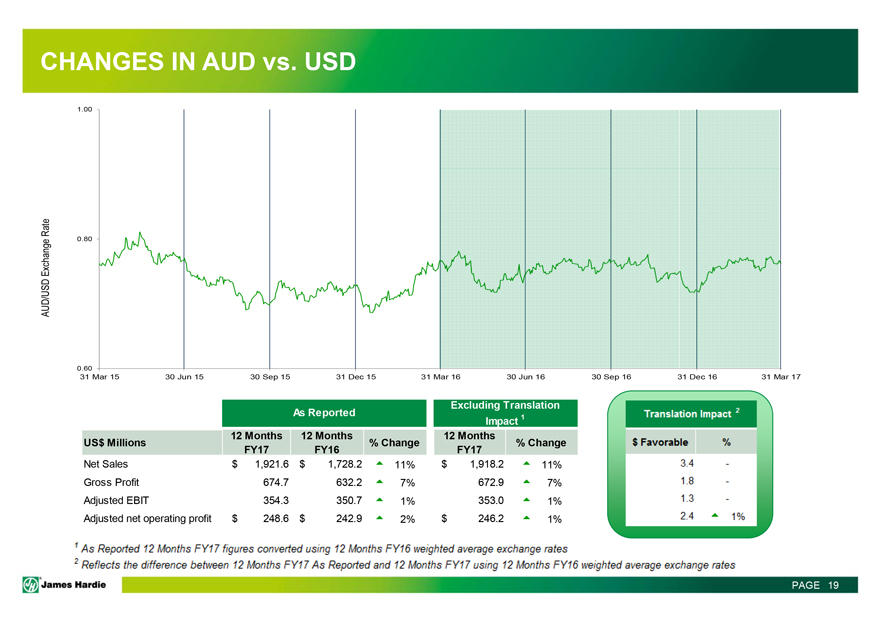

CHANGES IN AUD vs. USD

AUD/USD Exchange Rate

1.00

0.80

0.60

31 Mar 15 30 Jun 15 30 Sep 15 31 Dec 15 31 Mar 16 30 Jun 16 30 Sep 16 31 Dec 16 31 Mar 17

As Reported Excluding Translation Impact 1

US$ Millions % Change 12 Months FY17 12 Months FY16

12 Months FY17 % Change

Net Sales $1,921.6 $1,728.2 11% $1,918.2 11%

Gross

Profit 674.7 632.2 7% 672.9 7%

Adjusted EBIT 354.3 350.7 1% 353.0 1%

Adjusted

net operating profit $248.6 $242.9 2% $246.2 1%

Translation Impact2

$

Favorable %

3.4 -

1.8 -

1.3 -

2.4 1%

1 As Reported 12 Months FY17 figures converted using 12 Months FY16 weighted average exchange rates

2 Reflects the difference between 12 Months FY17 As Reported and 12 Months FY17 using 12 Months FY16 weighted average exchange rates

JH James Hardie PAGE 19

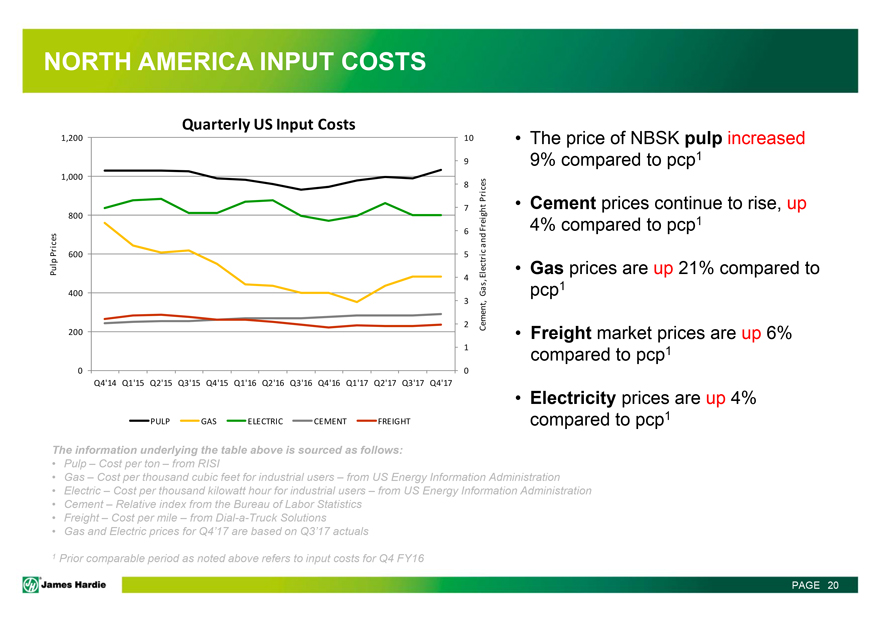

NORTH AMERICA INPUT COSTS

Quarterly US Input Costs

Pulp Prices

Cement, Gas, Electric and Freight Prices

1,200

1,000

800

600

400

200

0

10

9

8

7

6

5

4

3

2

1

0

Q4’14 Q1’15 Q2’15 Q3’15 Q4’15 Q1’16 Q2’16 Q3’16 Q4’16 Q1’17 Q2’17 Q3’17 Q4’17

PULP GAS ELECTRIC CEMENT FREIGHT

The price of NBSK pulp increased 9% compared to pcp1

Cement prices continue to rise, up 4% compared to pcp1

Gas prices are up 21%

compared to pcp1

Freight market prices are up 6% compared to pcp1

Electricity

prices are up 4% compared to pcp1

The information underlying the table above is sourced as follows:

Pulp – Cost per ton – from RISI

Gas – Cost per thousand cubic feet for

industrial users – from US Energy Information Administration

Electric – Cost per thousand kilowatt hour for industrial users – from US Energy

Information Administration

Cement – Relative index from the Bureau of Labor Statistics

Freight – Cost per mile – from Dial-a-Truck Solutions

Gas and Electric prices for

Q4’17 are based on Q3’17 actuals

1 Prior comparable period as noted above refers to input costs for Q4 FY16

JH James Hardie PAGE 20

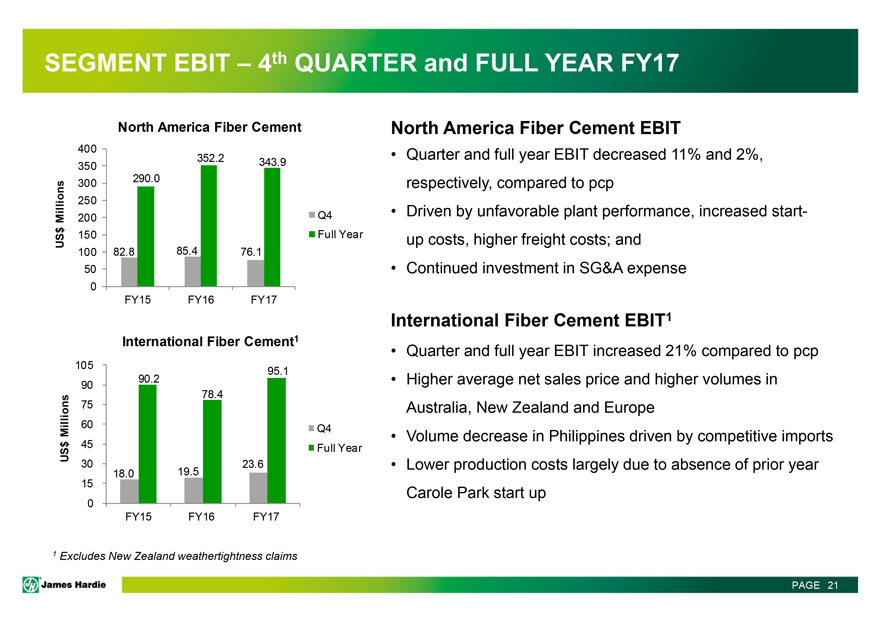

SEGMENT EBIT – 4th QUARTER and FULL YEAR FY17

North America Fiber Cement

US$ Millions

400

350

300

250

200

150

100

50

0

352.2 343.9 290.0 82.8 85.4 76.1

FY15 FY16 FY17

Q4

Full Year

International Fiber Cement1

US$ Millions

105

90

75

60

45

30

15

0

95.1 90.2 78.4 23.6 18.0 19.5

FY15 FY16 FY17

Q4

Full Year

North America Fiber Cement EBIT

Quarter and full year EBIT decreased 11% and 2%, respectively,

compared to pcp

Driven by unfavorable plant performance, increased startup costs, higher freight costs; and

Continued investment in SG&A expense

International Fiber Cement EBIT1

Quarter and full year EBIT increased 21% compared to pcp

Higher average net sales price and

higher volumes in Australia, New Zealand and Europe

Volume decrease in Philippines driven by competitive imports

Lower production costs largely due to absence of prior year Carole Park start up

1 Excludes

New Zealand weathertightness claims

JH James Hardie PAGE 21

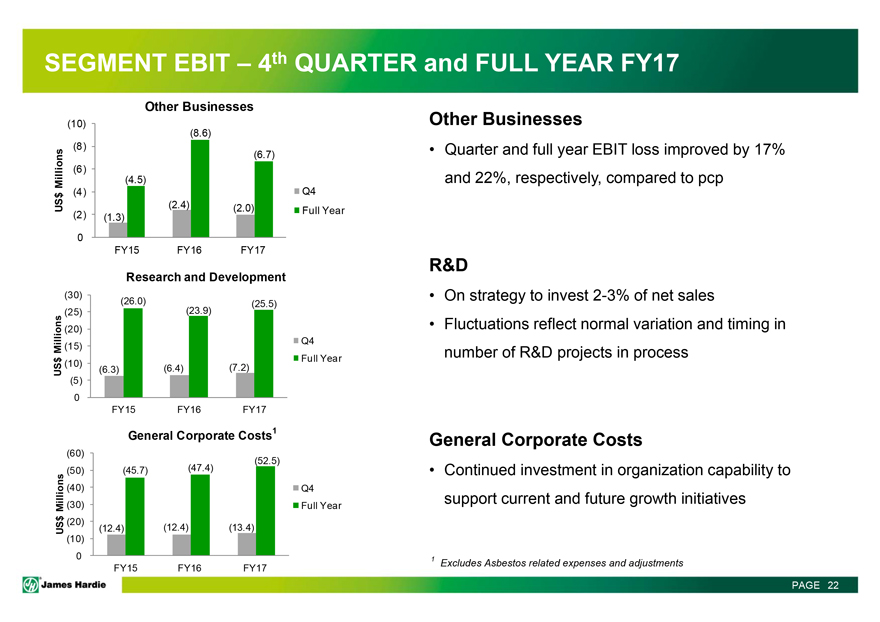

SEGMENT EBIT – 4th QUARTER and FULL YEAR FY17

Other Businesses

US$ Millions

(10)

(8)

(6)

(4)

(2)

0

(8.6) (6.7) (4.5) (2.4) (2.0) (1.3)

FY15 FY16 FY17

Q4

Full Year

Research and Development

US$ Millions

(30)

(25)

(20)

(15)

(10)

(5)

0

(26.0) (25.5) (23.9) (6.3) (6.4) (7.2)

FY15 FY16 FY17

Q4

Full Year

General Corporate Costs1

US$ Millions

(60)

(50)

(40)

(30)

(20)

(10)

0

(52.5) (45.7) (47.4) (12.4) (12.4) (13.4)

FY15 FY16 FY17

Q4

Full Year

Other Businesses

Quarter and full year EBIT loss improved by 17% and 22%, respectively,

compared to pcp

R&D

On strategy to invest 2-3% of net sales

Fluctuations reflect normal variation and timing in number of R&D projects in process

General Corporate Costs

Continued investment in organization capability to

support current and future growth initiatives

1 Excludes Asbestos related expenses and adjustments

JH James Hardie PAGE 22

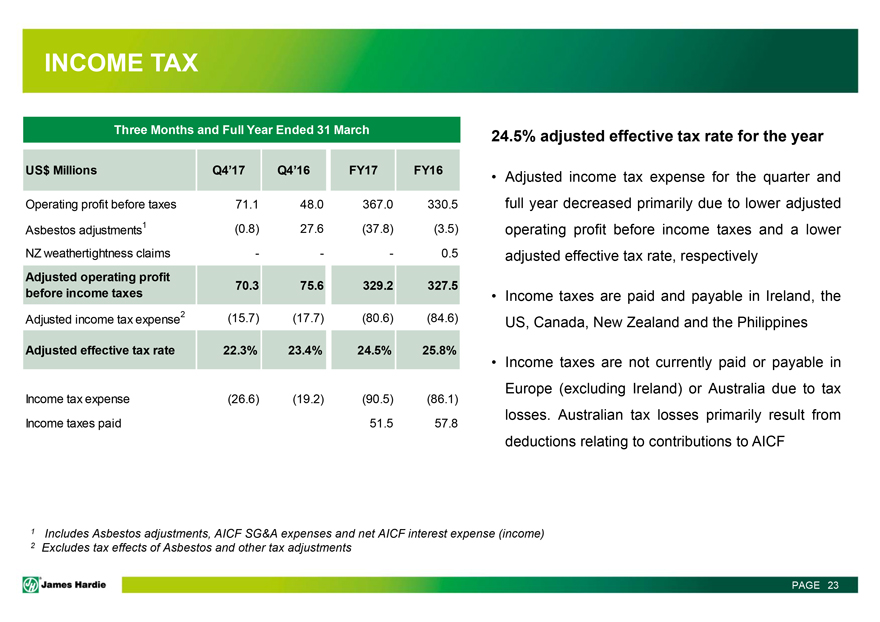

INCOME TAX

Three Months

and Full Year Ended 31 March US$ Millions Q4’17 Q4’16 FY17 FY16 Operating profit before taxes 71.1 48.0 367.0 330.5 Asbestos adjustments1 (0.8) 27.6 (37.8) (3.5) NZ weathertightness claims — —

— 0.5 Adjusted operating profit before income taxes 70.3 75.6 329.2 327.5 Adjusted income tax expense2 (15.7) (17.7) (80.6) (84.6) Adjusted effective tax rate 22.3% 23.4% 24.5% 25.8% Income tax expense (26.6) (19.2) (90.5) (86.1)

Income taxes paid 51.5 57.8

24.5% adjusted effective tax rate for the year

Adjusted income tax expense for the quarter and full year decreased primarily due to lower adjusted operating profit before income taxes and a lower adjusted

effective tax rate, respectively

Income taxes are paid and payable in Ireland, the US, Canada, New Zealand and the Philippines

Income taxes are not currently paid or payable in Europe (excluding Ireland) or Australia due to tax losses. Australian tax losses primarily result from deductions relating to

contributions to AICF

1 Includes Asbestos adjustments, AICF SG&A expenses and net AICF interest expense (income)

2 Excludes tax effects of Asbestos and other tax adjustments

JH James Hardie PAGE 23

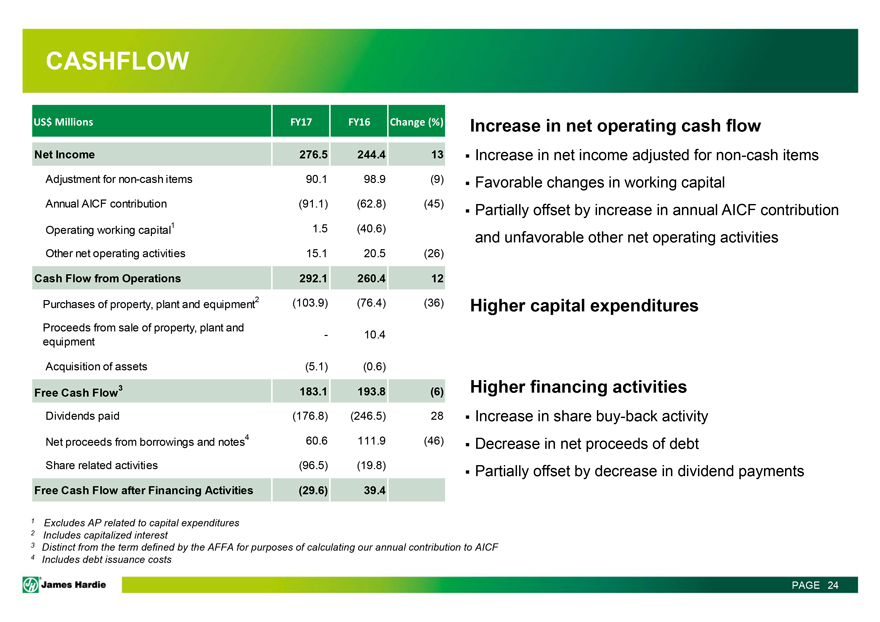

CASHFLOW

US$ Millions

FY17 FY16 Change (%) Net Income 276.5 244.4 13 Adjustment for non-cash items 90.1 98.9 (9) Annual AICF contribution (91.1) (62.8) (45) Operating working capital1 1.5 (40.6) Other net operating activities 15.1 20.5 (26) Cash Flow from Operations

292.1 260.4 12 Purchases of property, plant and equipment2 (103.9) (76.4) (36) Proceeds from sale of property, plant and equipment — 10.4 Acquisition of assets (5.1) (0.6) Free Cash Flow3 183.1 193.8 (6) Dividends paid (176.8) (246.5) 28 Net

proceeds from borrowings and notes4 60.6 111.9 (46) Share related activities (96.5) (19.8) Free Cash Flow after Financing Activities (29.6) 39.4

Increase in net

operating cash flow

Increase in net income adjusted for non-cash items

Favorable changes in working capital

Partially offset by increase in annual

AICF contribution and unfavorable other net operating activities

Higher capital expenditures

Higher financing activities

Increase in share buy-back activity

Decrease in net proceeds of debt

Partially offset by decrease in dividend payments

1 Excludes AP related to capital expenditures

2 Includes capitalized interest

3 Distinct from the term defined by the AFFA for purposes of calculating our annual contribution to AICF

4 Includes debt issuance costs

JH James Hardie PAGE 24

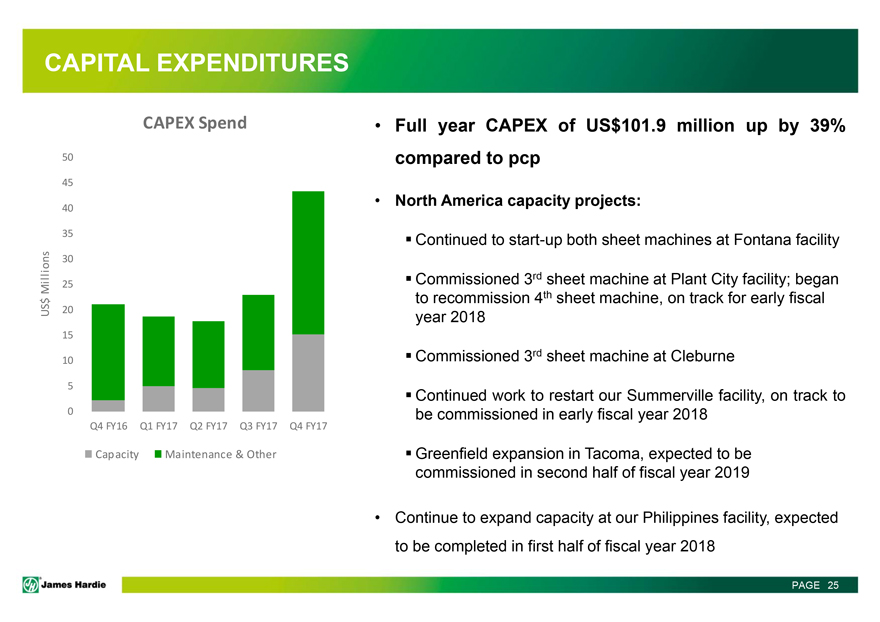

CAPITAL EXPENDITURES

CAPEX Spend

US$ Millions

50

45

40

35

30

25

20

15

10

5

0

Q4 FY16 Q1 FY17 Q2 FY17 Q3 FY17 Q4 FY17

Capacity Maintenance & Other

Full year CAPEX of US$101.9 million up by 39% compared to pcp

North America capacity projects:

Continued to start-up both sheet machines at

Fontana facility

Commissioned 3rd sheet machine at Plant City facility; began to recommission 4th sheet machine, on track for early fiscal year 2018

Commissioned 3rd sheet machine at Cleburne

Continued work to restart our Summerville facility,

on track to be commissioned in early fiscal year 2018

Greenfield expansion in Tacoma, expected to be commissioned in second half of fiscal year 2019

Continue to expand capacity at our Philippines facility, expected to be completed in first half of fiscal year 2018

JH James Hardie PAGE 25

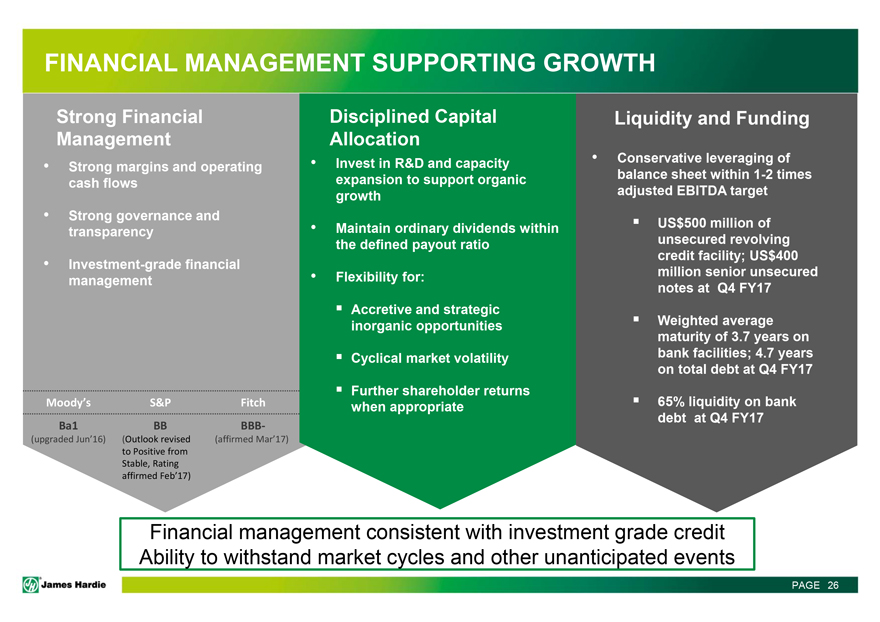

FINANCIAL MANAGEMENT SUPPORTING GROWTH

Strong Financial Management

Strong margins and operating cash flows

Strong governance and transparency

Investment-grade financial management

Moody’s Ba1 (upgraded Jun’16) S&P BB (Outlook revised to Positive from Stable, Rating affirmed Feb’17) Fitch BBB- (affirmed Mar’17)

Disciplined Capital Allocation

Invest in R&D and capacity expansion to support organic

growth

Maintain ordinary dividends within the defined payout ratio

Flexibility for:

Accretive and strategic inorganic opportunities

Cyclical market volatility Further shareholder returns when appropriate

Liquidity and Funding

Conservative leveraging of balance sheet within 1-2 times adjusted EBITDA target

US$500 million of unsecured revolving credit facility; US$400 million senior unsecured notes at Q4 FY17

Weighted average maturity of 3.7 years on bank facilities; 4.7 years on total debt at Q4 FY17

65% liquidity on bank debt at Q4 FY17

Financial management consistent with

investment grade credit Ability to withstand market cycles and other unanticipated events

JH James Hardie PAGE 26

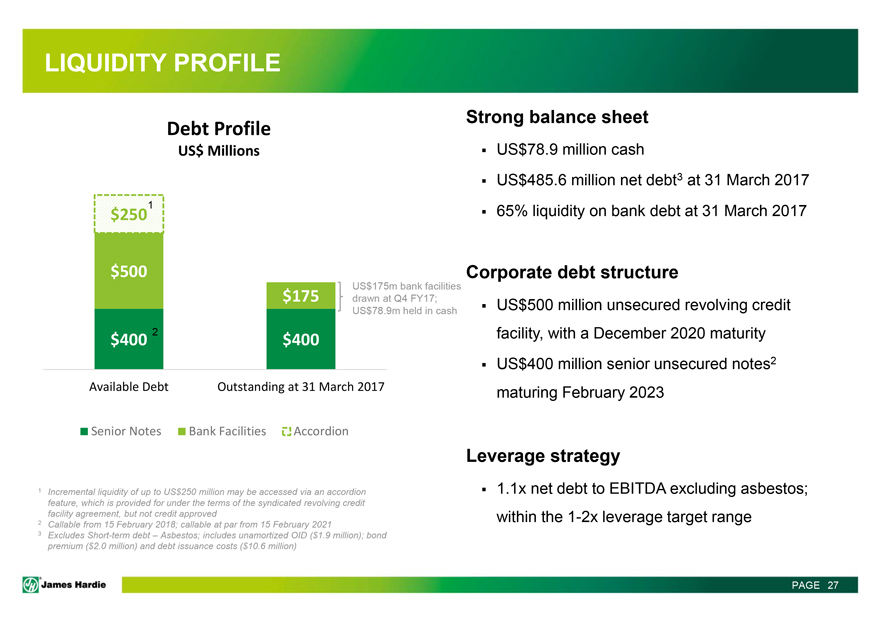

LIQUIDITY PROFILE

Debt

Profile

US$ Millions

$2501 $500 $400 2 $175 $400

Available Debt Outstanding at 31 March 2017

Senior Notes Bank Facilities Accordion

US$175m bank facilities drawn at Q4 FY17; US$78.9m held in cash

1 Incremental liquidity of up

to US$250 million may be accessed via an accordion feature, which is provided for under the terms of the syndicated revolving credit facility agreement, but not credit approved

2 Callable from 15 February 2018; callable at par from 15 February 2021

3 Excludes Short-term

debt – Asbestos; includes unamortized OID ($1.9 million); bond premium ($2.0 million) and debt issuance costs ($10.6 million)

Strong balance sheet

US$78.9 million cash

US$485.6 million net debt3 at 31 March 2017

65% liquidity on bank debt at 31 March 2017

Corporate debt structure

US$500 million unsecured revolving credit facility, with a December 2020 maturity

US$400

million senior unsecured notes2 maturing February 2023

Leverage strategy

1.1x

net debt to EBITDA excluding asbestos; within the 1-2x leverage target range

JH James Hardie PAGE 27

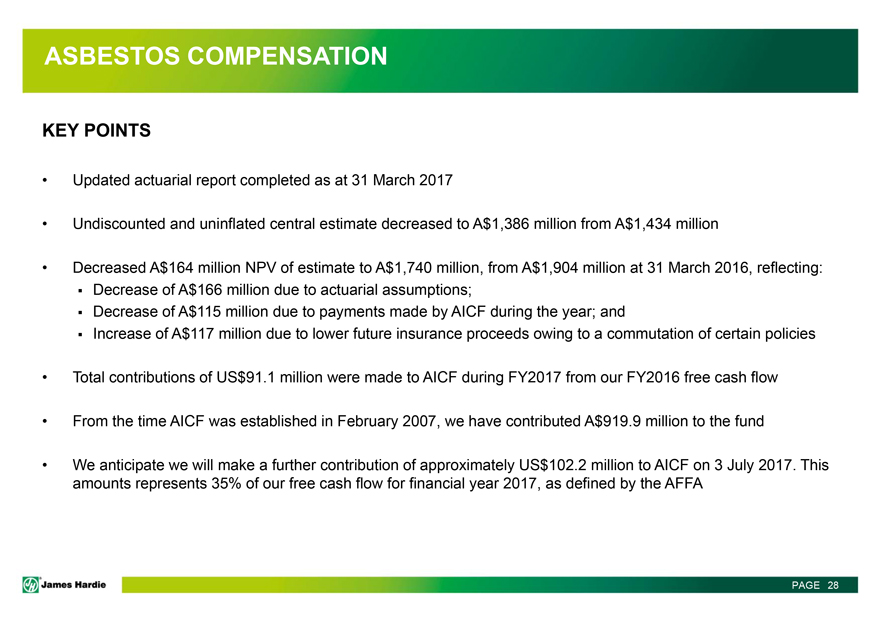

ASBESTOS COMPENSATION

KEY

POINTS

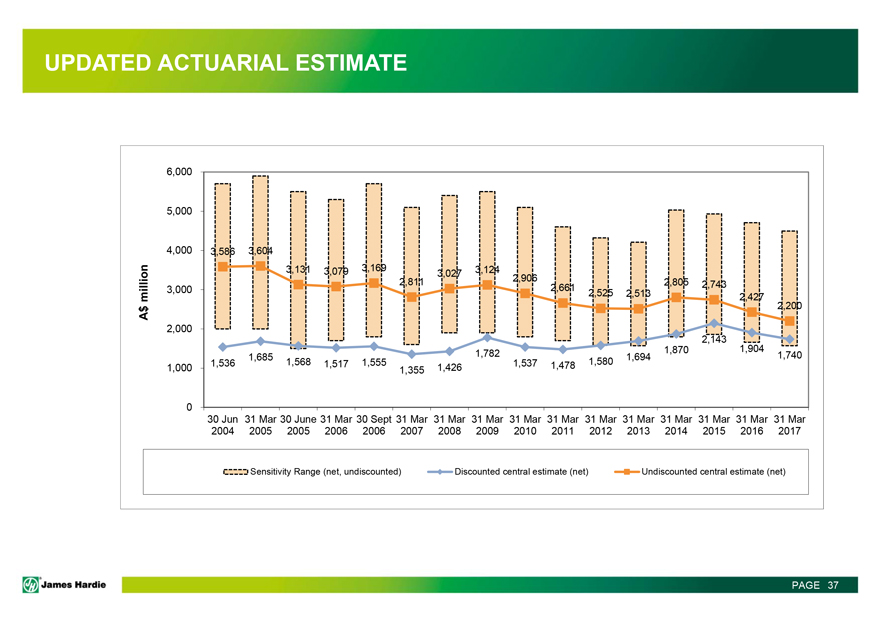

Updated actuarial report completed as at 31 March 2017

Undiscounted and uninflated central estimate decreased to A$1,386 million from A$1,434 million

Decreased A$164 million NPV of estimate to A$1,740 million, from A$1,904 million at 31 March 2016, reflecting:

Decrease of A$166 million due to actuarial assumptions;

Decrease of A$115 million

due to payments made by AICF during the year; and

Increase of A$117 million due to lower future insurance proceeds owing to a commutation of certain policies

Total contributions of US$91.1 million were made to AICF during FY2017 from our FY2016 free cash flow

From the time AICF was established in February 2007, we have contributed A$919.9 million to the fund

We anticipate we will make a further contribution of approximately US$102.2 million to AICF on 3 July 2017. This amounts represents 35% of our free cash flow for

financial year 2017, as defined by the AFFA

JH James Hardie PAGE 28

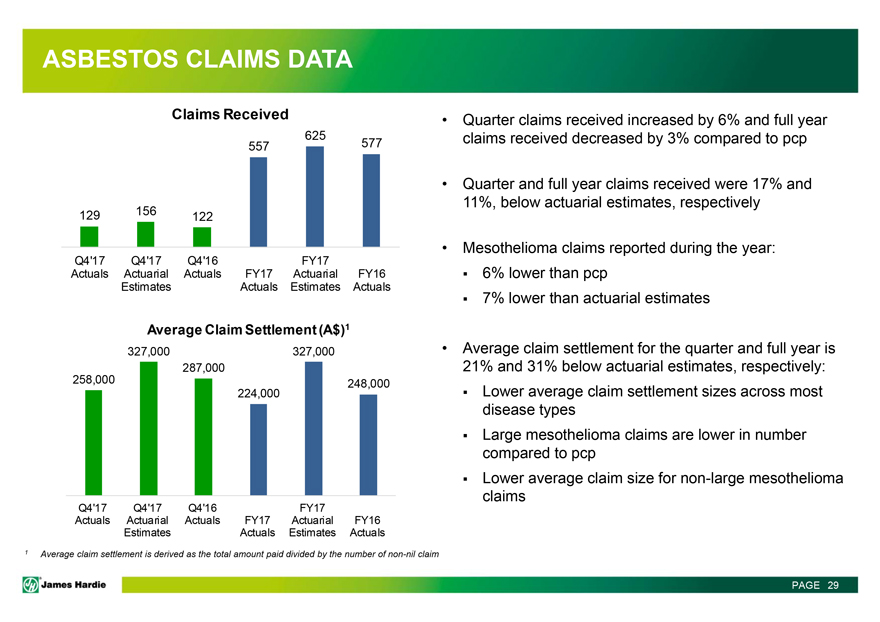

ASBESTOS CLAIMS DATA

Claims Received

625

557 577

129 156 122

Q4’17 Actuals

Q4’17 Actuarial Estimates

Q4’16 Actuals

FY17 Actuals

FY17 Actuarial Estimates

FY16 Actuals

Average Claim Settlement (A$)1

327,000 327,000

287,000

258,000 248,000

224,000

Q4’17 Actuals

Q4’17 Actuarial Estimates

Q4’16 Actuals

FY17 Actuals

FY17 Actuarial Estimates

FY16 Actuals

1 Average claim settlement is derived as the total amount paid divided by the

number of non-nil claim

Quarter claims received increased by 6% and full year claims received decreased by 3% compared to

pcp

Quarter and full year claims received were 17% and 11%, below actuarial estimates, respectively

Mesothelioma claims reported during the year:

6% lower than pcp

7% lower than actuarial estimates

Average claim settlement for the quarter and full year is

21% and 31% below actuarial estimates, respectively:

Lower average claim settlement sizes across most disease types

Large mesothelioma claims are lower in number compared to pcp

Lower average claim size for non-large mesothelioma claims

JH James Hardie PAGE 29

FY2018 KEY PLANNING ASSUMPTIONS

The modest market growth and more prolonged recovery of the US housing market to continue into FY2018. The single family new construction market and repair and remodel market are

expected to grow similar to the year-on-year growth experienced in fiscal year 2017

US Residential Housing Starts forecasted to be between 1.2 and 1.3 million

North America Fiber Cement Segment

EBIT margins expected to be in our stated

target range of 20% to 25%

Expectation is based upon the Company continuing to deliver operating performance in its plants consistent with recent quarters, and

stable exchange rates and input cost trends

Australian business expected to trend in line with the average growth of the domestic repair and remodel and single

detached housing markets in the eastern states of Australia

New Zealand growth expected to continue into fiscal year 2018

JH James Hardie PAGE 30

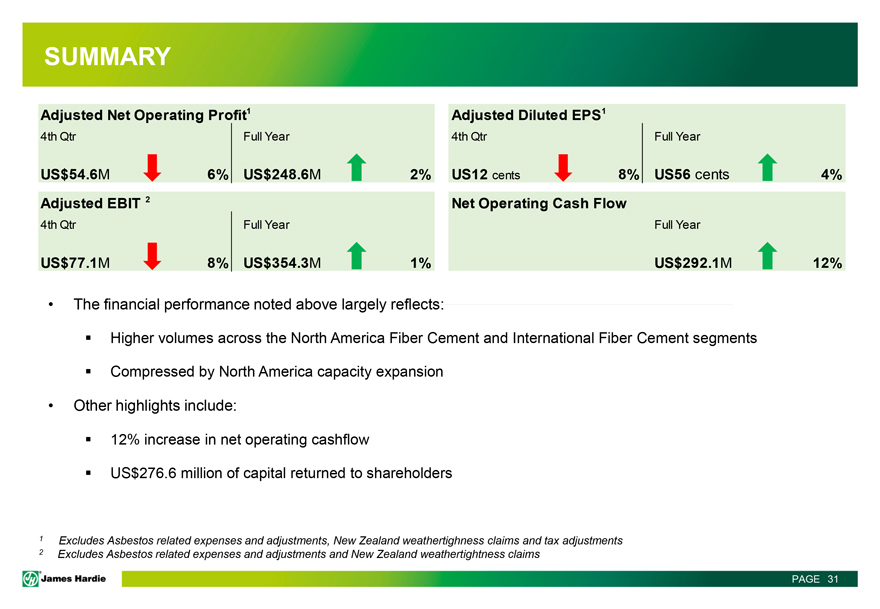

SUMMARY

Adjusted Net

Operating Profit1

4th Qtr Full Year

US$54.6M 6% US$248.6M 2%

Adjusted EBIT 2

4th Qtr Full Year

US$77.1M 8% US$354.3M 1%

Adjusted Diluted EPS1

4th Qtr Full Year

US12 cents 8% US56 cents 4%

Net Operating Cash Flow

Full Year

US$292.1M 12%

The financial performance noted above largely reflects:

Higher volumes across the North America Fiber Cement and International Fiber Cement segments

Compressed by North America capacity expansion

Other highlights include:

12% increase in net operating cashflow

US$276.6 million of capital

returned to shareholders

1 Excludes Asbestos related expenses and adjustments, New Zealand weathertighness claims and tax adjustments

2 Excludes Asbestos related expenses and adjustments and New Zealand weathertightness claims

JH James Hardie PAGE 31

JH James Hardie

QUESTIONS

JH James Hardie

APPENDIX

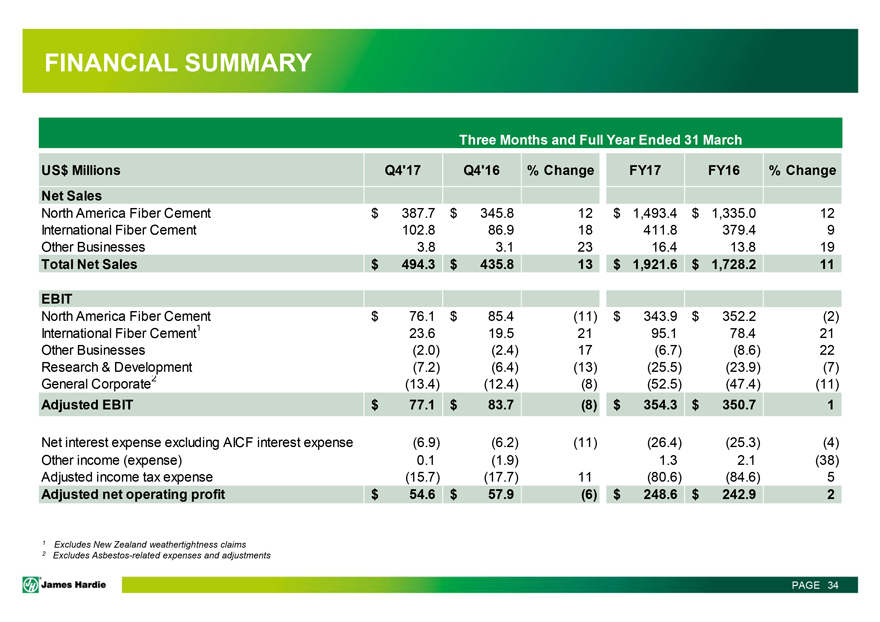

FINANCIAL SUMMARY

Three

Months and Full Year Ended 31 March

US$ Millions Q4’17 Q4’16 % Change FY17 FY16 % Change

Net Sales

North America Fiber Cement $ 387.7 $ 345.8 12 $ 1,493.4 $ 1,335.0 12

International Fiber Cement 102.8 86.9 18 411.8 379.4 9

Other Businesses 3.8 3.1 23 16.4 13.8

19

Total Net Sales $ 494.3 $ 435.8 13 $ 1,921.6 $ 1,728.2 11

EBIT

North America Fiber Cement $ 76.1 $ 85.4 (11) $ 343.9 $ 352.2 (2)

International Fiber Cement1

23.6 19.5 21 95.1 78.4 21

Other Businesses (2.0) (2.4) 17 (6.7) (8.6) 22

Research & Development (7.2) (6.4) (13) (25.5) (23.9) (7)

General

Corporate2 (13.4) (12.4) (8) (52.5) (47.4) (11)

Adjusted EBIT $ 77.1 $ 83.7 (8) $ 354.3 $ 350.7 1

Net interest expense excluding AICF interest expense (6.9) (6.2) (11) (26.4) (25.3) (4)

Other

income (expense) 0.1 (1.9) 1.3 2.1 (38)

Adjusted income tax expense (15.7) (17.7) 11 (80.6) (84.6) 5

Adjusted net operating profit $ 54.6 $ 57.9 (6) $ 248.6 $ 242.9 2

1 Excludes New Zealand

weathertightness claims

2 Excludes Asbestos-related expenses and adjustments

JH James Hardie PAGE 34

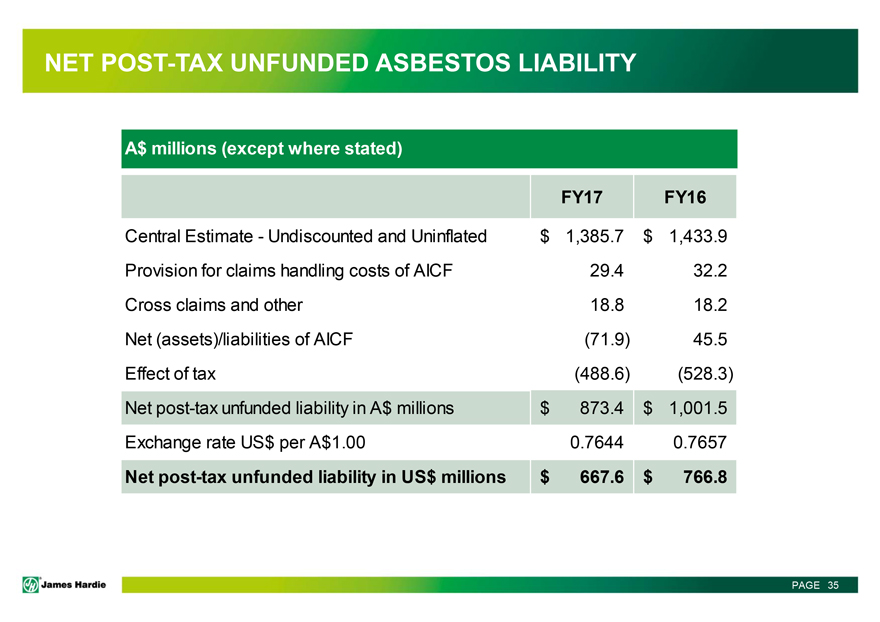

NET POST-TAX UNFUNDED ASBESTOS LIABILITY

A$ millions (except where stated)

FY17 FY16

Central Estimate - Undiscounted and Uninflated $ 1,385.7 $ 1,433.9

Provision for claims

handling costs of AICF 29.4 32.2

Cross claims and other 18.8 18.2

Net

(assets)/liabilities of AICF (71.9) 45.5

Effect of tax (488.6) (528.3)

Net post-tax unfunded liability in A$ millions $ 873.4 $ 1,001.5

Exchange rate US$ per A$1.00 0.7644 0.7657

Net post-tax unfunded liability in US$ millions $ 667.6 $ 766.8

JH James Hardie PAGE 35

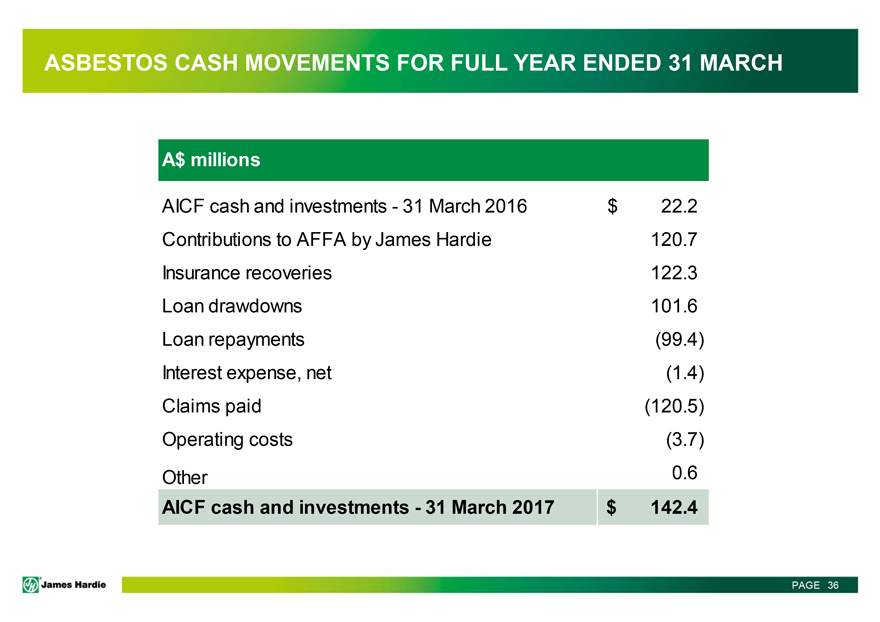

ASBESTOS CASH MOVEMENTS FOR FULL YEAR ENDED 31 MARCH

A$ millions

AICF cash and investments - 31 March 2016 $ 22.2

Contributions to AFFA by James Hardie 120.7

Insurance recoveries 122.3

Loan drawdowns 101.6

Loan repayments (99.4)

Interest expense, net (1.4)

Claims paid (120.5)

Operating costs (3.7)

Other 0.6

AICF cash and investments - 31 March 2017 $ 142.4

JH James Hardie PAGE 36

UPDATED ACTUARIAL ESTIMATE

A$ million

6,000

5,000

4,000

3,000

2,000

1,000

0

3,586 3,604

3,131 3,079 3,169 3,027 3,124 2,906

2,811 2,661 2,805 2,743

2,525 2,513 2,427

2,200

2,143

1,782 1,870 1,904

1,685 1,694 1,740

1,536 1,568 1,517 1,555 1,355 1,426 1,537 1,478 1,580

30 Jun 31 Mar 30 June 31 Mar 30

Sept 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar 31 Mar

2004 2005 2005 2006 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sensitivity Range (net, undiscounted) Discounted central estimate (net) Undiscounted central estimate (net)

JH James Hardie PAGE 37

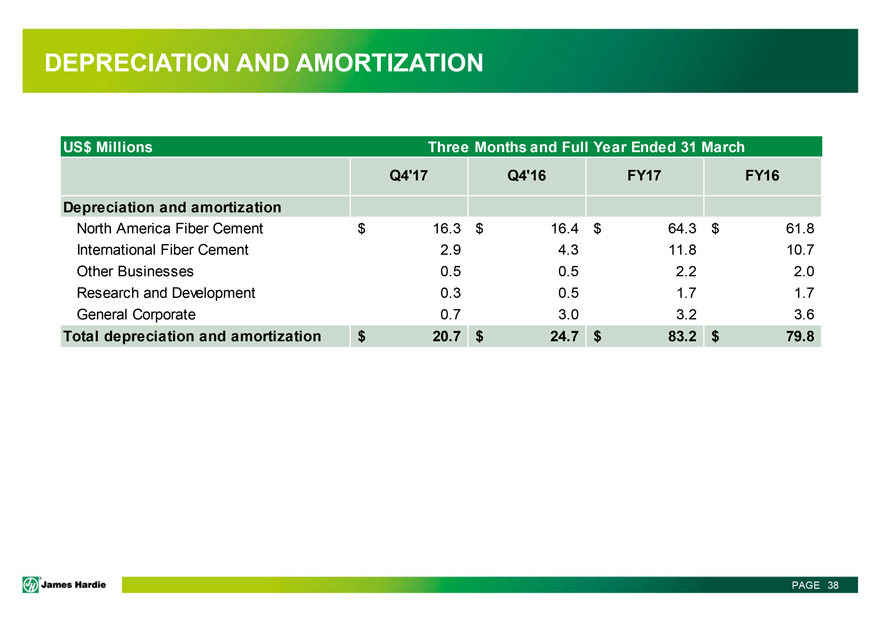

DEPRECIATION AND AMORTIZATION

US$ Millions Three Months and Full Year Ended 31 March

Q4’17 Q4’16 FY17 FY16

Depreciation and amortization

North America Fiber Cement $16.3 $16.4 $64.3

$61.8

International Fiber Cement 2.9 4.3 11.8 10.7

Other Businesses 0.5 0.5

2.2 2.0

Research and Development 0.3 0.5 1.7 1.7

General Corporate 0.7 3.0

3.2 3.6

Total depreciation and amortization $20.7 $24.7 $83.2 $79.8

JH James

Hardie PAGE 38

DEFINITIONS AND OTHER TERMS

This Management Presentation forms part of a package of information about the company’s results. It should be read in conjunction with the other parts of this

package, including the Management’s Analysis of Results, Media Release and Consolidated Financial Statements

Definitions

Non-financial Terms

AFFA – Amended and Restated

Final Funding Agreement

AICF – Asbestos Injuries Compensation Fund Ltd

Legacy New Zealand weathertightness claims (“New Zealand weathertightness claims”) – Expenses arising from defending and resolving claims in New

Zealand that allege poor building design, inadequate certification review and compliance certification and deficient work by sub-contractors

JH James Hardie PAGE 39

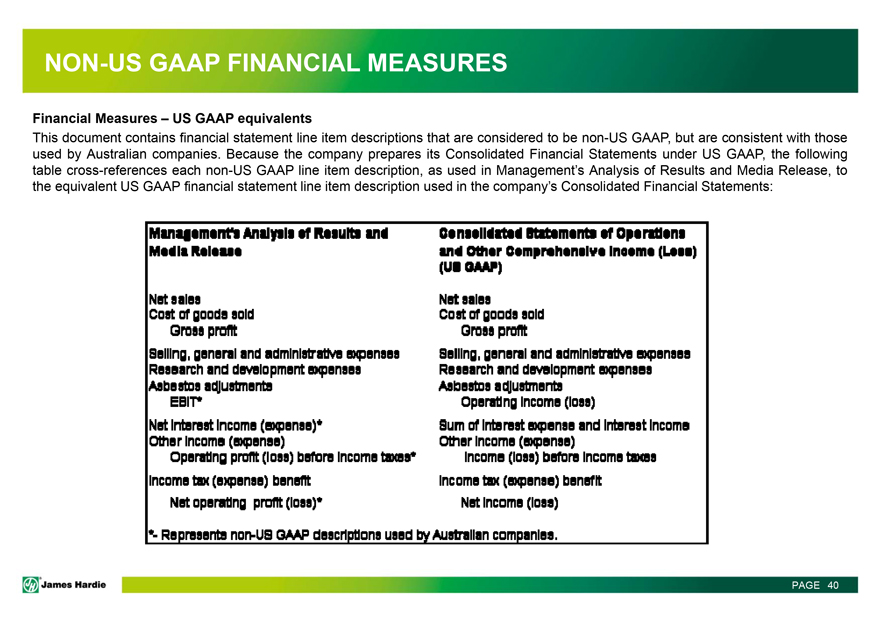

NON-US GAAP FINANCIAL MEASURES

Financial Measures – US GAAP equivalents

This document contains financial statement

line item descriptions that are considered to be non-US GAAP, but are consistent with those used by Australian companies. Because the company prepares its Consolidated Financial Statements under US GAAP,

the following table cross-references each non-US GAAP line item description, as used in Management’s Analysis of Results and Media Release, to the equivalent US GAAP financial statement line item

description used in the company’s Consolidated Financial Statements:

Management’s Analysis of Results and Media Release

Net sales

Cost of goods sold

Gross profit

Selling, general and administrative expenses

Research and development expenses

Asbestos adjustments

EBIT*

Net Interest Income (expense)*

Other Income (expense)

Operating profit (loss) before income taxes*

Income tax (expense) benefit

Net operating profit (loss)*

* Represents non-US GAAP descriptions used by Australian companies.

Consolidated Statements of Operations and Other Comprehensive Income (Loss) (US GAAP)

Net

sales

Cost of goods sold

Gross profit

Selling, general and administrative expenses

Research and development expenses

Abestos Adjustments

Operating income (loss)

Sum of interest expense and interest income

Other income (expense)

Income (loss) before income taxes

Income tax (expense) benefit

Net Income (loss)

JH James Hardie PAGE 40

NON-US GAAP FINANCIAL MEASURES

EBIT – Earnings before interest and taxes

EBIT margin – EBIT margin is defined as

EBIT as a percentage of net sales

Sales Volumes

mmsf – million square

feet, where a square foot is defined as a standard square foot of 5/16” thickness

msf – thousand square feet, where a square foot is defined as a

standard square foot of 5/16” thickness

JH James Hardie PAGE 41

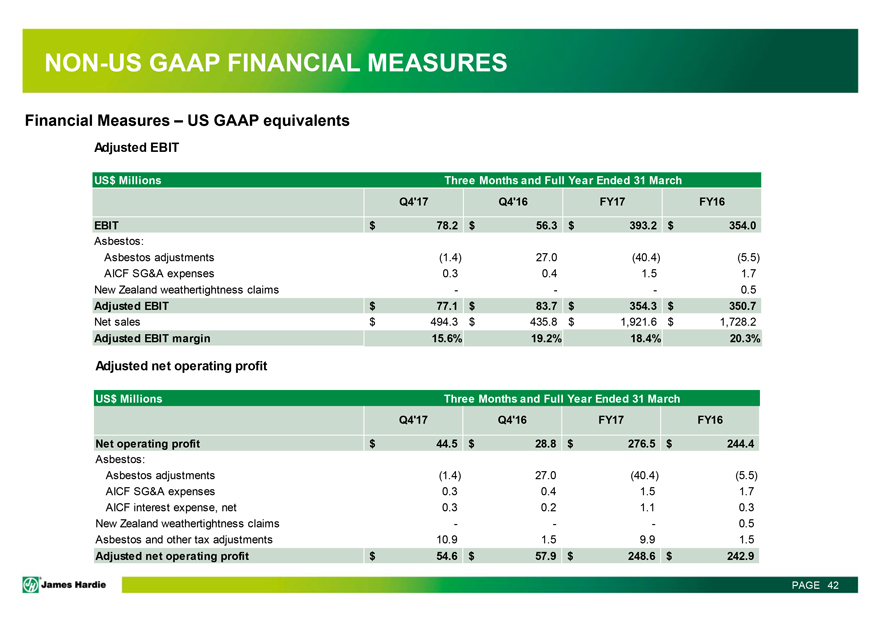

NON-US GAAP FINANCIAL MEASURES

Financial Measures – US GAAP equivalents

Adjusted EBIT

US$ Millions Three Months and Full Year Ended 31 March

Q4’17 Q4’16 FY17 FY16

EBIT $78.2 $56.3 $393.2 $354.0

Asbestos:

Asbestos adjustments (1.4) 27.0 (40.4) (5.5)

AICF SG&A expenses 0.3 0.4 1.5 1.7

New Zealand weathertightness claims - - - 0.5

Adjusted EBIT $77.1 $83.7

$354.3 $350.7

Net sales $494.3 $435.8 $1,921.6 $1,728.2

Adjusted EBIT margin

15.6% 19.2% 18.4% 20.3%

Adjusted net operating profit

US$ Millions Three

Months and Full Year Ended 31 March

Q4’17 Q4’16 FY17 FY16

Net

operating profit $44.5 $28.8 $276.5 $ 244.4

Asbestos:

Asbestos adjustments

(1.4) 27.0 (40.4) (5.5)

AICF SG&A expenses 0.3 0.4 1.5 1.7

AICF interest

expense, net 0.3 0.2 1.1 0.3

New Zealand weathertightness claims - - - 0.5

Asbestos and other tax adjustments 10.9 1.5 9.9 1.5

Adjusted net operating

profit $54.6 $57.9 $248.6 $ 242.9

JH James Hardie PAGE 42

NON-US GAAP FINANCIAL MEASURES

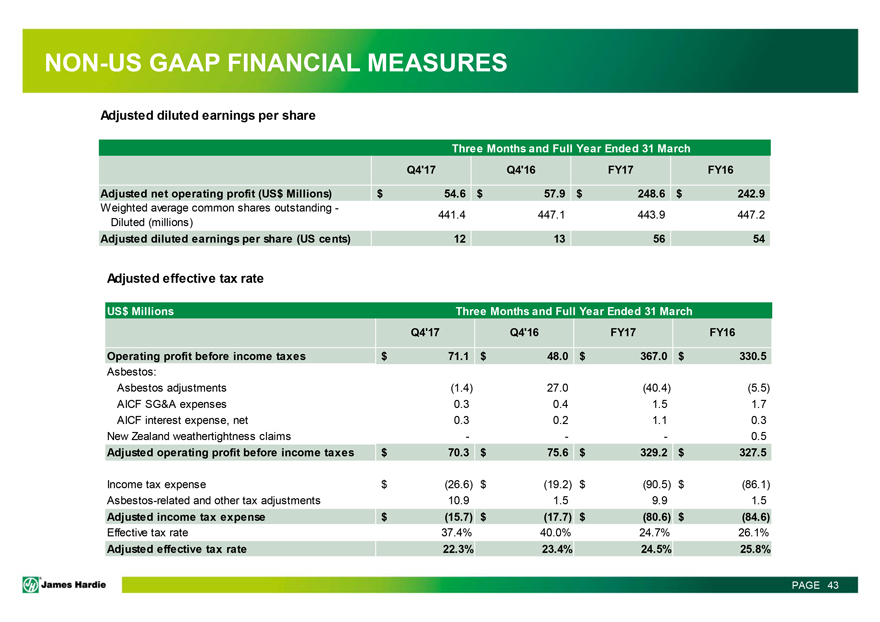

Adjusted diluted earnings per share

Three Months and Full Year Ended 31 March

Q4’17 Q4’16 FY17 FY16

Adjusted net operating profit (US$ Millions) $ 54.6 $57.9

$248.6 $242.9

Weighted average common shares outstanding - Diluted (millions) 441.4 447.1 443.9 447.2

Adjusted diluted earnings per share (US cents) 12 13 56 54

Adjusted effective tax rate

US$ Millions Three Months and Full Year Ended 31 March

Q4’17

Q4’16 FY17 FY16

Operating profit before income taxes $71.1 $48.0 $367.0 $330.5

Asbestos:

Asbestos adjustments (1.4) 27.0 (40.4) (5.5)

AICF SG&A expenses 0.3 0.4 1.5 1.7

AICF interest expense, net 0.3 0.2 1.1 0.3

New Zealand weathertightness claims - - - 0.5

Adjusted operating profit before income taxes

$70.3 $75.6 $329.2 $327.5

Income tax expense $(26.6) $(19.2) $(90.5) $(86.1)

Asbestos-related and other tax adjustments 10.9 1.5 9.9 1.5

Adjusted income

tax expense $(15.7) $(17.7) $(80.6) $(84.6)

Effective tax rate 37.4% 40.0% 24.7% 26.1%

Adjusted effective tax rate 22.3% 23.4% 24.5% 25.8%

JH James Hardie PAGE 43

NON-US GAAP FINANCIAL MEASURES

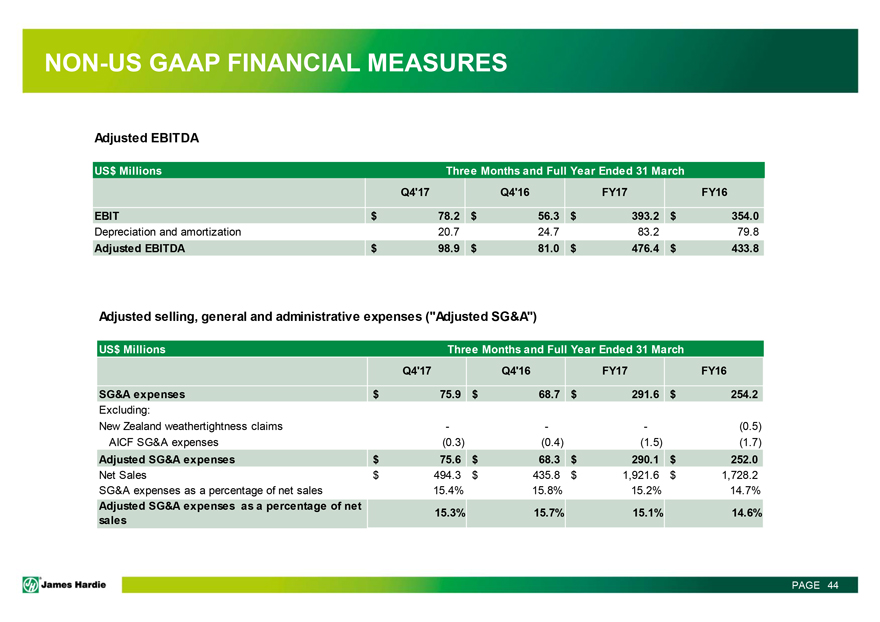

Adjusted EBITDA

US$ Millions Three Months and Full Year Ended 31 March

Q4’17 Q4’16 FY17 FY16

EBIT $78.2 $56.3 $393.2 $354.0

Depreciation and amortization 20.7 24.7 83.2 79.8

Adjusted EBITDA $98.9 $81.0 $476.4 $433.8

Adjusted selling, general and administrative expenses (“Adjusted SG&A”)

US$ Millions Three Months and Full Year Ended 31 March

Q4’17 Q4’16 FY17 FY16

SG&A expenses $75.9 $68.7 $291.6 $254.2

Excluding:

New Zealand weathertightness claims - - - (0.5)

AICF SG&A expenses (0.3) (0.4) (1.5) (1.7)

Adjusted SG&A expenses $75.6 $68.3 $290.1 $252.0

Net Sales $494.3 $435.8

$1,921.6 $1,728.2

SG&A expenses as a percentage of net sales 15.4% 15.8% 15.2% 14.7%

Adjusted SG&A expenses as a percentage of net 15.3% 15.7% 15.1% 14.6%

sales

JH James Hardie PAGE 44

JH James Hardie

Q4 FY17

MANAGEMENT PRESENTATION

18 May 2017